I'm Back...Free Edition!

"The Fed Meeting Will Be Boring - It's What Happens in Q4 That Matters"

KR Opinion

Brief announcement: I'm back online after my absence and will be rolling out some new ideas I've developed. Tonight I won't be covering the database - I'll be introducing these changes gradually throughout the week. Glad to be back and getting back into the game.

This is undoubtedly going to be an interesting week to make a comeback after spending the better part of two weeks away from the markets. There's a lot to digest with a very heavy schedule on the calendar, including the Federal Reserve decision, which clearly has a priced-in expectation of a .25 point decline in rates. These expectations have been on the books for the last several weeks, though there was previously a .50 basis point expectation that was way out of line. I certainly don't have any issues with the Fed doing twenty-five basis points, as I've been saying for the last couple of quarters that I thought they would lower at least fifty basis points this year in an effort to steepen the yield curve.

The issue that has emerged is that we've seen those expectations come into the back end of the curve as well, with the ten-year yield moving back towards the four percent level. Unfortunately, this has temporarily taken away some of the effects of the Fed's efforts, particularly regarding the steepening of the yield curve that I've been discussing. We need this steepening to have a really positive effect, especially on small-cap stocks. Even though they've looked a little better over the last several weeks, they're still not in a position for a substantial rally.

I've been talking for the better part of a year, maybe even going back two years, about the importance of the yield curve steepening, and what we're seeing right now is that it has flattened as the front end of the curve is not declining, though it will if the Fed drops twenty-five basis points. If the back end of the curve stabilizes down here, that will force the Fed to lower another fifty basis points. I expect that the back end of the yield curve will not be affected as much, although they may have already built in the expectations. The forecast on the weekly model still suggests we could see a print in the 3.90 range, though I don't believe they'll stay there very long. As we approach year-end, I think the back end of the curve will bottom and start to steepen.

The Fed seems to be, as Trump calls them, too late. Powell once again missed the opportunity to get that steepening in just by continuing to hold. Even though I would argue that from an economic standpoint, there's no reason to do it, I continue to believe that everything they're being driven by right now is the yield curve. Employment numbers have softened, but not substantially, and we're starting to see negative numbers and similar trends. I see the probabilities that employment will continue to weaken slightly, so the back end of the curve might be more sympathetic to those types of metrics if we start to see them as we enter the fourth quarter.

At the moment, I think they're still looking at this yield curve situation, and they're not really concerned about the economy softening. I have argued for the better part of two years, possibly since shortly after they started raising rates just over two years ago, that the goal was to achieve a yield curve, to get a steepening, and to normalize the interest rate market. We seem to be continuing somewhat down that path. Maybe this week's action and some of the commentary will still support this underlying tone. I'll discuss this further as we approach the meeting on Wednesday, but I believe sentiment is likely to shift, considering the potential for further softness in employment numbers and possibly some economic metrics.

The big fly in the ointment is that the tariffs aren't having the effects that everybody told us they would have, and in fact, they've been an overall positive. I think there's some genius in some of the things that Secretary Bessent is doing at the Treasury that is helping to manage the finances as well. When you see a market guy like Scott Bessent, you can see that he's having fun running the finances of the United States. It's got to be a very interesting job, but the point is that we should probably see more stability.

Unfortunately, it doesn't look like we're going to get that steepening yield curve, maybe not until next year, but I am seeing some promise in the forecast of the weekly treasuries. I won't cover them tonight, but I'll try to get them in before the Fed meeting on Wednesday to see if we can fine-tune this a little bit. It appears that by the end of the year, we'll see this pattern start to unfold sometime in November or December. As we enter 2026, I think we'll begin to see more aspects of the new economy emerge, particularly in 2026, 2027, and beyond.

Returning to this week's data, retail sales are expected to be released on Tuesday, which will have a fairly significant impact, with expectations of a 0.3% increase. Other things coming out will be industrial production and capacity utilization. They will have some effect and could slightly impact sentiment, but all eyes will be on the Fed to see what type of rhetoric they release, though I don't think there will be anything new. We do have housing starts coming out on Wednesday, along with the FOMC decision, with expectations of a quarter percent drop. Then we'll move on to Thursday with continuing claims and other similar data that will finish out the week as far as economics go.

My expectation right now is that we'll continue to stay pretty positive in the equity markets. Everything's going to be on pause until we get into Thursday, but overall, the equity markets are still forecasting higher prices. Those of you who followed the weekly sheets during the week I was going to be out of town saw that they were projecting that we would get a low and move back up and potentially go to new highs, which we have done. So, I'll dive into this week and start getting back into the market's flow, especially with the Fed meeting and all the developments that are coming out.

Week of September 15 - 19

· Sep 15

· 08:30 ET: Empire State Manufacturing For: Sep | Trading Impact: Low | KR Forecast: 6.3 | KR Cons: 3.0 | Prior: 11.9

· Sep 16

· 08:30 ET: Retail Sales For: Aug | Trading Impact: High | KR Forecast: 0.1% | KR Cons: 0.3% | Prior: 0.5%

· 08:30 ET: Retail Sales ex-auto For: Aug | Trading Impact: High | KR Forecast: 0.1% | KR Cons: 0.3% | Prior: 0.3%

· 08:30 ET: Import Prices For: Aug | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: 0.4%

· 08:30 ET: Import Prices ex-oil For: Aug | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: 0.3%

· 08:30 ET: Export Prices For: Aug | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: 0.1%

· 08:30 ET: Export Prices ex-ag. For: Aug | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: 0.1%

· 09:15 ET: Industrial Production For: Aug | Trading Impact: Medium | KR Forecast: 0.1% | KR Cons: 0.0% | Prior: -0.1%

· 09:15 ET: Capacity Utilization For: Aug | Trading Impact: Medium | KR Forecast: 77.5% | KR Cons: 77.4% | Prior: 77.5%

· 10:00 ET: Business Inventories For: Jul | Trading Impact: Low | KR Forecast: 0.1% | KR Cons: 0.2% | Prior: 0.0%

· 10:00 ET: NAHB Housing Market Index For: Sep | Trading Impact: Low | KR Forecast: 31 | KR Cons: 33 | Prior: 32

· Sep 17

· 07:00 ET: MBA Mortgage Applications Index For: 09/13 | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: 9.2%

· 08:30 ET: Housing Starts For: Aug | Trading Impact: High | KR Forecast: 1350K | KR Cons: 1375K | Prior: 1428K

· 08:30 ET: Building Permits For: Aug | Trading Impact: High | KR Forecast: 1340K | KR Cons: 1370K | Prior: 1362K

· 10:30 ET: EIA Crude Oil Inventories For: 09/13 | Trading Impact: High | KR Forecast: NA | KR Cons: NA | Prior: +3.94M

· 14:00 ET: FOMC Rate Decision For: Sep | Trading Impact: High | KR Forecast: 4.00-4.25% | KR Cons: 4.00-4.25% | Prior: 4.25-4.50%

· Sep 18

· 08:30 ET: Continuing Claims For: 09/13 | Trading Impact: High | KR Forecast: NA | KR Cons: NA | Prior: 1939K

· 08:30 ET: Initial Claims For: 09/13 | Trading Impact: High | KR Forecast: 255K | KR Cons: 245K | Prior: 263K

· 08:30 ET: Philadelphia Fed Index For: Sep | Trading Impact: Low | KR Forecast: 0.0 | KR Cons: 3.0 | Prior: -0.3

· 10:00 ET: Leading Indicators For: Aug | Trading Impact: Low | KR Forecast: -0.1% | KR Cons: -0.1% | Prior: -0.1%

· 10:30 ET: EIA Natural Gas Inventories For: 09/13 | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: +71 bcf

· 16:00 ET: Net Long-Term TIC Flows For: Jul | Trading Impact: Low | KR Forecast: NA | KR Cons: NA | Prior: $150.8B

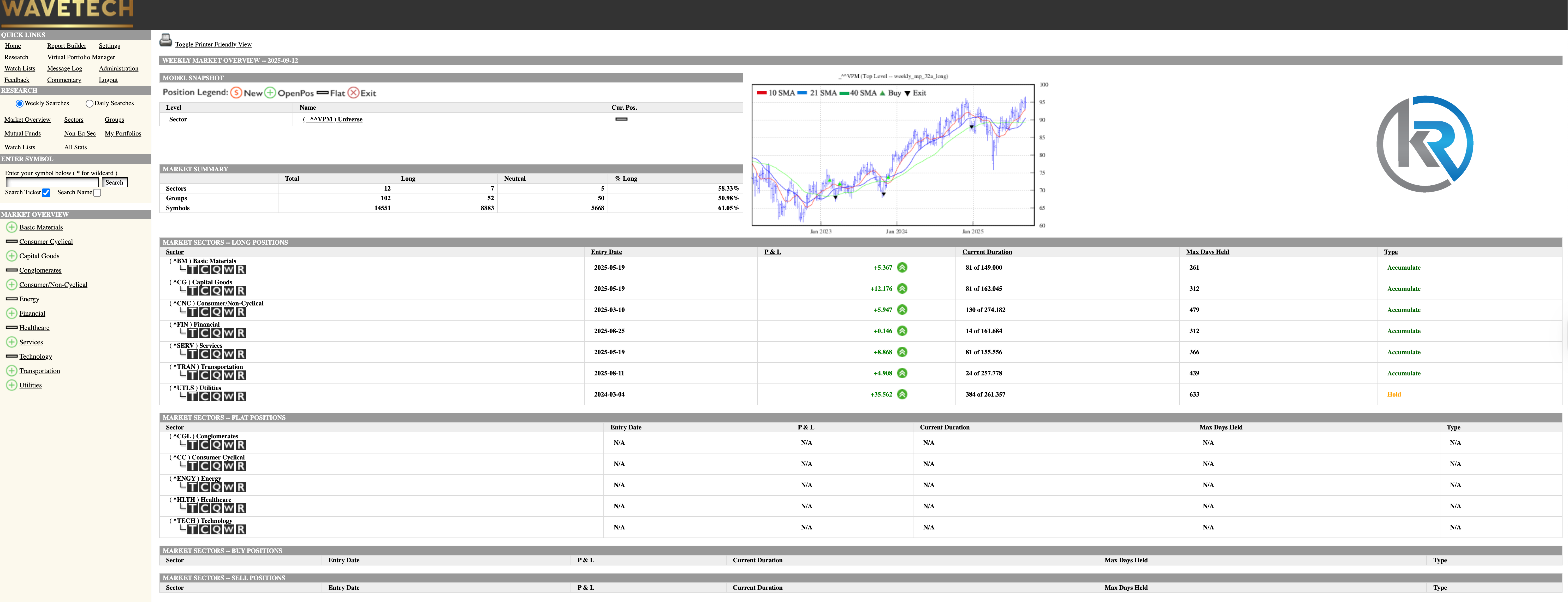

S&P 500 futures

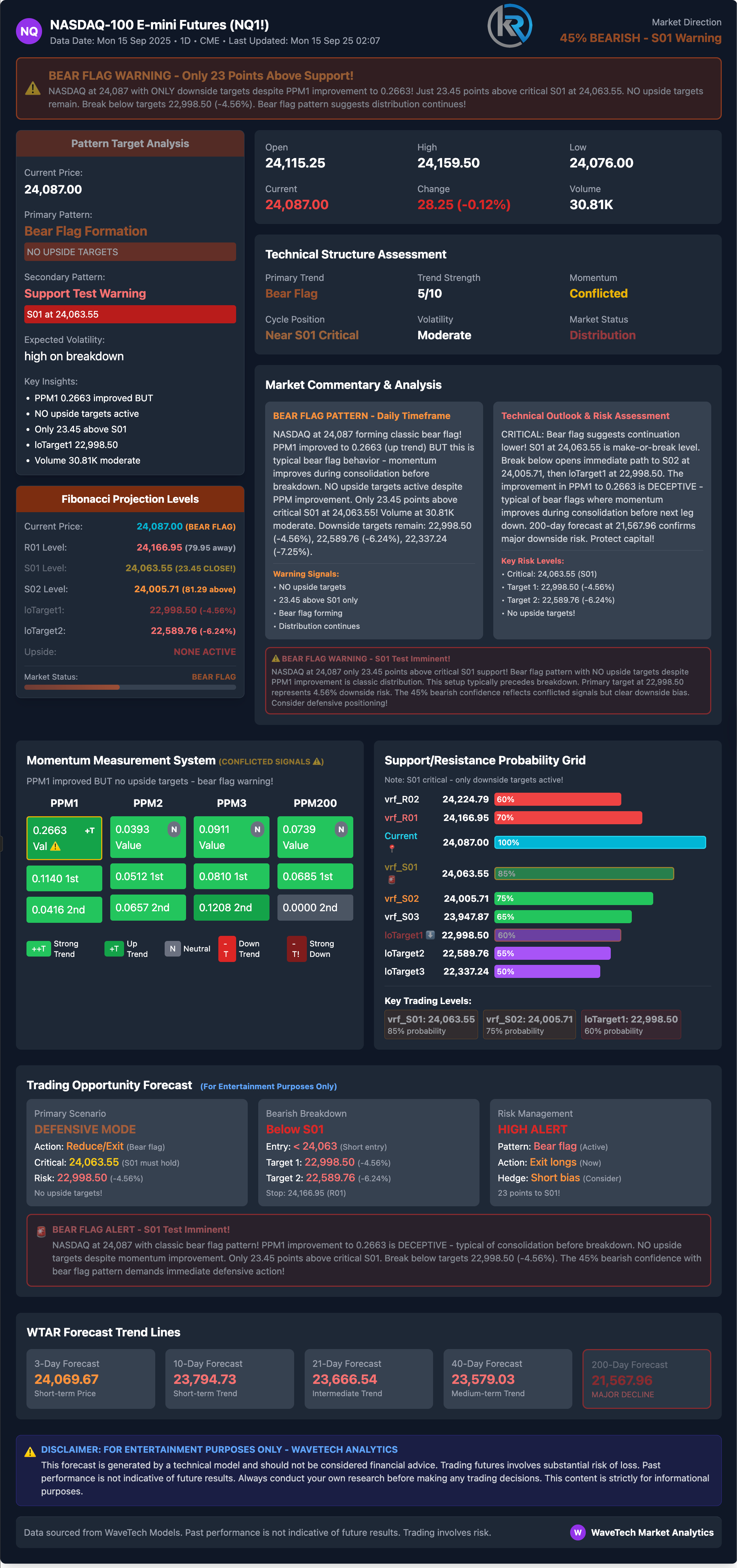

NASDAQ 100 futures

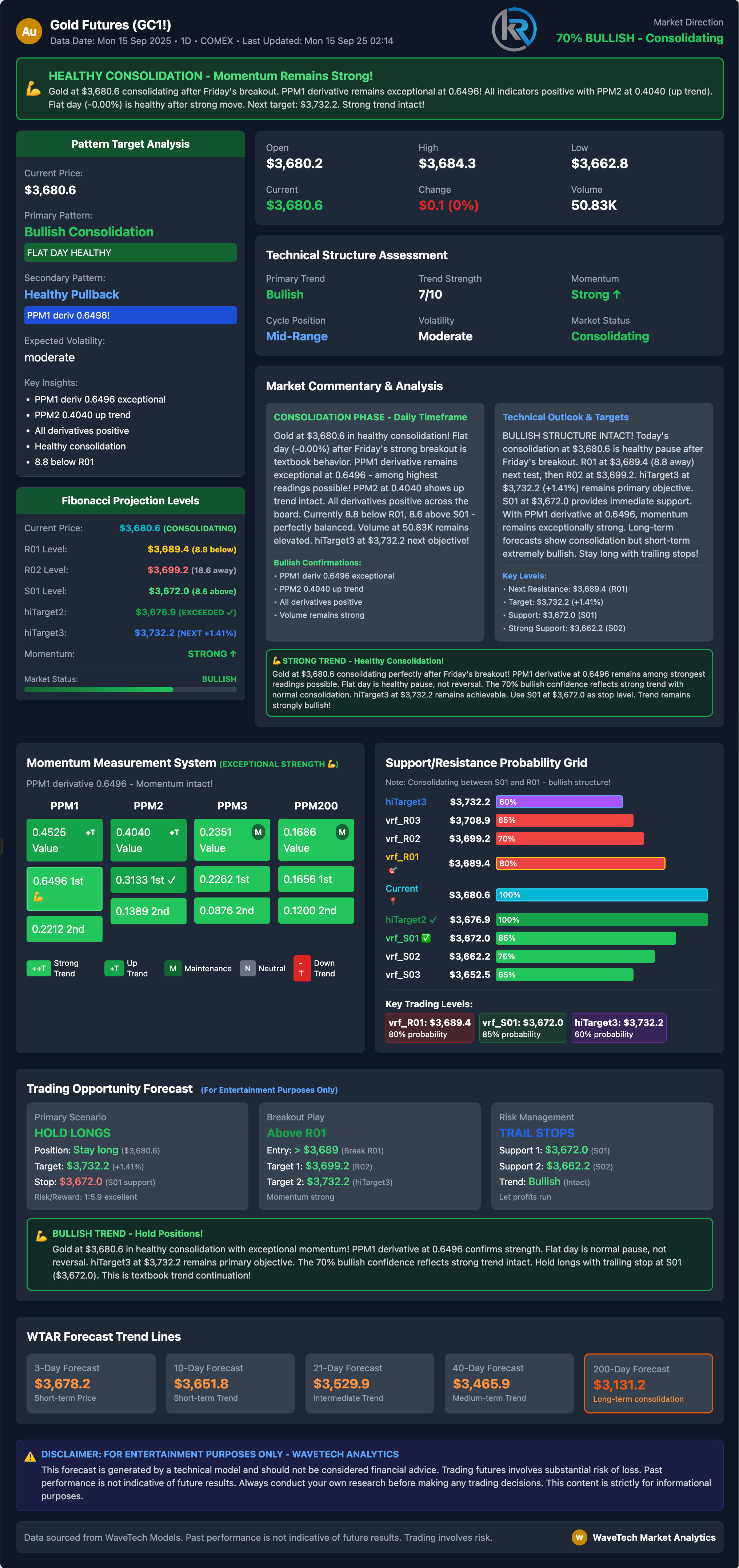

Gold

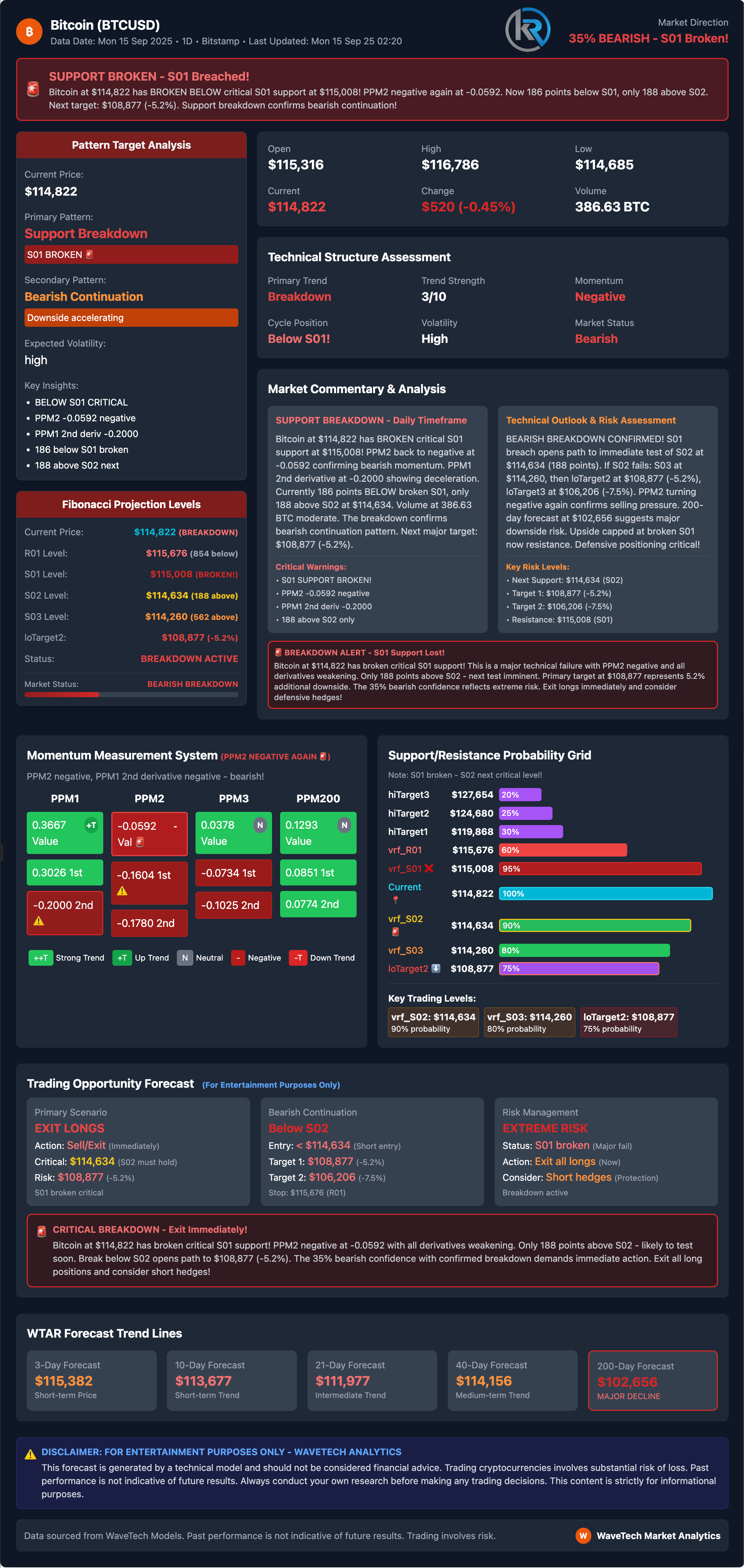

Bitcoin

Robert Kendall

Chief Analyst

"Disclaimer for “The Kendall Report

The information provided in "The Kendall Report" is for general informational and educational purposes only. The opinions, analyses, and forecasts included in this newsletter are based on the author's personal views and experiences and are provided as is without warranty of any kind.

While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, reliability, or timeliness of any information contained in this newsletter. The information presented should not be construed as financial, investment, legal, or other professional advice. It does not constitute a recommendation or endorsement of any particular investment strategy, financial instrument, product, or service.

Investors should consider their financial situation, objectives, and risk tolerance before making investment decisions based on the information provided. The financial market is subject to high risk and volatility. Past performance is not indicative of future results. Investing in the financial market involves the risk of loss, including the loss of principal.

"The Kendall Report" and its contributors will not be liable for any direct, indirect, incidental, consequential, or exemplary damages arising from the use or inability to use the information provided in this newsletter, including but not limited to losses or missed gains.

By accessing and using "The Kendall Report," you acknowledge and agree to this disclaimer and assume full responsibility for the use of the information provided. We reserve the right to make changes to the content of this newsletter at any time without notice.

This disclaimer is subject to change at our discretion, and it is the reader's responsibility to review it regularly for any updates.