Fed Decision! Will It Surprise?

.25or .50 Basis Points?

KR Opinion

Reflecting on Tuesday’s market action, I'm struck by the initial enthusiasm that propelled the S&P 500 and the Dow Jones Industrial Average to new all-time intraday highs. It was an exciting start.

However, as the day progressed, I observed a gradual retreat from these peak levels, with both indices ultimately closing near their flat lines. This pullback from the highs tells me that while there's underlying optimism in the market, there's also a degree of caution as we approach tomorrow's crucial Federal Reserve decision.

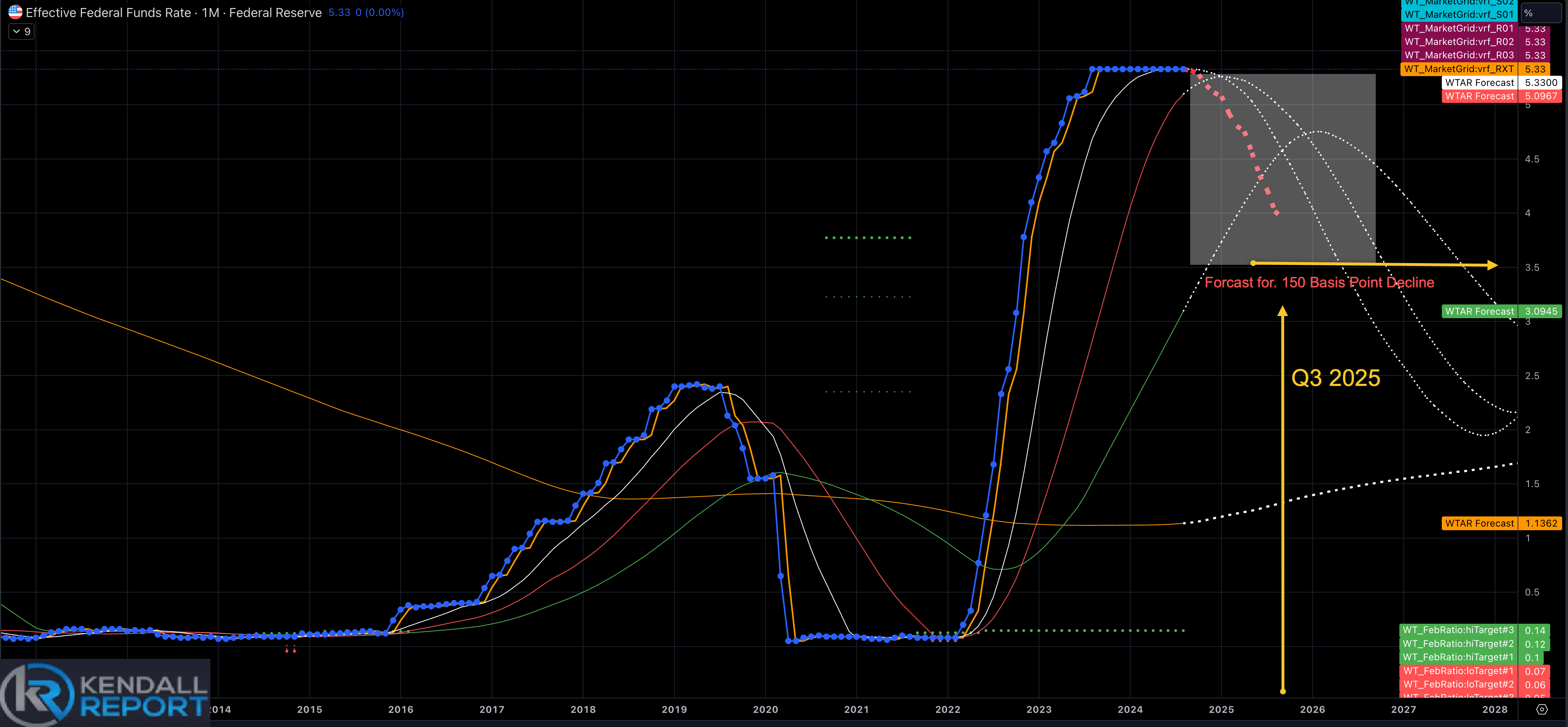

The economic data released today was particularly intriguing. Both retail sales and industrial production for August came in stronger than expected, which I see as bolstering the 'soft landing' narrative that's been gaining traction in recent weeks. This data paints a picture of an economy’s resilience despite its challenges. What's particularly fascinating is how this data interacted with market expectations for rate cuts. Despite the strong economic indicators, the CME FedWatch Tool shows a 63% probability of a 50 basis point rate cut tomorrow, up significantly from 34% just a week ago. This tells me that market participants interpret the data optimistically, believing that the Fed might see room for more accommodative policy despite robust economic activity—fat Chance, in my opinion.

The sector performance today was quite telling. The outperformance of small-cap stocks, as evidenced by the Russell 2000's 0.7% gain, suggests a growing risk appetite among investors. Furthermore, the strength in cyclical sectors like energy, industrials, financials, and consumer discretionary reinforces this risk-on sentiment. It's as if investors are positioning themselves for a continuation of economic growth, albeit with the added tailwind of potential rate cuts.

On the flip side, I couldn't help but notice the underperformance of traditionally defensive sectors like healthcare and consumer staples. This divergence further underscores the market's current bias towards growth and cyclical exposure.

Microsoft's announcement of a 10% dividend increase and a substantial $60 billion share buyback authorization also caught my attention. This move by one of the

market's most influential companies directly supported the broader market and signaled confidence in prospects. It's a reminder of the significant role that large-cap tech stocks continue to play in driving overall market sentiment.

In the bond market, I observed a slight uptick in yields, with the 10-year settling two basis points higher at 3.64% and the 2-year rising three basis points to 3.59%. Despite the strong economic data, this modest increase in yields suggests that bond traders are also factoring in the possibility of a more dovish Fed stance.

I'm preparing for potential volatility for tomorrow's Fed announcement. The market has priced in significant expectations for a rate cut, and any deviation from these expectations could lead to sharp moves in equities and bonds. I'll be paying close attention to the Fed's forward guidance rate decision and any comments on their view of the economic landscape.

In summary, today's session encapsulated the complex interplay of economic data, monetary policy expectations, and market sentiment. While the initial push to new highs reflects underlying optimism, the subsequent pullback reminds us of the cautious approach many investors take ahead of tomorrow's critical Fed decision.

· S&P 500: +18.1% YTD

· Nasdaq Composite: +17.4% YTD

· Dow Jones Industrial Average: +10.4% YTD

· S&P Midcap 400: +10.4% YTD

· Russell 2000: +8.8% YTD

Reviewing Tuesday's economic releases:

August Retail Sales came in at 0.1% (KR Forecast consensus -0.2%), with the prior month revised to 1.1% from 1.0%. August Retail Sales excluding auto were 0.1% (KR Forecast consensus 0.2%), compared to the previous 0.4%.

The key takeaway from this report is the robust performance of control group sales, which are factored into GDP calculations. These sales increased by 0.3%, following an upwardly revised 0.4% increase in July (previously reported as 0.3%) and a 0.9% increase in June. These figures strongly contradict any notion of a hard landing for the economy.

August Industrial Production showed a significant increase of 0.8% (KR Forecast consensus 0.1%), with the prior month revised to -0.9% from -0.6%. August Capacity Utilization rose to 78.0% (KR Forecast consensus 77.9%), with the prior month revised to 77.4% from 77.8%.

The key point to note here is the strong rebound in industrial production for August, driven by manufacturing output and a substantial near 10% increase in the motor vehicles and parts index. This bounce-back follows July's depressed figures due to Hurricane Beryl's impact.

July Business Inventories increased by 0.4% (KR Forecast consensus 0.4%), up from the prior 0.3%.

The September NAHB Housing Market Index rose to 41 (KR Forecast consensus 41), up from the prior reading of 39.

Looking ahead to Wednesday's economic calendar:

- 7:00 ET: We'll see the release of the Weekly MBA Mortgage Applications Index

- 8:30 ET: August Housing Starts and Building Permits data will be published

- 10:30 ET: The Weekly EIA Crude Oil Inventories report will be released

The main event tomorrow, however, will be the Federal Reserve's policy decision, scheduled for 2:00 ET. This announcement will likely be the focal point for market participants, potentially overshadowing the day's earlier economic releases.

Also, I will be doing a Livestream at 1:30 EST on The Kendall Report on YouTube.

WaveTech Database