Final Quarter How will the Year End?

KR Opinion

As we begin this week, we witnessed some early softening in the markets on Monday. However, as we entered the final hour of trading, which marked the end of the month and the quarter, we saw significant window dressing and buying activity. This late surge pushed the market to new session highs. The buying momentum continued briefly after the market closed, but we now see a return to stability. Overall, the patterns we're observing continue to maintain a bullish stance.

Looking ahead to Wednesday's ADP numbers and throughout the week, we will likely see a continuation of this choppy pattern. Tuesday will bring the JOLTS (Job Openings and Labor Turnover Survey) numbers, providing insight into the current employment scenario. This has weakened over the past several months, with the last report showing 7.6 million job openings. It will be interesting to see if this number changes significantly.

A critical development I've been discussing for several days has become official: the longshoremen's strike. The potential impact is substantial, with estimates suggesting that one day of strike could equal one week of delay in shipping. If this holds true, it won't take long for serious backlogs to develop. There doesn't appear to be much movement towards any type of settlement.

Even if the Taft-Hartley Act is invoked, forcing workers back for 90 days, it's likely they won't be working at full speed. For those who saw my YouTube video featuring the union boss's message, it's clear that these workers are prepared for a prolonged strike. They're demanding a 76% wage increase, which seems extraordinarily high. While longshoremen have traditionally earned decent wages, a 76% increase appears out of line, especially considering that West Coast workers recently secured a 36% increase.

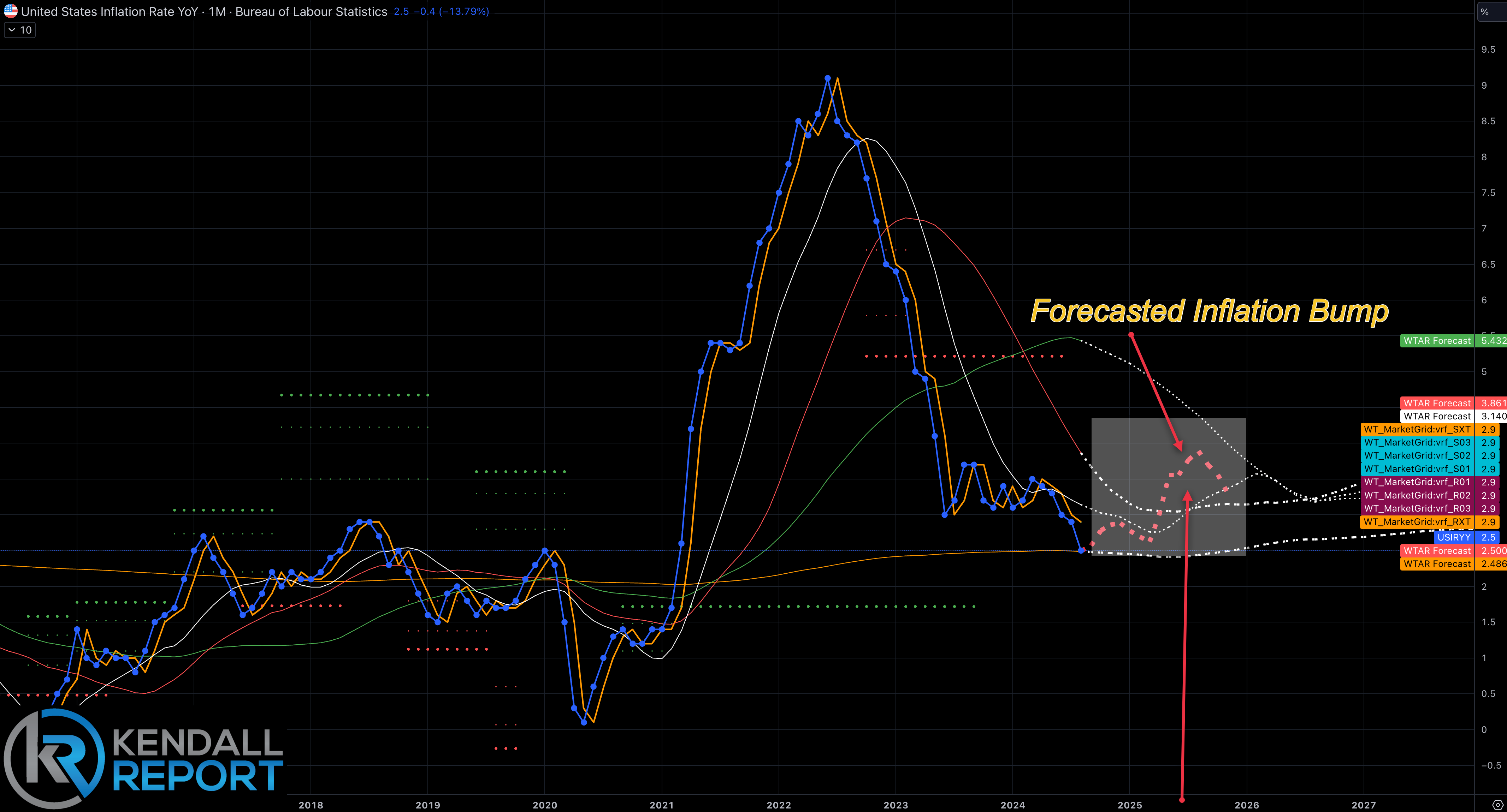

The union's stance, as evidenced in their public messages, doesn't appear very flexible at the moment. This situation is likely to play out as I discussed in yesterday's report, with potentially devastating scenarios starting to stack up. We might see a bounce in inflation, although this would likely be a bit down the road. I've been discussing an "echo bounce" in inflation for several months, and this strike situation could be the catalyst for such an event.

Despite these concerns, I see a broad market trading range. The database indicators remain solid, so I don't anticipate any major declines. However, we certainly have plenty of interesting news to be released this week, including employment numbers and manufacturing data, which could affect short-term sentiment.

We saw interest rates increase yesterday following Jerome Powell's comments that the Fed would not be moving too quickly on rate cuts. Despite this, the markets are still pricing in a 65% chance of a 50 basis point drop. I'm leaning more towards an incremental 0.25% drop, potentially in November. However, I think November could be a "skip" meeting with no rate changes, with cuts starting in December and proceeding methodically at quarter-point intervals all the way into Q2 of 2025.

Looking Back on Monday’s action

The stock market had a relatively calm trading day, capping off a strong third quarter with a late rally. Earlier in the day, losses were modest, with the market reaching its lowest point around 2:30 p.m. ET.

This dip came after Federal Reserve Chair Powell's remarks at an NABE Conference, where he indicated that two more 25 basis point rate cuts could be implemented this year if the economy progresses as expected. This statement caused some brief selling pressure, as the market had anticipated 75 basis points in cuts before year-end.

In response to Powell's comments, Treasury yields increased, with the 2-year note yield rising nine basis points to 3.65% and the 10-year note yield climbing five basis points to 3.80%.

However, the market quickly rebounded, buoyed by the understanding that the Fed would still be cutting rates and could act more aggressively if needed. This reaction demonstrated the persistence of the "Fed put" mentality, combined with the successful "buy-the-dip" strategy that has been prevalent throughout the year.

The S&P 500 reached its session highs just before the close, ending the third quarter positively. While not as dramatic as the 8.1% gain seen in China's Shanghai Composite (driven by reports of the People's Bank of China instructing commercial banks to lower mortgage rates), it was still impressive. The market-cap-weighted S&P 500 gained 5.5% for the quarter, while the equal-weighted S&P 500 rose 9.1%.

Sector performance was mixed throughout the day but turned largely positive by the close—nine of the eleven S&P 500 sectors finished with gains ranging from 0.1% to 0.8%. The materials sector (-0.6%) and consumer discretionary sector (-0.3%) were the only decliners, with Amazon.com's 0.9% loss weighing on the latter.

The communication services sector (+0.8%) benefited from gains in Alphabet (+1.2%) and Meta Platforms (+0.9%) while also digesting significant M&A news in the industry. This included DIRECTV's acquisition of EchoStar's video distribution business, AT&T's sale of its remaining stake in DIRECTV to TPG, and Verizon's agreement with Vertical Bridge regarding wireless communications towers.

The energy sector (+0.8%) also performed well, influenced by a Washington Post report about Israel informing the U.S. of plans for an imminent and limited ground operation in Lebanon.

Overall, the day's trading reflected a resilient market responsive to economic signals and geopolitical developments.

·Nasdaq Composite: +21.2% YTD (+2.6% for Q3)

·S&P 500: +20.8% YTD (+5.5% for Q3)

·Dow Jones Industrial Average: +12.3% YTD (+8.2% for Q3)

·S&P Midcap 400: +12.2% YTD (+6.6% for Q3)

·Russell 2000: +10.0% YTD (+8.9% for Q3)

Monday's economic data review:

The September Chicago PMI reported at 46.6, slightly above the KR Forecast consensus of 46.2 and the August reading of 46.1. While this indicates a marginal improvement, it's important to note that any reading below 50.0 signifies a contraction in manufacturing activity. Thus, the Chicago Fed region's manufacturing sector continued to contract in September, albeit slightly slower than in August.

Tuesday's economic calendar:

September Final S&P Global US Manufacturing PMI

- Release time: 09:45 ET

- Previous reading: 47.9

September ISM Manufacturing PMI

- Release time: 10:00 ET

- KR Forecast consensus: 47.7%

- Previous reading: 47.2%

August JOLTS - Job Openings

- Release time: 10:00 ET

- Previous reading: 7.673 million

August Construction Spending

- Release time: 10:00 ET

- KR Forecast consensus: 0.1% increase

- Previous reading: 0.3% decrease

WaveTech Database

Keep reading with a 7-day free trial

Subscribe to The Kendall Report to keep reading this post and get 7 days of free access to the full post archives.