Market Correction Coming?

Interest Rates Bounce back...

Special Offer: Seminar Replay Available Now!

Before diving into tonight's report, I'm excited to announce the release of the replay of the seminar I conducted last fall. If you own the indicators, this presentation is a must-watch. It's six hours of in-depth content, including edited videos and numerous illustrations for trades, understanding PPMs, and much more.

We've substantially reduced the cost, so don't miss out. Click on the graphic below to access the review page and take advantage of this offer. I hope you find it incredibly useful!

KR Opinion

As we approach Thursday, we have the usual continuing claims and initial claims data coming in, but I don't anticipate any surprises from this information. However, some out-of-cycle earnings reports are coming in below expectations, which, combined with stressors in the real estate market, is beginning to shift sentiment slightly negative.

Over the past several days, I've been discussing that algorithms indicate we are likely to test the support at the 21-day moving average for the S&P 500. For the Nasdaq, this suggests entering a corrective phase starting in early July and potentially continuing into mid-July or beyond.

We could see more substantial selling, as even the database is starting to show negative rotation again. While we're grinding near all-time highs, we might experience a bit more downward movement.

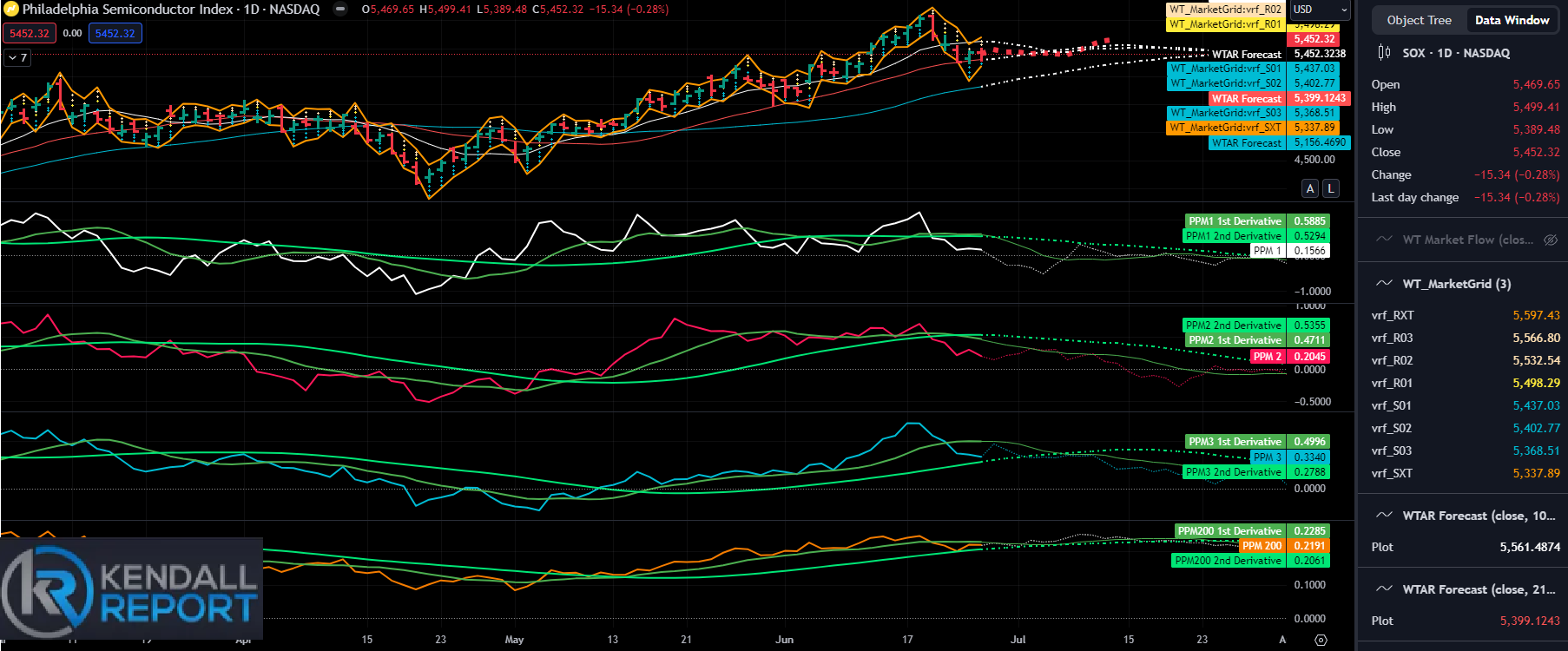

The chip sector is also under pressure. Although NVDA saw a bit of a rebound, the rest of the chip stocks were weak during Wednesday's session. We're also expecting revised GDP and deflator data, but I don't foresee any significant changes; however, there is a possibility these numbers could be adjusted down more than expected.

I am not expecting any significant declines at this time. We will enter a broader trading range with a slight bias to the downside.

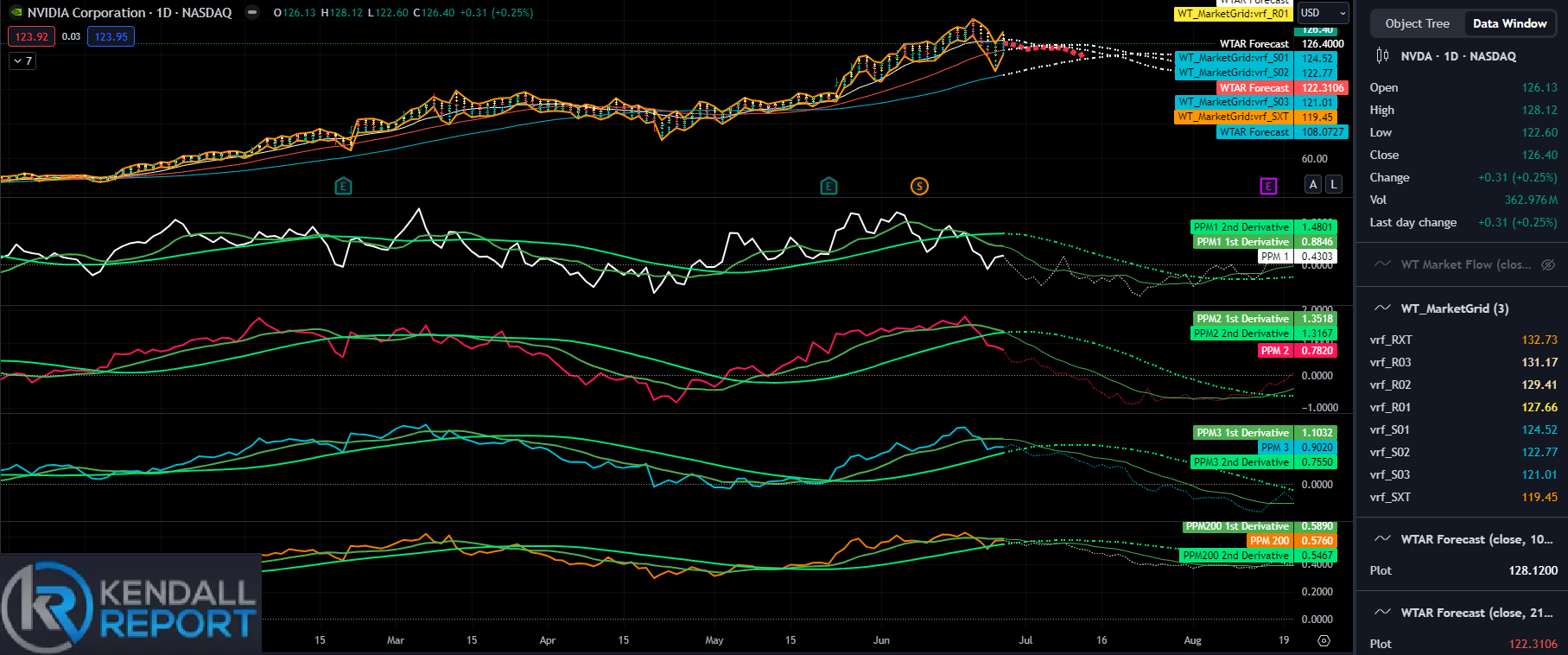

NVDA

The algorithms project NVDA lower across the board. Over the next couple of weeks, we should expect a move back to approximately 115-108. I anticipate the trading to be somewhat choppy.

If we close lower today, it could indicate the formation of a downward channel, as the market grid would turn down. Although the three-day trade was violated two days ago, we might set up a right shoulder, bringing the price down to around 110. This could erase the rally from 100 to 140 before this cycle concludes.

Preston Huang did speak at the shareholders' meeting, but his impact on the market was limited compared to Elon Musk's ability to influence stock prices. As mentioned in the opening comments, the chip sector is also under pressure, which is evident on the SOX chart below, suggesting a decline into early July.

While some stabilization is possible in the next couple of days, I believe NVIDIA will ultimately lead the sector lower. There remains significant interest in owning NVDA, so we should expect plenty of volatility in both directions as we unwind this substantial rally.

Looking back on Wednesday’s Action

The S&P 500 (+0.2%) and the Nasdaq Composite (+0.5%) closed at or near their highs for the day, following a surge of buying in mega-cap stocks during the afternoon session. The Dow Jones Industrial Average slightly increased compared to the previous day, while the Russell 2000 recorded a 0.2% decline.

Among the top performers in the mega-cap space were Apple (AAPL), closing at $213.25, up $4.18 (+2.0%); Amazon.com (AMZN) ending the day at $193.61, up $7.27 (+3.9%); and Tesla (TSLA) finishing at $196.37, up $9.02 (+4.8%). NVIDIA (NVDA) also had a significant impact, closing at $126.40 and up $0.31 (+0.3%) after initially trading down as much as 2.8% before recovering towards the end of the session.

FedEx (FDX) drew considerable attention, closing at $296.19, up $39.81 (+15.5 % %), after reporting better-than-expected earnings and indicating that demand is expected to improve through fiscal year 2025. Conversely, General Mills (GIS) was a notable underperformer, closing at $64.17, down $3.09 (-4.6 %), following a fiscal Q4 earnings report that showed a revenue miss attributed to lower prices and volumes.

Despite the positive movements in certain stocks, the market had an underlying negative bias. Decliners outnumbered advancers by roughly a 4-to-3 margin at the NYSE and Nasdaq.

Treasury yields contributed to the downside bias in equities. The yield on the 10-year note increased by eight basis points to 4.32%, and the yield on the 2-year note rose by two basis points to 4.32% despite a substantial $70 billion 5-year note sale. Additionally, the market was processing a below-consensus New Home Sales report for May.

The equal-weighted S&P 500 experienced a 0.4% decline, with eight out of the 11 S&P 500 sectors closing lower. The financial sector was among the worst performers, down 0.5%, while the consumer discretionary sector led with a 2.0% gain.

·Nasdaq Composite: +18.6% YTD

·S&P 500:+14.8% YTD

·S&P Midcap 400: +4.7% YTD

·Dow Jones Industrial Average: +3.8% YTD

·Russell 2000: -0.4% YTD

Reviewing Wednesday’s Economic Releases:

- Weekly MBA Mortgage Applications Index: 0.8% (prior: 0.9%)

- May New Home Sales: 619K (KR Forecast consensus: 650K); prior was revised to 698K from 634K.

The key takeaway from the report is that new home sales activity slowed in May. However, after considering the upward revision to April sales, the combined two-month period was better than the consensus estimate for May (650,000) and the original report for April (634,000). Despite this, higher mortgage rates and elevated prices continue to pressure new home sales, which are down 16.5% year over year.

Thursday's Economic Releases:

- 8:30 ET:

- May advance goods trade balance (prior: -$99.4 billion)

- Advance Retail Inventories (prior: 0.7%)

- Advance Wholesale Inventories (prior: 0.2%)

- Weekly Initial Claims (KR Forecast consensus: 238,000; prior: 238,000)

- Continuing Claims (prior: 1.828 million)

- May Durable Orders (KR Forecast consensus: -1.2%; prior: 0.7%)

- Durable Orders ex-transportation (KR Forecast consensus: 0.2%; prior: 0.4%)

- Q1 GDP – third estimate (KR Forecast consensus: 1.3%; prior: 1.3%)

- Q1 GDP Deflator – third estimate (KR Forecast consensus: 3.1%; prior: 3.0%)

- 10:00 ET:

- May Pending Home Sales (KR Forecast consensus: 2.3%; prior: -7.7%)

- 10:30 ET:

- Weekly natural gas inventories (prior: +71 bcf)

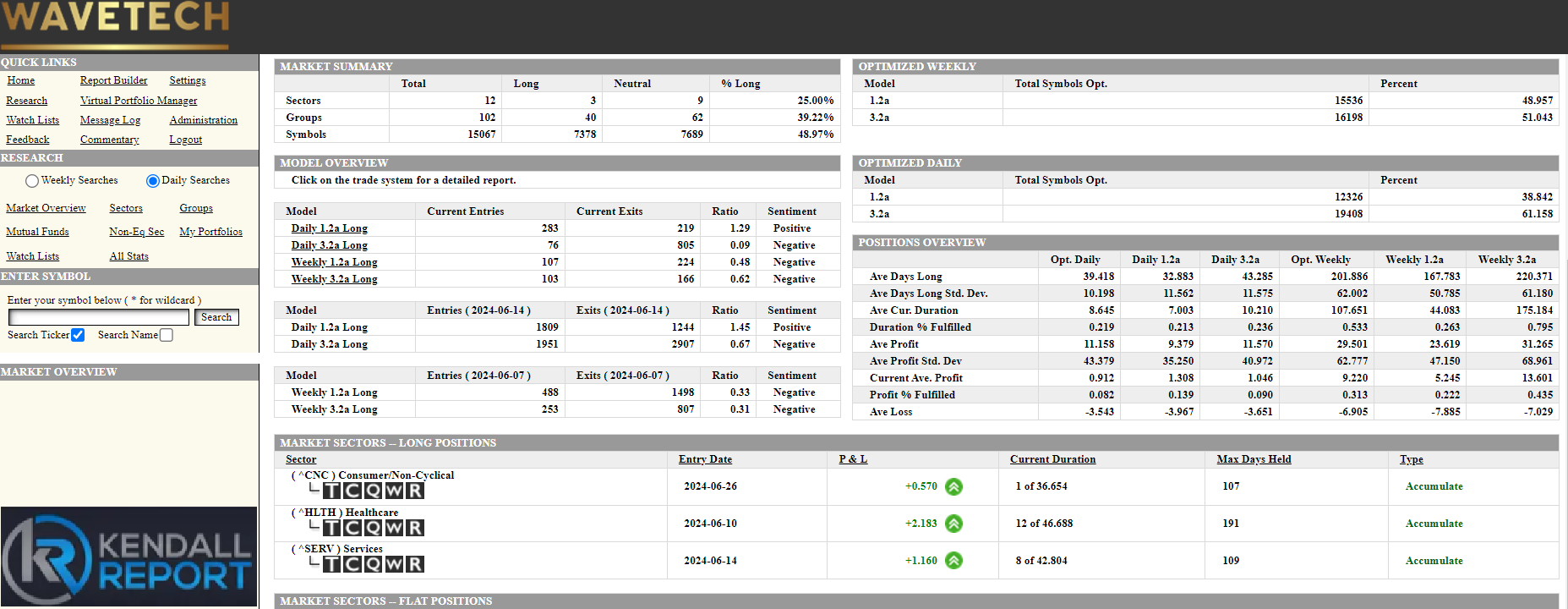

WaveTech Database

The database continues to exhibit choppy trading patterns. Although it appeared we were stabilizing above the 50% bullish level, we have now dropped back to 48.97% bullish. While this is not disastrous, it indicates ongoing rotation in the market.

There has been a slight increase in conglomerate participation on a sector basis, suggesting a minor expansion in sector involvement. However, this change is not particularly significant.

As we approach the end of the week, if we observe further downside in the major indices, we will likely see some of the selling pressure I have been anticipating reflected in the intermediate database. I will provide more updates on this as we approach Friday.

S&P 500