Big Week Ahead. Get Ready!

Will The Fed Move by .50 Again in November?

KR Opinion

This Post is Too Long For Email; go to Kendallreport.substack.com for the full report.

As we approach a pivotal week in the economic calendar, we are drawn to the forthcoming employment numbers, job openings data, and the usual claims figures. However, an undercurrent warrants closer scrutiny: the International Longshoremen's Association (ILA) contract negotiations. This situation affects every port from Boston to Houston, and its ramifications could ripple through our entire supply chain with alarming speed.

For every day these ports remain closed, shipment delays could multiply sixfold. It's akin to shutting down a major airport—the backlog doesn't just disappear when operations resume. Instead, it compounds, creating a logistical nightmare that could take weeks, if not months, to untangle.

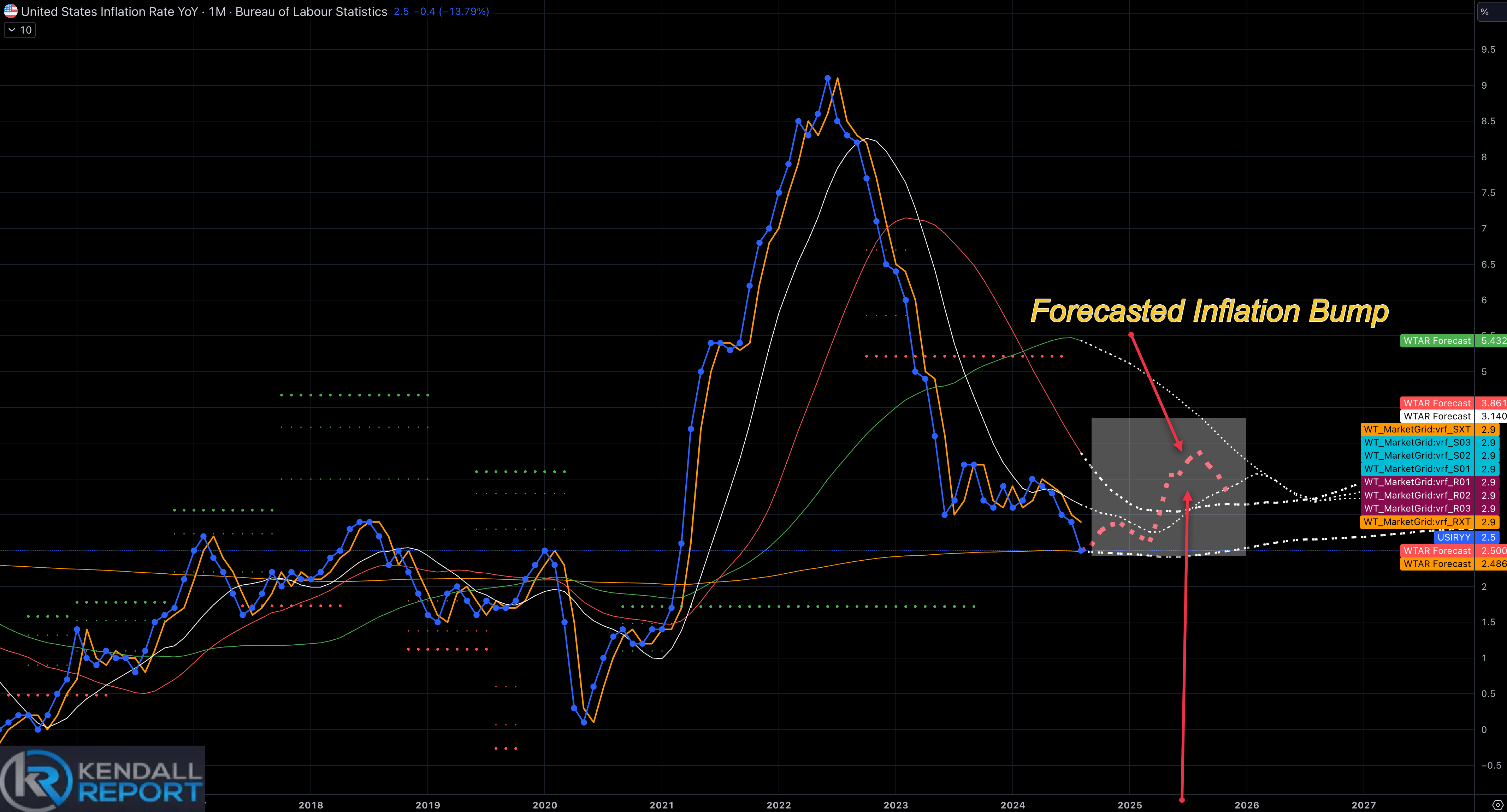

The prospect of a jump in inflation as we enter October, which seemed like a cautious forecast months ago, might materialize with startling accuracy if this longshoremen's strike gains traction. Widespread layoffs loom large, potentially significantly casting a long shadow over our employment situation if the dispute extends beyond two weeks.

The ILA reportedly seeks a 76% raise – a figure that dwarfs the 36% increase secured by their West Coast counterparts last year. If successful, this could trigger a domino effect, dramatically increasing shipping costs and creating material issues across various industries. The inflation spike cautioned about earlier seems less like a guesstimate and more like an impending reality.

Algorithms that initially suggested this inflationary trend are now potentially validated by real-world events, underscoring the delicate balance of our economic ecosystem. The Biden administration has thus far maintained a hands-off approach to these negotiations. While government intervention in labor disputes is often a double-edged sword, we've seen the far-reaching effects of recent standoffs with auto workers and West Coast longshoremen. As inflation squeezes households nationwide, this latest dispute could fuel an already smoldering fire.

Regarding the imminent employment figures, while no earth-shattering revelations are anticipated, the unemployment rate might increase to around 4.4%. The Fed funds market is beginning to price in another 50-basis point cut, which would bring us down to 4.25%. The trajectory of the longshoremen's negotiations could play a crucial role in swaying the Fed's decision-making process.

From a market perspective, technical indicators suggest we may be in for a decline as we navigate the first couple of weeks of October. This downturn might extend further, especially considering we're just over a month away from a significant election. The confluence of these factors presents a complex tapestry of economic variables to unravel in the weeks ahead.

On a broader scale, we're witnessing a shift towards more accommodative policies from central banks around the globe. This trend could reignite demand and fan the flames of global inflationary pressures, adding another layer of complexity to our economic outlook.

As we stand on the cusp of what promises to be a fascinating 30 to 60 days in the financial world, the interconnectedness of our global economy is evident. The longshoremen's negotiations, while seemingly isolated, have the potential to set off a chain reaction that could reshape our economic trajectory in the short to medium term. The coming weeks promise to be remarkable, with these developments potentially radically reshaping our economic landscape.

Looking Back on last week

The market's focus shifted to China last week as officials unveiled a series of measures aimed at stimulating the economy. The People's Bank of China lowered key rates and hinted at further cuts while a substantial fiscal spending package was announced. Chinese equities responded positively, with the Shanghai Composite and Hong Kong's Hang Seng surging 13.0% for the week. Risk assets in Europe and the U.S. also showed strength, though oil price pressures kept growth concerns in view.

Semiconductor stocks gained momentum after Micron's strong quarterly results and guidance, driving the PHLX Semiconductor Index up 4.3% for the week. Treasury yields saw mixed movements, with longer-dated securities experiencing slight losses while the 2-year note made small gains. Rate cut expectations increased, with the Fed funds futures market indicating a higher probability of another 50-basis point cut in November.

Market sentiment remained optimistic about a soft landing for the economy despite growing expectations of potential consolidation. The Dow Jones Industrial Average and S&P 500 extended their record-breaking run, while the Nasdaq Composite also advanced.

Key economic data releases included a significant drop in the Consumer Confidence Index to 98.7 in September (KR Forecast 102.9). New home sales in August exceeded expectations at 716,000 (KR Forecast 695,000). Initial jobless claims fell to 218,000 (KR Forecast 224,000), indicating continued labor market resilience. The third estimate for Q2 GDP held steady at 3.0%, with personal spending at 2.8%, surpassing recent averages and suggesting robust consumer activity.

Friday's trading session began positively, bolstered by encouraging economic data showing moderation in PCE price inflation and improved consumer sentiment. However, momentum waned as the day progressed, with the information technology sector underperforming. Despite this, the broader market maintained an overall positive tone, evidenced by gains in the equal-weighted S&P 500 and Russell 2000.

Throughout the week, global central banks, including the Fed, ECB, and People's Bank of China, moved towards more accommodative policy stances. This shift and China's stimulus measures fueled optimism about improving global growth prospects. The materials sector and industrial stocks like Caterpillar reflected this sentiment, with the latter reaching an all-time high.

Energy prices continued fluctuating, with OPEC+ announcing plans to increase oil output in December. This news contributed to a decline in WTI crude futures, which fell to $67.68/bbl by week's end. The energy sector felt the impact, underperforming other market segments.

As the third quarter draws to a close, investors remained attentive to economic indicators and central bank policies, balancing optimism about growth with ongoing concerns about inflation and geopolitical tensions. The market's resilience in the face of mixed signals highlighted the complex interplay of factors shaping current financial landscapes.

This Week’s economic releases

Sep 30

· 09:45 ET: Chicago PMI (Sep) Impact: Low KR Forecast: 46.5 KR Cons: 46.2 Prior: 46.1

Midnight on the 30th, the international longshoremen are slated to walk off the job unless there is a settlement.

Oct 01

· 09:45 ET: S&P Global US Manufacturing PMI - Final (Sep) Impact: Low KR Forecast: NA KR Cons: NA Prior: 47.9

· 10:00 ET: ISM Manufacturing Index (Sep) Impact: High KR Forecast: 47.4% KR Cons: 47.7% Prior: 47.2%

· 10:00 ET: JOLTS - Job Openings (Aug) Impact: Medium KR Forecast: NA KR Cons: NA Prior: 7.673M

· 10:00 ET: Construction Spending (Aug) Impact: Low KR Forecast: 0.3% KR Cons: 0.1% Prior: -0.3%

Oct 02

· 07:00 ET: MBA Mortgage Applications Index (09/28) Impact: Low KR Forecast: NA KR Cons: NA Prior: 11.0%

· 08:15 ET: ADP Employment Change (Sep) Impact: Medium KR Forecast: 95K KR Cons: 120K Prior: 99K

· 10:30 ET: EIA Crude Oil Inventories (09/28) Impact: High KR Forecast: NA KR Cons: NA Prior: -4.47M

Oct 03

· 08:30 ET: Initial Claims (09/28) Impact: High KR Forecast: 221K KR Cons: 223K Prior: 218K

· 08:30 ET: Continuing Claims (09/21) Impact: High KR Forecast: NA KR Cons: NA Prior: 1834K

· 09:45 ET: S&P Global US Services PMI - Final (Sep) Impact: Low KR Forecast: NA KR Cons: NA Prior: 55.7

· 10:00 ET: Factory Orders (Aug) Impact: Low KR Forecast: 0.1% KR Cons: 0.1% Prior: 5.0%

· 10:00 ET: ISM Non-Manufacturing Index (Sep) Impact: High KR Forecast: 51.7% KR Cons: 51.6% Prior: 51.5%

· 10:30 ET: EIA Natural Gas Inventories (09/28) Impact: Low KR Forecast: NA KR Cons: NA Prior: +47 bcf

Oct 04

· 08:30 ET: Nonfarm Payrolls (Sep) Impact: High KR Forecast: 120K KR Cons: 135K Prior: 142K

· 08:30 ET: Nonfarm Private Payrolls (Sep) Impact: High KR Forecast: 105K KR Cons: 125K Prior: 118K

· 08:30 ET: Avg. Hourly Earnings (Sep) Impact: High KR Forecast: 0.3% KR Cons: 0.3% Prior: 0.4%

· 08:30 ET: Unemployment Rate (Sep) Impact: High KR Forecast: 4.3% KR Cons: 4.2% Prior: 4.2%

· 08:30 ET: Average Workweek (Sep) Impact: High KR Forecast: 34.3 KR Cons: 34.3 Prior: 34.3

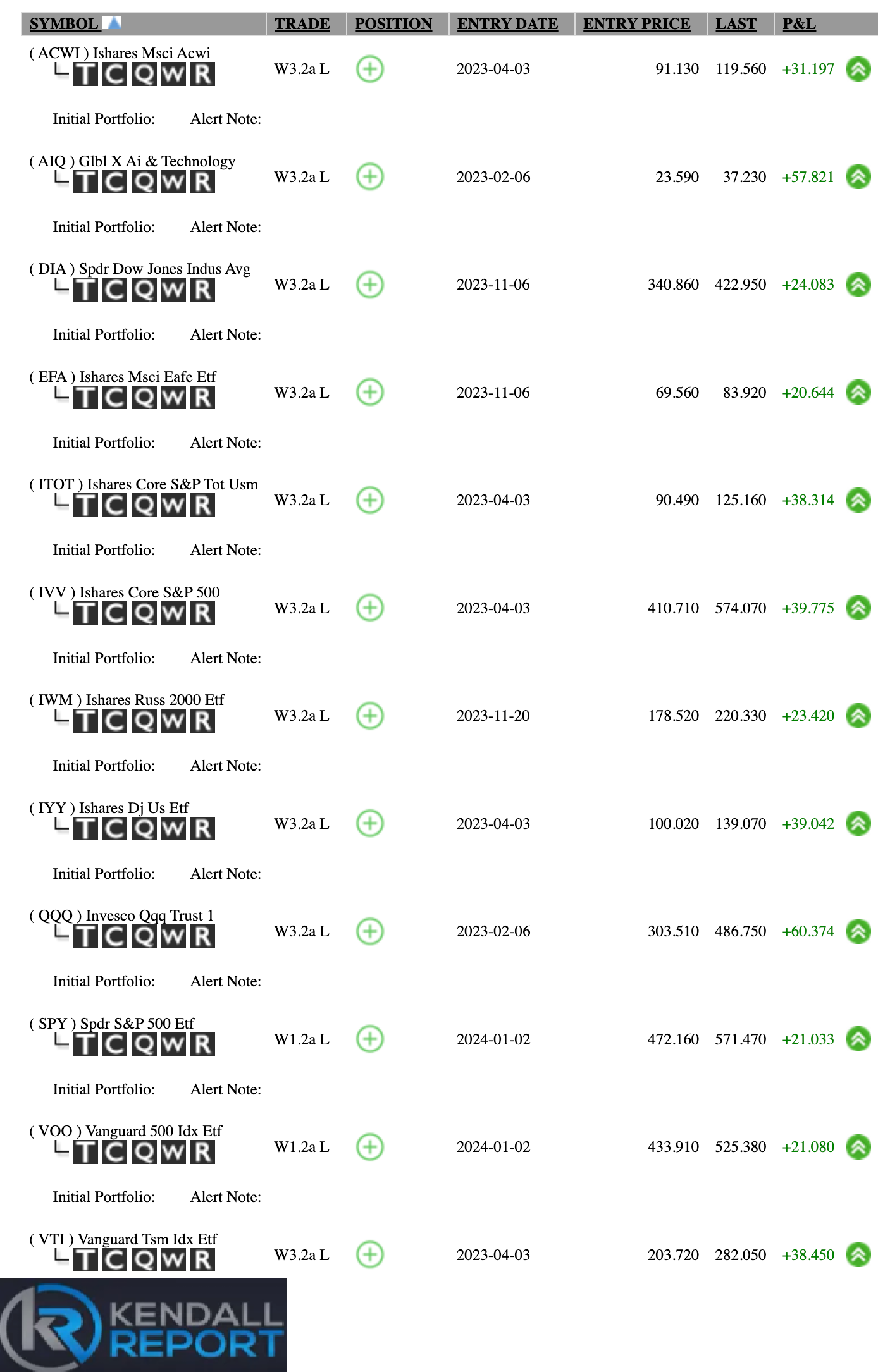

WaveTech Open Position Report by Index

WaveTech Database

The latest database update has revealed some genuinely remarkable figures, showcasing the resilience and strength of the current market trend. We've witnessed an astounding 1,889 new entries in the intermediate models, coupled with only 248 exits. This substantial influx has propelled the bullish percent to a staggering 82%, meaning that 8 out of every 10 symbols in the database are now in trend mode.

This development is nothing short of extraordinary. To put it in perspective, even when the bullish percent surpassed 72%, the lowest it subsequently retreated to was 61%. We're seeing it rebound to 82%, setting a new high for the year. Just when we thought the cycle might be nearing completion, it appears to be rejuvenating, gearing up for another round of forward-looking market movement.

The short-term database tells a similar story of robust market health. With 940 new buys and 482 exits, we're looking at a bullish percent of 69.58%. While this figure has rebounded somewhat from its recent lows, it still paints a picture of a market in a strong uptrend.

Sector-wise, we're seeing widespread strength. The technology sector has re-emerged as a new buy, bringing the number of bullish sectors to nine out of twelve. Only basic materials, energy, and transportation remain neutral, with everything else firmly in the green. What's particularly noteworthy is that five of the nine bullish sectors are only about 30-40% through their normal holding cycle, suggesting substantial room for further growth.

The semiconductor industry has returned, and we're observing continued rotation within the tech sector. This rotation is occurring even as we anticipated some flattening in performance. As viewed through the lens of the intermediate models, the financial sector maintains its extended position only about three-quarters of the way through its cycle. This hints at the potential for continued strength into the year-end and possibly extending into the first quarter of 2025.

Interestingly, all expectations of market hesitation or caution in the lead-up to the election have been dispelled. The markets are fearless as they forge ahead, seemingly undeterred by potential political uncertainties.

This bull market's persistence is genuinely remarkable. It defies conventional wisdom and continues to surprise. Our robust configuration across various timeframes and sectors suggests a strong market showing signs of sustainable momentum.