Inflation Echo Bounce Coming?

KR Opinion

The start of 2025 has introduced an intriguing market dynamic, with the S&P 500 down roughly 1.8% year-to-date. Despite this relatively modest decline, there's a noticeable shift in market sentiment as investors contend with questions regarding valuations and inflation expectations. The rising yields at the longer end of the curve are especially significant, exerting increasing pressure on equity valuations.

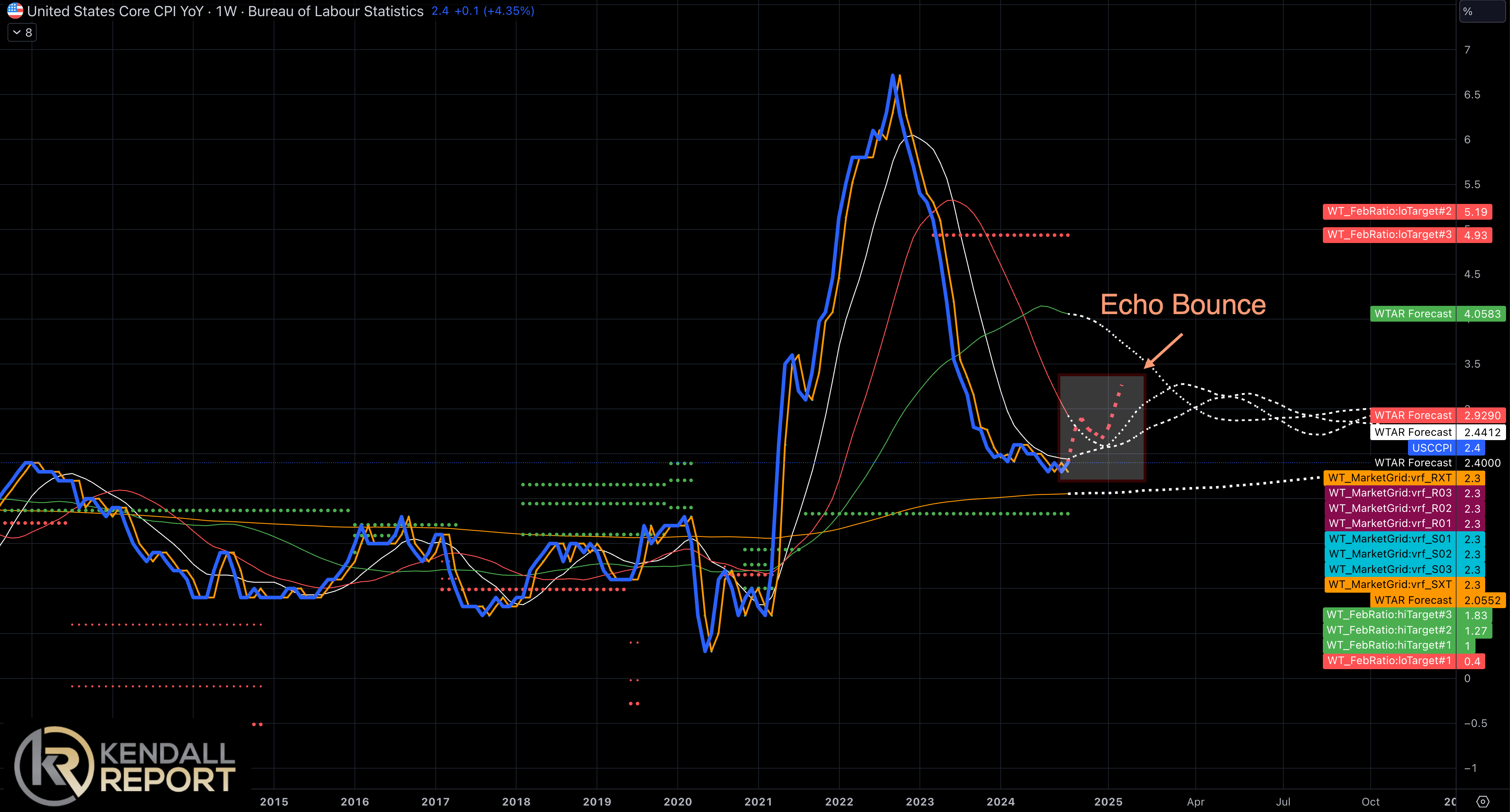

This week marks a crucial moment as PPI and CPI data releases approach. The bond market has started to factor in higher inflation expectations, with the 10-year Treasury yield indicating potential technical targets between 4.91% and 5.14% in the coming weeks. This upward pressure on yields reflects a fundamental reassessment of the Federal Reserve's expected rate path, challenging the previous market consensus regarding imminent rate cuts.

The political transition introduces an additional layer of complexity to the market narrative. While President-elect Trump's upcoming inauguration typically suggests a business-friendly environment, there are growing concerns about potential near-term disruptions. Market participants are primarily focused on proposed policy changes, particularly regarding immigration and trade, which could result in workforce disruptions and economic adjustment periods.

Last week's unexpectedly strong employment report, which indicated solid job creation, raised some questions about data quality during the administrative transition. The potential effects of upcoming policy changes, especially concerning immigration and workforce composition, could notably change these employment dynamics over the next several quarters.

The upcoming retail sales data will be particularly significant as they provide crucial insight into consumer behavior. Despite current market volatility, there are still no immediate signs of a recession. However, the second half of 2025 remains uncertain and warrants careful monitoring.

The market's technical indicators, particularly the WaveTech database, have shifted into a defensive posture, suggesting continued caution. This defensive positioning aligns with broader market sentiment as investors digest competing narratives: strong employment data, rising inflation concerns, political transition, and potential policy disruptions.

Looking ahead, this week could be pivotal in establishing market direction. Combining critical inflation data, retail sales figures, and ongoing yield curve dynamics will likely provide more precise signals about the market's near-term trajectory. Investors should prepare for continued volatility as markets adjust to these evolving economic and political realities.

Looking back on last week

The financial markets ended the week on a defensive note, primarily driven by concerns about persistent inflation and a potential delay in Federal Reserve rate cuts. Ironically, the story revolved around strong economic data that created headwinds for market sentiment.

The December employment report delivered a significant surprise, with 256,000 new jobs added to the economy—substantially exceeding expectations. While robust job creation typically signals economic health, it sparked anxiety among investors worried about stubborn inflation. The unemployment rate's decline to 4.1% further reinforced these concerns, suggesting the labor market might be too strong for the Federal Reserve's comfort.

Interest rates have played a central role in the market narrative, with the 10-year Treasury yield climbing 18 basis points to 4.78%. This surge reflects growing skepticism about the timing of potential rate cuts, especially after the December FOMC minutes were released. The Fed's message is clear: They need more confidence in inflation's decline toward their 2% target before considering rate reductions.

Adding to the complex picture, the ISM Services PMI data revealed unexpected strength in the services sector. More importantly, it showed a concerning jump in the Prices Index to 64.4%—the highest level since January 2024. This development particularly rattled markets, suggesting inflation pressures might be rebuilding rather than subsiding.

The market's response was broad-based, with the S&P 500 declining 1.9% for the week, while the technology-heavy Nasdaq Composite saw a larger decline of 2.3%. The equal-weighted S&P 500's 1.7% decrease showed that the weakness extended beyond just the largest companies. Only three sectors – health care, energy, and materials – recorded gains, while the rate-sensitive real estate sector faced the brunt of the selling pressure, plunging 4.1%.

President-elect Trump's confirmation of his tariff policies added another layer of uncertainty, particularly after speculation about possible policy adjustments. This stance, combined with the University of Michigan's consumer sentiment survey indicating increased inflation expectations, highlighted the potential for price pressures that could persist longer than anticipated.

Last week's narrative ultimately focused on a paradox: strong economic data that would usually be celebrated instead raised concerns about prolonged higher interest rates and persistent inflation. This shift in sentiment indicates that markets are entering a phase where good news for the economy might, counterintuitively, be seen as bad news for asset prices, particularly as investors adjust their expectations for Federal Reserve policy in 2025.

Economic Calendar for the week of January 13, 2025:

The week ahead brings several high-impact economic releases crucial for market sentiment, with inflation data taking center stage. The Producer Price Index (PPI) starts on January 14th, with forecasts pointing to a 0.3% increase and core PPI expected at 0.2%. These numbers will set the tone for the closely watched Consumer Price Index (CPI) release the following day.

January 15th is a pivotal day for the markets. It features the December CPI report, which KR Forecast expects will show a 0.3% increase in headline CPI and a 0.2% increase in core CPI. That same day, we will also see the release of manufacturing data through the Empire State Manufacturing Index, which is predicted to indicate a contraction of -2.0. The Federal Reserve's Beige Book will also be published, providing insights into regional economic conditions across Fed districts.

With December's retail sales data, consumer spending moves into focus on January 16th. KR Forecast projects a 0.6% increase in headline retail sales and 0.5% excluding automobiles. The labor market picture will be updated through weekly jobless claims, forecast at 212K initial claims. The Philadelphia Fed manufacturing index is expected to remain in contractionary territory at -6.0, improving from the previous -16.4 reading.

The week ends with housing sector data on January 17th. Housing starts are projected to show modest improvement to 1318K units while building permits are expected to moderate to 1454 K. These numbers will provide insight into the residential construction sector's response to recent changes in mortgage rates.

Additional weekly reports include import and export prices, business inventories, and the NAHB Housing Market Index, though these typically have a lower market impact. Energy traders will monitor the weekly EIA crude oil and natural gas inventory reports on January 15th and 16th.

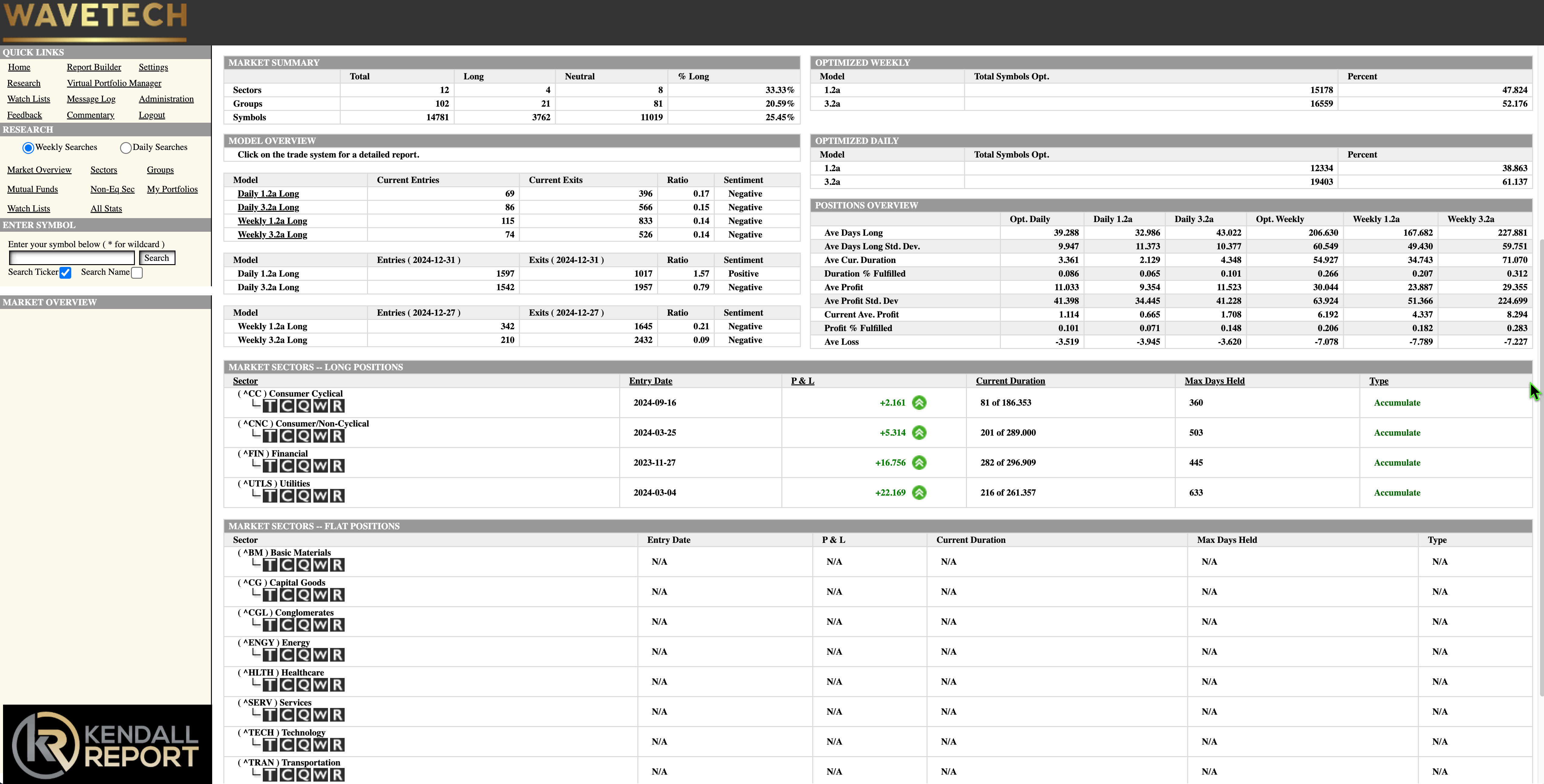

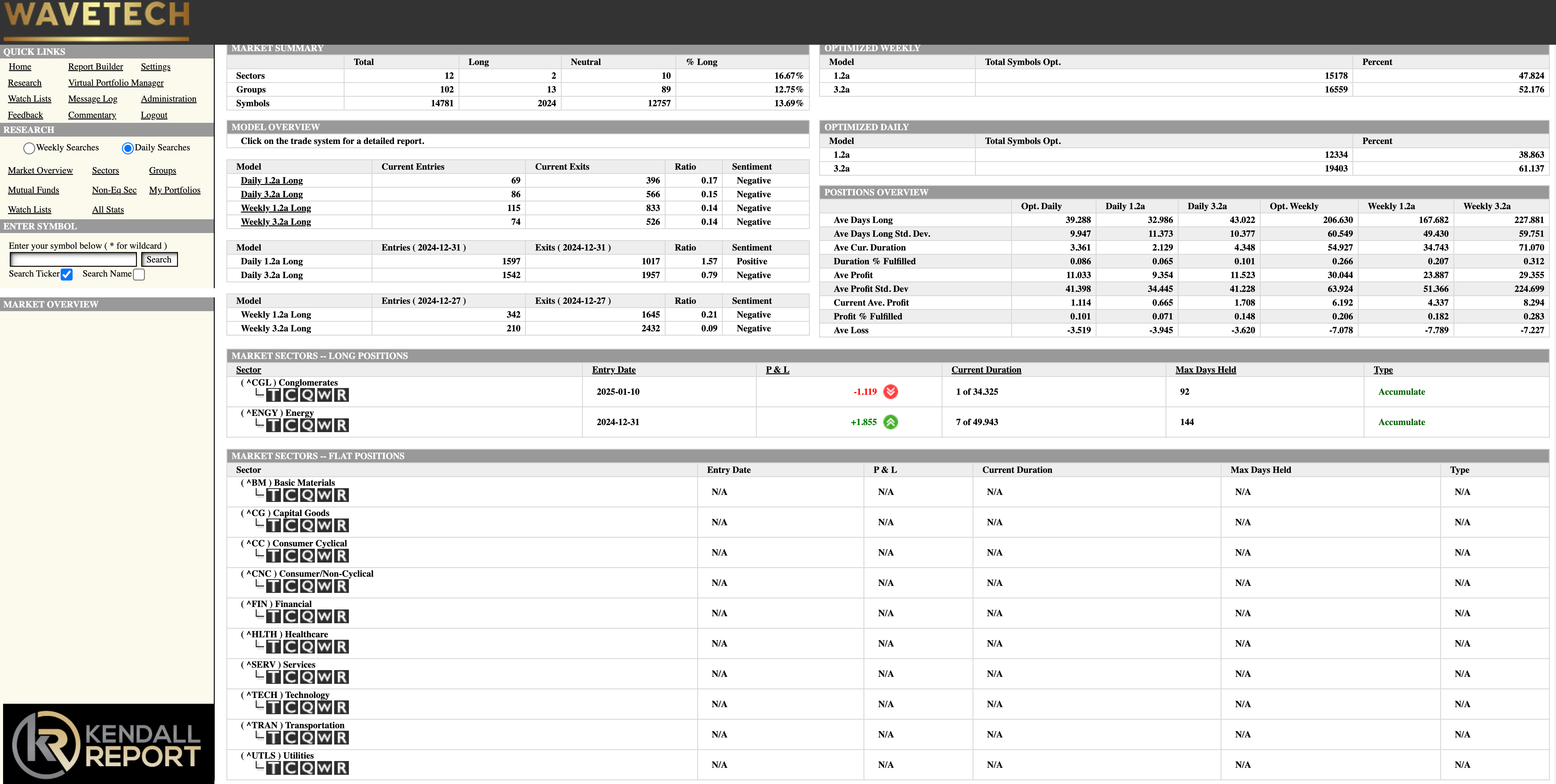

WaveTech Database

The database is exhibiting substantial technical deterioration from previously stable levels. After maintaining above 61% bullish through most of 2024, current readings have plunged to 25.43% bullish, with 70% of tracked symbols showing no discernible trend characteristics.

In the intermediate timeframe analysis, while four sectors maintain long signals, these positions stand at critical thresholds near liquidation levels. Industry group readings have contracted to just 20% bullish. This erosion pattern suggests the intermediate database could decline further toward 12% bullish readings.

The short-term database currently registers 13.5% bullish, with flow metrics showing 962 exits against only 188 new entries. More significantly, the intermediate models reflect 13,159 exits versus just 189 entries, indicating massive position liquidation across broader timeframes.

The stark imbalance between exits and entries in both short and intermediate timeframes indicates increased market choppiness with downward pressure through month-end. The sheer magnitude of exit signals, particularly in the intermediate database, suggests this technical deterioration carries significance beyond normal market fluctuations.

The systematic weakening across multiple database indicators reinforces the probability of continued technical pressure. With industry groups already showing significant weakness and sector positions approaching liquidation levels, the database metrics suggest the heightened risk of further technical deterioration in the coming weeks.

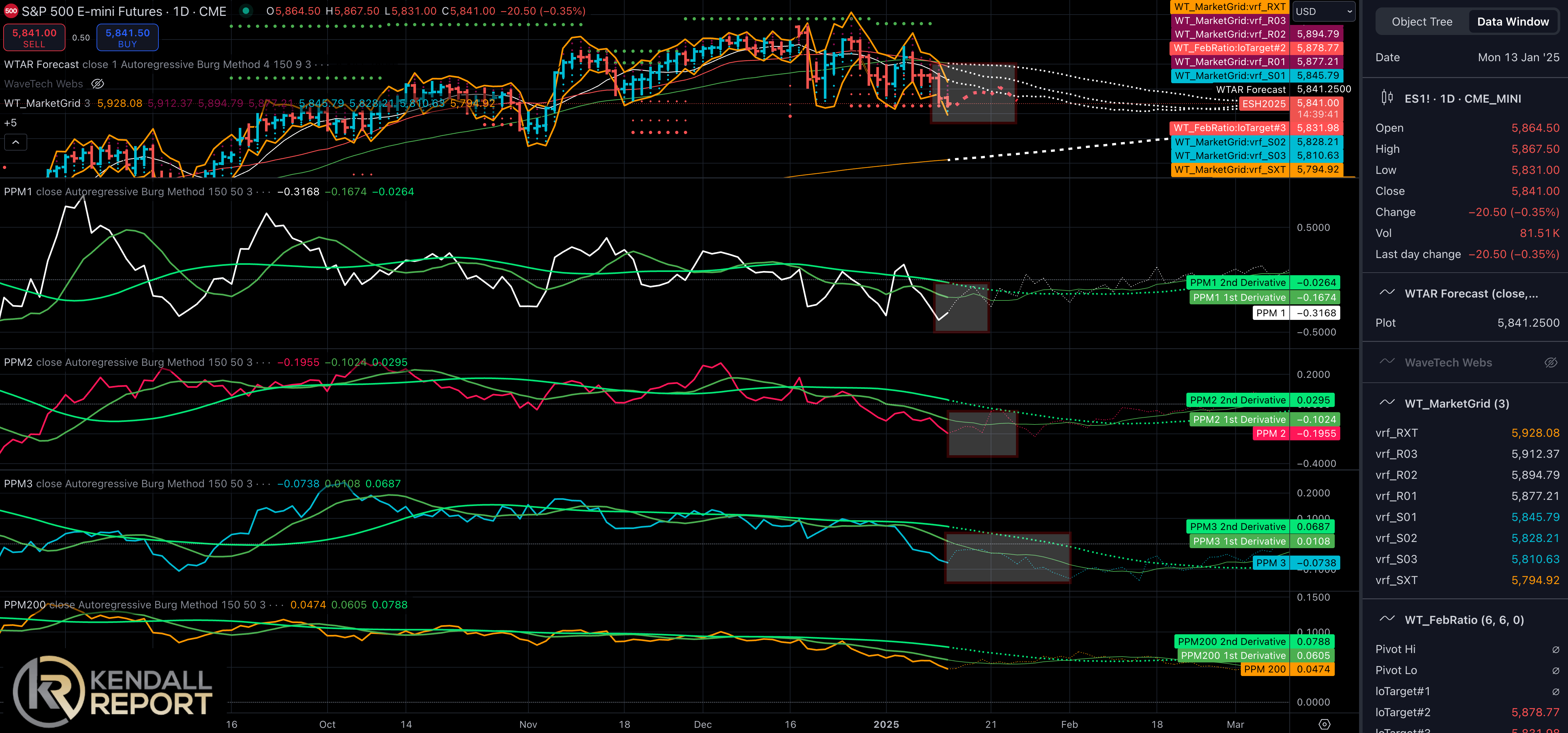

S&P 500 Futures

The daily technical readings show a newly triggered STX buy signal from Friday's action, which typically indicates a brief sideways consolidation period. The algorithmic indicators suggest the potential for a modest rebound, possibly ahead of this week's CPI and PPI reports, driven by short-covering activity.

The short-term trend has turned negative, with the price pressure momentum (PPM1) registering -0.31%. This establishes key resistance at 5938, though any bounce toward this level would represent a significant rally from current levels. Today's immediate trading range appears between resistance at 5877-5894 and support at 5845-5828.

Overnight trading has already tested the support zone, and if 5828 fails to hold, further decline toward 5810 becomes likely. The day's extreme downside target sits at 5794. The confirmed downtrend suggests continued pressure through next week and potentially month-end.

The intermediate-term charts align with this bearish bias, indicating deeper support at 5760, which could extend beyond as January concludes. The convergence of both daily and intermediate timeframe signals strengthens the likelihood of ongoing downward pressure, although short-term consolidation or minor rebounds may occur around key economic data releases.

NASDAQ Futures