Is the Inflation Cycle done?

CPI and PPI to confirm...

KR Opinion

The recent employment numbers, exceeding expectations by 100,000 jobs, have highlighted several key points. The previously anticipated 50 basis point drop in interest rates at the last meeting appears to have been politically motivated rather than economically necessary. While some aspects of the yield curve might have justified such a move, this magnitude of change is typically reserved for more volatile market conditions.

The yield curve's back end has pushed closer to 4%, reaching 3.98%, with potential upward movement. This shift is causing a market-wide reassessment of the current economic situation. The probability of a 50 basis point rate cut has essentially dropped to zero, with even a 25 basis point move now in question. The prevailing view suggests that the Federal Reserve might skip a rate change in November, initiating a series of 25 basis point cuts starting in December and continuing through mid-Q2 or into Q3 of next year.

Other market trends are also experiencing corrections. The previously popular weaker dollar trade is reversing, with a rebound in the dollar and an expected weakening of the yen. The Commodity Futures Trading Commission reported $12.3 billion in short trades against the dollar, which could lead to significant market movements if the dollar continues to strengthen.

The job report surprised many, triggering short covering in equity markets as the week closed. Despite this, the wave tech database shows remarkable strength and persistent bullish sentiment, reminiscent of the market dynamics in 2009 and 2010.

The potential resolution of the longshoremen dispute, with substantial wage increases on the table, is likely to fade as a market concern soon. The narrative of a weakening economy gives way to a more realistic expectation of a "soft landing," reinforcing the view that a recession is unlikely.

As we approach the year's final quarter and look toward 2025, market rotations are expected to continue. The upcoming election, now less than 30 days away, will likely introduce significant volatility, as seen in previous election cycles.

The economic calendar for the coming week includes the release of CPI and PPI figures, which are expected to remain relatively flat. The FOMC minutes will also be published, offering insights into the reasoning behind the recent rate decisions.

The market is poised for adjustment and potential volatility as it digests these economic indicators and geopolitical events.

Looking back on last week

The stock market experienced a tumultuous week, with most trading sessions seeing downward pressure due to profit-taking following a strong third quarter and heightened geopolitical tensions. The situation in the Middle East, particularly Iran's missile attack on Israel and Israel's vow of retaliation contributed to market unease and drove oil prices higher. West Texas Intermediate crude oil futures surged from $68.15 per barrel at the previous week's close to $74.40 by Friday, boosting the S&P 500 energy sector by 7.0% for the week.

Despite the challenges, the three major indices managed to eke out fractional gains by week's end, thanks to a Friday rally sparked by the release of the September Employment Situation Report. The report revealed stronger-than-expected hiring, decreased unemployment, and a rise in average hourly earnings, aligning with the market's preferred "soft landing" narrative. This led to a recalibration of rate cut expectations, with the likelihood of a 50 basis point rate cut at the November FOMC meeting dropping to zero, down from 32.1% on Thursday and 53.3% a week prior.

The week began with relatively modest losses on Monday as the market digested comments from Federal Reserve Chair Powell at an NABE Conference. Powell suggested that two more 25-basis point rate cuts could occur this year if the economy evolves as expected. This initially sparked some selling, but the market quickly rebounded on the understanding that rate cuts were still on the table.

Tuesday saw a weak start to the fourth quarter, with concerns about potential Iranian strikes on Israel weighing on investor sentiment. The major indices closed lower but above their worst levels for the day. Adding to the downbeat mood were growth concerns stemming from the start of a dockworkers' strike on the East Coast and Gulf Coast, as well as another contraction in the ISM Manufacturing PMI for September.

Midweek trading saw the equity market hold up relatively well, with major indices trading near their prior closing levels. The semiconductor space showed strength, providing support to the broader market. Thursday's session was characterized by hesitation ahead of Friday's employment report, with a negative bias stemming from ongoing geopolitical worries and rising oil prices.

The week concluded on a high note, with solid gains on Friday. The Dow Jones Industrial Average reached a fresh all-time high as investors responded positively to the September jobs report. The data supported the soft landing narrative while prompting a reassessment of rate cut expectations. Despite a jump in Treasury yields, buying interest in stocks persisted, particularly in the semiconductor space and among mega-cap stocks.

Throughout the week, Treasury yields moved sharply higher, with the 10-year yield jumping 23 basis points to 3.98% and the 2-year yield settling 37 basis points higher at 3.93%. The market also grappled with the temporary resolution of the dockworkers' strike, which had initially stirred growth concerns.

The week was marked by a complex interplay of geopolitical tensions, economic data, and shifting monetary policy expectations. Despite periods of uncertainty and volatility, the major indices closed the week with slight gains, demonstrating the market's resilience in the face of multiple headwinds.

Economic Releases for the Week of October 07 - 11, 2024

As we enter the second week of October, market participants are bracing for a series of critical economic reports that could shape market sentiment and monetary policy expectations.

The week kicks off on Monday afternoon with the August consumer Credit data release. While this report typically has a low trading impact, it may offer insights into consumer spending habits and overall economic health.

Tuesday brings the NFIB Small Business Optimism index, providing a pulse check on the small business sector. The August Trade Balance report will be closely watched for its potential medium impact on trading. The KR forecast suggests a slight improvement to—$71.1B from the previous—$78.8B, which could influence currency markets and trade-sensitive sectors.

Midweek, Wednesday's agenda includes the MBA Mortgage Applications Index and Wholesale Inventories, both of which offer additional context to the housing market and business activity. The EIA Crude Oil Inventories report will be crucial for energy markets, potentially causing significant price movements. The day concludes with the highly anticipated FOMC Minutes from the September meeting, which may provide valuable insights into the Federal Reserve's thinking on monetary policy.

Thursday is the busiest day, with a flurry of high-impact releases. Initial and Continuing Claims will offer the latest snapshot of the labor market. However, the spotlight will be on September's Consumer Price Index (CPI) data. With headline and core CPI forecasted at 0.1% and 0.2%, respectively, any deviation could significantly influence inflation expectations and Fed policy outlooks. The EIA Natural Gas Inventories and Treasury Budget report the day.

The week concludes with another set of crucial inflation indicators on Friday. The Producer Price Index (PPI) and Core PPI for September will be released, both forecasted at levels consistent with the previous month. These figures will be pivotal in assessing inflationary pressures at the producer level. Finally, the preliminary University of Michigan Consumer Sentiment for October will provide a timely gauge of consumer confidence, with the KR forecast slightly above the consensus at 70.3.

WaveTech Database

As we navigate the second week of October, our proprietary database reveals fascinating market dynamics characterized by rotational solid patterns and evolving trends across different time horizons.

Intermediate-Term Outlook:

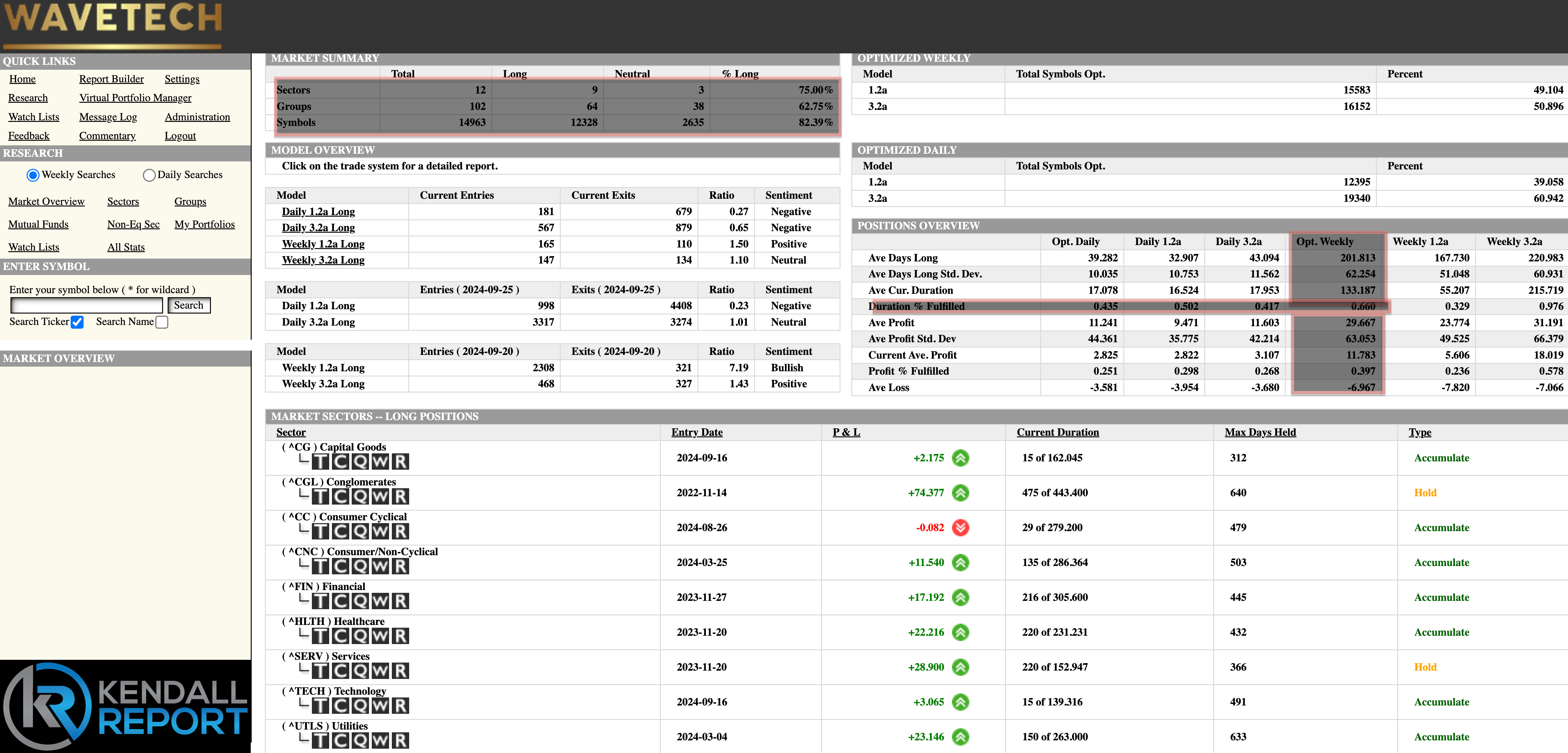

The intermediate-term database remains decidedly bullish, maintaining an impressive 82.39% bullish stance. This robust sentiment is underpinned by a healthy churn in the market, with 312 new entries balanced against 244 exits. This rotation suggests a vibrant market environment where opportunities consistently emerge across various sectors.

Sector Analysis:

Our sector-by-sector analysis on the intermediate term paints an intriguing picture. Currently, nine sectors are in an extended position, indicating broad-based strength. Only two sectors - services and conglomerates - are in an extended phase. The remaining sectors are positioned in their typical holding periods' early to middle stages. This distribution is particularly noteworthy as it suggests we're approximately 66% through the average holding duration, yet only about 40% of the potential returns have been realized. This discrepancy points to significant upside potential in the currently held positions, reinforcing our expectation of continued robust sector rotation.

Short-Term Trends:

In contrast to the intermediate-term strength, the short-term database shows signs of attrition. With 648 new entries overshadowed by 1,558 exits, the bullish percentage has declined to 65.03%. This shift in the short-term outlook may contribute to increased day-to-day volatility, even as the intermediate-term trend remains decidedly positive.

Market Pattern and Expectations:

Despite the recent achievement of slightly new highs, the market continues to pull back into an established range. We anticipate this choppy range-bound behavior to persist in the near term. However, it's important to note that the overall trend remains upward. This suggests that the longer-term trajectory remains positive, while we may see short-term fluctuations and pullbacks.

Looking Ahead:

As we move forward, the robust sector rotation is expected to continue. This rotation, coupled with the unrealized potential in current holdings, suggests that there's still significant room for returns in the symbols currently being held. Investors should remain vigilant to these rotational opportunities while preparing for potential short-term volatility.

S&P 500 Futures