Bitcoin Collapsing ETFs Suckered them All In For the Kill...

Equity Markets Continue the Upward Trek!

KR Opinion

As we leave the holiday and into the final day of the first week of July, I hope everyone in the US had a safe 4th of July and that those elsewhere enjoyed a day off from the markets.

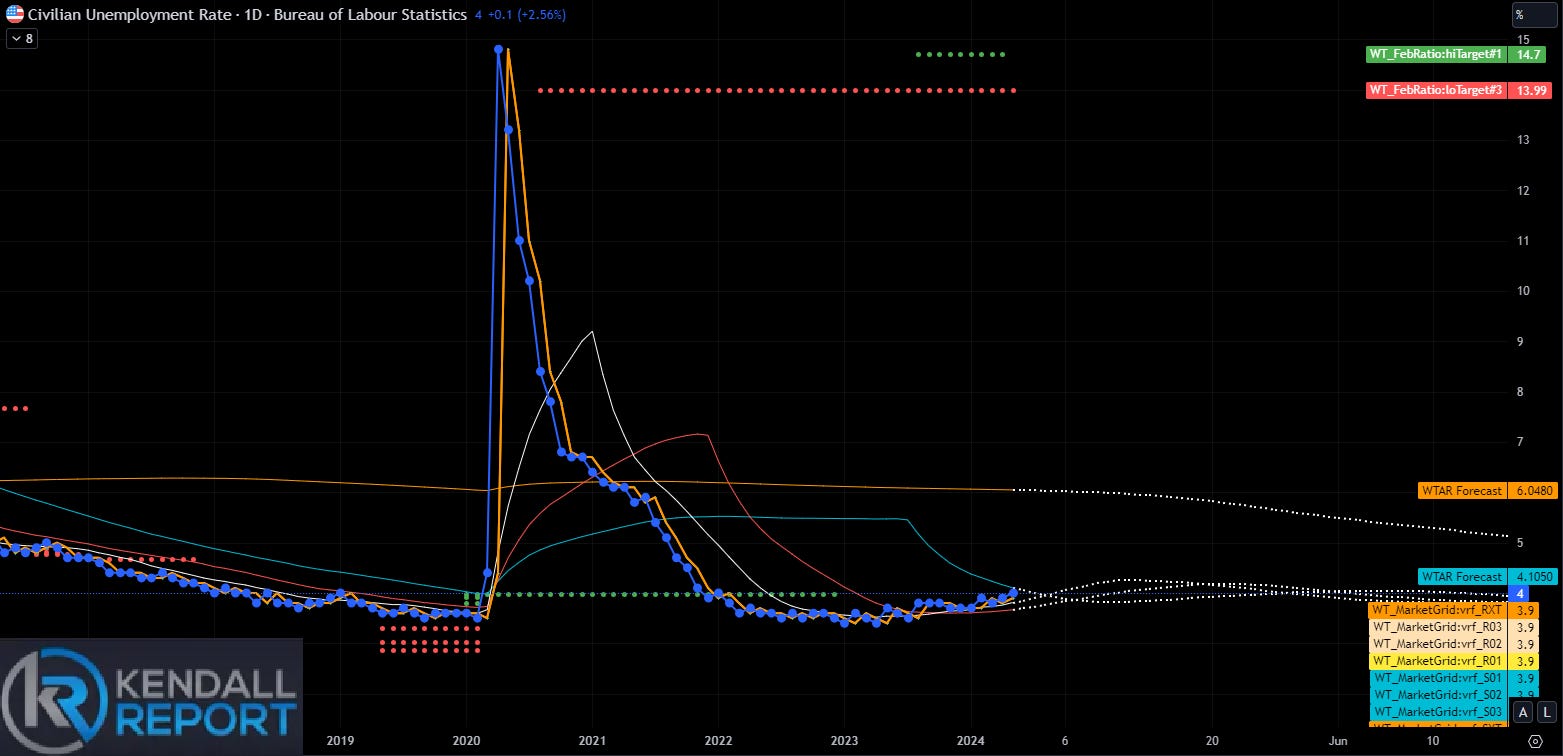

With the release of the unemployment numbers, the consensus expectation is for the unemployment rate to remain unchanged. However, I anticipate a slight increase to 4.2% over the next two to three months. While this is not a substantial rise, it suggests some shifts in the employment landscape.

The forecast for non-farm payrolls is set at 170,000, with the average work week expected to remain steady. There doesn’t appear to be significant market-moving data here, but a surprise could emerge if the non-farm private payrolls, projected at 150,000, come in weaker than expected. Although these figures are not shocking, they have declined over recent months, though not turning negative.

On Wednesday, the continuing and weekly claims data were released without surprises, remaining stable at current levels. My expectation for today is that we might see some deterioration, possibly a downside surprise. This raises the question: Is bad news good, or is bad news just bad news? We will find out tomorrow.

Overall, with the markets continuing to hit new highs, it seems unlikely that we will see a major reversal. While today's news might not significantly impact the market, any surprise will likely come from this report.

In next Monday's report, I will examine longer-term market trends and discuss how we are preparing for the final two months of Q3.

Looking back on Wednesday’s action

The S&P 500 (+0.5%) and Nasdaq Composite (+0.9%) reached new record highs in this holiday-shortened session. The Russell 2000 (+0.1%) and S&P Mid Cap 400 (+0.3%) also posted gains. However, the price-weighted Dow Jones Industrial Average (-0.1%) fell slightly due to a decline in its top-weighted component, United Healthcare (UNH 489.89, -8.35, -1.7%).

Strong performances from mega-cap stocks significantly impacted the indexes, but many other stocks also saw gains. Notable performers included NVIDIA (NVDA 128.28, +5.61, +4.6%), Broadcom (AVGO 1729.22, +71.74, +4.3%), Tesla (TSLA 246.39, +15.13, +6.5%), Apple (AAPL 221.55, +1.28, +0.6%), Microsoft (MSFT 460.77, +1.49, +0.3%), and Alphabet (GOOG 187.39, +0.78, +0.4%).

These gains helped propel the S&P 500 information technology sector to the top leaderboard among the 11 sectors, rising 1.5% daily. The materials (+0.8%) and utilities (+0.6%) sectors were also among the top performers.

In contrast, the healthcare sector (-0.7%) experienced the most significant decline due to losses in United Healthcare, Eli Lilly (LLY 898.10, -8.61, -1.0%), and others.

A drop in market rates acted as a catalyst for stocks. The yield on the 10-year Treasury note fell nine basis points to 4.35%, and the yield on the 2-year note fell four basis points to 4.70%. The Treasury market will close at 2:00 p.m. ET.

·Nasdaq Composite: +21.2% YTD

·S&P 500: +16.1% YTD

·S&P Midcap 400: +4.9% YTD

·Dow Jones Industrial Average: +4.3% YTD

·Russell 2000: +0.5% YTD

·Reviewing Wednesday’s Economic releases:

- Weekly MBA Mortgage Applications Index: -2.6% (previously +0.8%)

- June ADP Employment Change: 150K (KR Forecast consensus 163K); previous revised to 157K from 152K

- Weekly Initial Claims: 238K (KR Forecast consensus 235K); previous revised to 234K from 233K

- Weekly Continuing Claims: 1.858 million; previous revised to 1.832 million from 1.839 million

- Key takeaway: Initial jobless claims have increased slightly but remain below recession levels. However, the rising continuing jobless claims suggest that finding new employment after layoffs is becoming more challenging, indicating a slowdown in the labor market.

- May Trade Balance: -$75.1 billion (KR Forecast consensus -$76.0 billion); previous revised to -$74.5 billion from -$74.6 billion

- Key takeaway: Declines in both exports and imports signal a decrease in overall trade demand in May.

- June S&P Global US Services PMI - Final: 55.3 (previously 55.3)

- May Factory Orders: -0.5% (KR Forecast consensus +0.3%); previously revised to +0.4% from +0.7%

- Key takeaway: A drop in business spending in May aligns with a slowdown in manufacturing activity, as reflected in the advance durable goods report.

- June ISM Non-Manufacturing Index: 48.8% (KR Forecast consensus 52.5%); previous 53.8%

- Key takeaway: This indicates a contraction in the nation's largest sector, reinforcing expectations that the Fed may cut rates before the end of the year.

Friday Economic Releases

At 8:30 ET, the market will closely watch the release of several key economic indicators for June, each carrying a high trading impact.

According to KR's forecast, the Nonfarm Payrolls report is expected to show an increase of 170K jobs, slightly below the consensus estimate of 185 K. This follows a prior increase of 272K jobs.

Similarly, Nonfarm Private Payrolls are forecasted to rise by 150K jobs, compared to the consensus expectation of 160K and the prior month's increase of 229 K.

Average Hourly Earnings are anticipated to grow by 0.3%, matching the consensus forecast but down from the previous month's 0.4% increase.

The Unemployment Rate is projected to hold steady at 4.0%, unchanged from the prior month, in both KR's forecast and the consensus estimate.

Lastly, the Average Workweek is expected to remain unchanged at 34.3 hours, consistent with the KR forecast and the consensus.

These reports will provide critical insights into the labor market's current state and could significantly influence trading decisions.

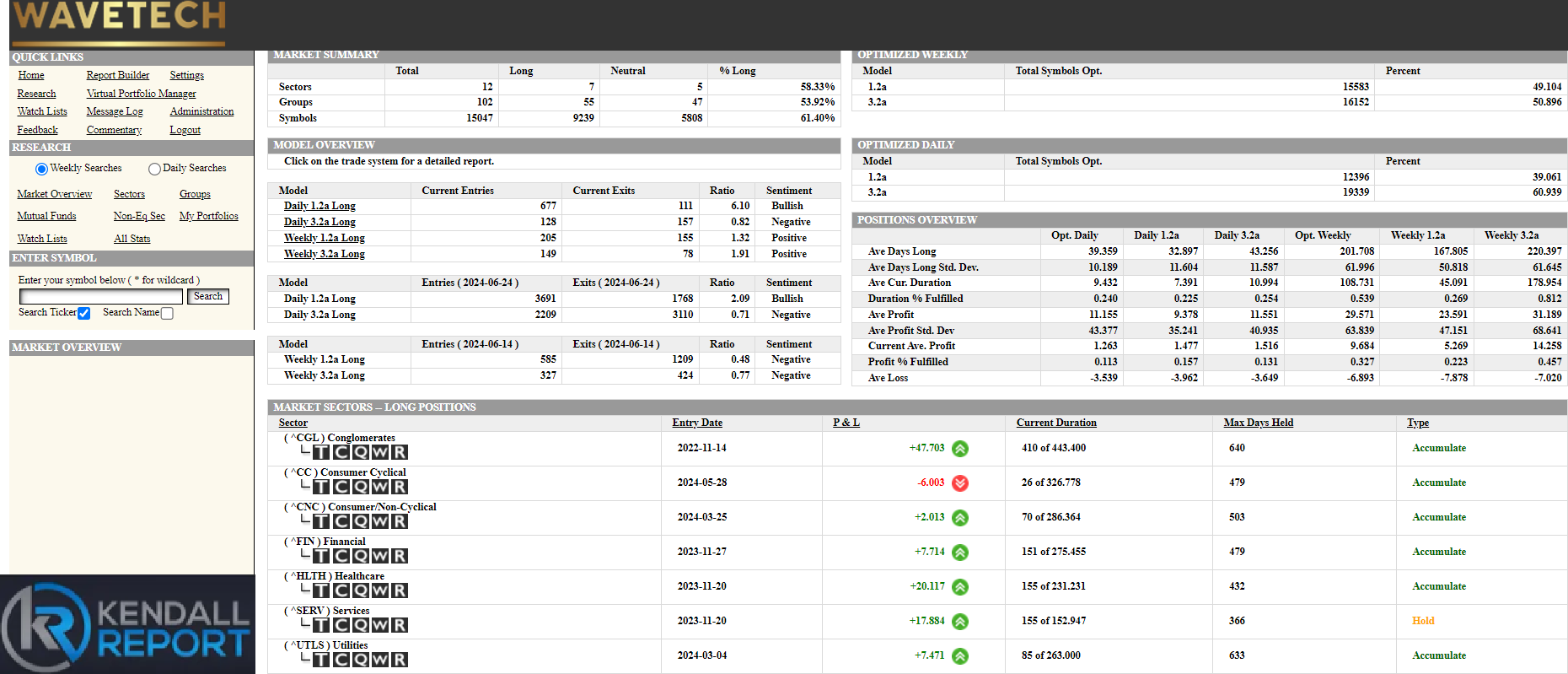

WaveTech Data Base

Once again, we conducted an intermediate run on our database and observed minimal changes. We saw 354 new entries compared to 233 exits, resulting in a bullish percentage of 61.40 on the intermediate database. I double-checked to ensure the database was functioning correctly because this number has remained at this level for some time. Despite the indexes reaching all-time new highs, the stocks have no significant new rotation.

Similarly, we recorded 805 new entries and 268 exits on the daily models, yielding a bullish percent of 51.31%. In conclusion, there has been no significant change for another week. I expect some rotation in the intermediate database, but it has not materialized.

Interestingly, although we see much leadership returning to the Magnificent 7 stocks, the overall database remains unchanged, maintaining the same sectors without any new rotation. We observe a smaller subset of sectors and groups that continue to lead and push the market forward.

While there were expectations for broader movement, the markets have primarily experienced sideways movement within a wide range. Now, we are seeing the markets gradually print new highs as they continue to advance.

S&P 500 Futures