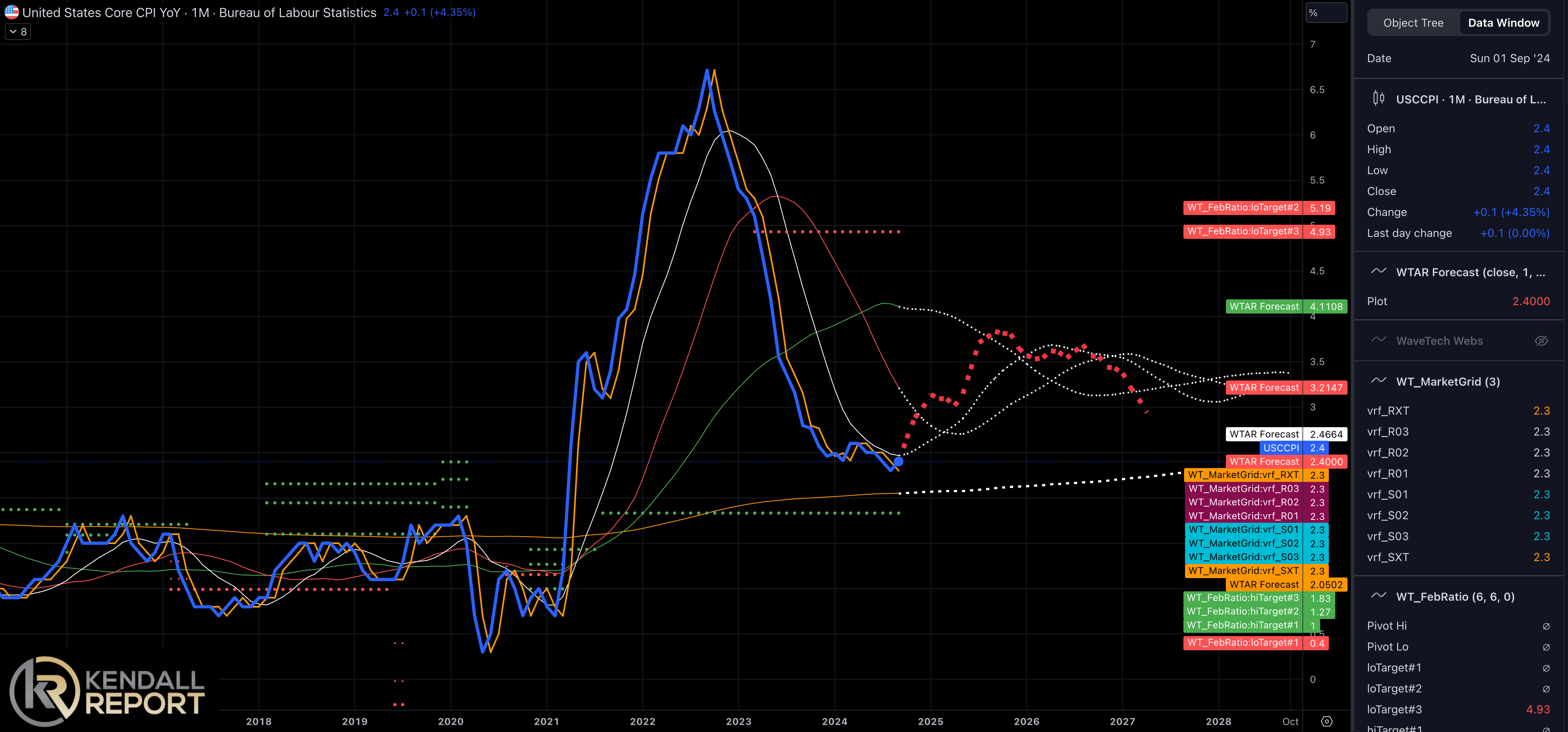

CPI Surprize?

Bitcoin Stalls

KR Opinion

The market enters a pivotal period with tomorrow's CPI release, where expectations center on a modest 0.2% month-over-month increase. However, current indicators suggest the potential for what could be characterized as an "echo bounce" in inflation metrics. This possibility gains particular relevance given the prospect of new tariffs under the Trump administration and other emerging inflationary pressures.

Forward-looking inflation expectations have crept up to approximately 3.2%, while projections suggest potential inflation rates returning to around 3.5%. This anticipated echo effect could manifest over several quarters, driven by multiple factors now coming into focus.

The year's market performance has been remarkable, with the NASDAQ's 28.5% gain leading the charge. NVIDIA's continued ascent toward $150 per share exemplifies the market's enthusiasm for AI-related opportunities, cementing its position as Wall Street's premier growth story. This performance underscores the reality of the AI boom and its tangible impact on market valuations.

Current overnight trading shows some hesitancy, though buyers appear to be stepping in ahead of the U.S. open and CPI release. This pre-release positioning suggests market participants may anticipate inflation data supporting the current bullish narrative.

The convergence of these factors—potential inflation dynamics, strong tech sector performance, and continued AI momentum—creates an intriguing market environment. While this year's remarkable gains might raise questions about sustainability, the underlying drivers, particularly in the technology sector, appear to maintain their strength.

These next few trading sessions could reveal particular aspects of market direction as participants digest the CPI data and its implications for monetary policy and economic growth. Despite some overnight apprehension, pre-market buying interest suggests continued confidence in the upward trajectory.

Looking back on Tuesday’s action

Today's market action represented a modest consolidation after the strong post-election rally. The Russell 2000 experienced the most significant pullback, declining 1.8% while maintaining a robust 5.8% gain since election day.

Rising market rates influenced today's trading dynamics, with the 10-year yield climbing 12 basis points to 4.43% and the 2-year yield increasing nine basis points to 4.34%. This rate movement contributed to broader market profit-taking activity.

Market breadth reflected widespread selling pressure, evidenced by the Invesco S&P 500 Equal Weight ETF's 0.8% decline and losses in nine S&P 500 sectors. Consumer discretionary stocks faced pressure, dropping 1.1%, with notable declines in sector leaders Tesla (-6.2% to $328.49) and Home Depot (-1.3% to $403.08).

However, select mega-cap technology names provided some market stability, with Microsoft advancing 1.2% to $423.03 and NVIDIA gaining 2.1% to $148.29. These gains helped offset some of the broader market weakness.

Today's Economic data showed encouraging inflation trends, with the New York Fed's Survey of Consumer Expectations revealing declining inflation expectations across multiple time horizons. Year-ahead expectations eased to 2.9% from 3.0%, three-year projections decreased to 2.5% from 2.7%, and five-year expectations moderated to 2.8% from 2.9%. Additionally, the NFIB Small Business Optimism index showed improvement, rising to 93.7 in October from September's 91.5 reading.

This consolidation pattern appears healthy following last week's strong gains, suggesting a market digesting recent advances rather than signaling a significant shift in sentiment. The mixed performance between smaller caps and mega-cap technology leaders highlights ongoing market rotation dynamics as participants adjust positions ahead of upcoming inflation data.

Nasdaq Composite: +28.5%

S&P 500: +25.5%

S&P Midcap 400: +18.4%

Russell 2000: +18.0%

Dow Jones Industrial Average: +16.5%

WaveTech Database