Market Rebound... But?

Bitcoin Gets Ready and Assault on 100k

KR Opinion

Cross Currents and Consolidation Phase Ahead

The markets reveal interesting patterns as we approach year-end, with several key trends that warrant careful attention. The energy sector is showing renewed strength, while healthcare faces potential headwinds amid speculation about RFK Jr.'s possible appointment as Secretary of Health and Human Services under the incoming administration.

Looking at the broader picture, we're entering what appears to be a six-week period of portfolio repositioning. Rather than anticipating a major downturn or dramatic reversal, technical analysis suggests we're more likely to experience a broadening trading range. Both intermediate and secular charts continue to show underlying upward momentum, though this may be tempered by increased volatility and a slight downward bias in the near term.

The housing sector will be in focus this week, though expectations suggest continuing the sideways momentum we've been seeing. The fixed-income market is particularly interesting, where we're observing noteworthy activity in the spread between 10-year and 30-year securities. Current projections indicate the potential for yields to climb another 25 to 50 basis points on the long end of the curve.

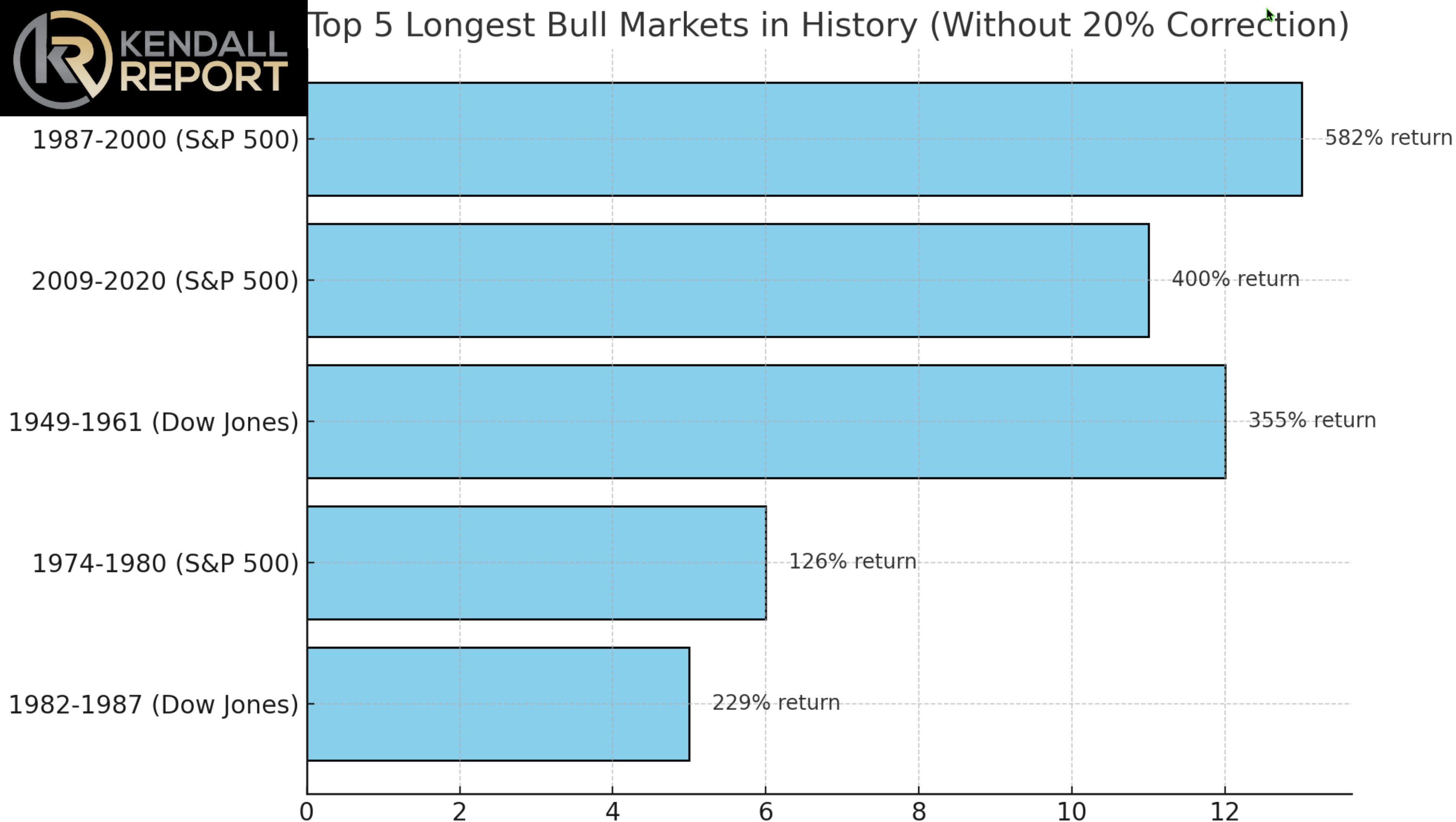

From a historical perspective, it's important to remember that bull markets can demonstrate remarkable staying power. Looking back to my market entry in 1979, we've seen several sustained bullish periods lasting anywhere from six to thirteen years without experiencing a 20% correction. The 1987-2000 rally stands as a prime example of this phenomenon.

The artificial intelligence sector continues to generate optimistic long-term expectations, with markets still processing the potential efficiencies and innovations this technology might bring. However, the immediate focus appears to be on consolidation as investors reassess sector leadership and growth trajectories.

Conclusive market direction may only be achieved well into 2025 as various economic, political, and technological factors continue to evolve. This suggests we're entering a period of strategic repositioning rather than dramatic directional moves, with opportunities arising from sector rotation and careful position management rather than broad market momentum.

This consolidation phase shouldn't necessarily be viewed as a warning sign, but rather as a natural recalibration period as markets digest recent gains and adjust to evolving economic and political landscapes. For investors, this environment demands increased attention to sector-specific opportunities while maintaining a balanced, long-term perspective.

Looking back on Yesterday

Major indices pushed higher in a positive turn for Wall Street today as Treasury yields retreated from their overnight peaks. The S&P 500 advanced 0.4%, the tech-heavy Nasdaq Composite gained 0.6%, and the small-cap Russell 2000 edged up 0.1%. After reaching nearly 4.50% overnight, the 10-year Treasury yield settled at 4.41%, down one basis point from Friday's close.

Investors showed a renewed appetite for stocks that had pulled back during last week's post-election consolidation. The market favored mega-cap technology stocks and semiconductor companies, though NVIDIA proved an exception. The chip giant's shares declined 1.3% following reports in The Information about potential overheating issues with its AI chips. All eyes remain on NVIDIA as it prepares to release earnings after Wednesday's closing bell.

Tesla emerged as a standout performer, surging 5.6% on Bloomberg's report that the Trump administration might ease regulations on self-driving vehicles. The electric vehicle maker's stock has now soared an impressive 37.8% since November 5, helping drive the S&P 500 consumer discretionary sector up by 0.9%.

Energy stocks led sector gains, rising 1.0% as commodity prices strengthened. WTI crude oil jumped 3.2% to close at $69.18 per barrel, while natural gas prices climbed 5.3% to settle at $2.97.

The day's advance showed broad market participation, with nine of eleven sectors finishing higher than their Friday closes. The healthcare sector remained flat, weighed down by Eli Lilly's 2.6% decline following reports that some Republican Senators might support Robert F. Kennedy Jr.'s potential nomination for Secretary of Health and Human Services.

This rally indicates that investors should remain optimistic despite recent market volatility. However, they continue to monitor Treasury yields and upcoming corporate earnings reports for further direction.

Today's economic data included the November NAHB Housing Market Index, which rose to 46 in November from 43 in October.

Looking ahead to Tuesday, the October Housing Starts and Building Permits report will be released at 8:30 ET.

Nasdaq Composite: +25.2%

S&P 500: +23.6%

S&P Midcap 400: +15.5%

Dow Jones Industrial Average: +15.1%

Russell 2000: +13.8%

WaveTech Database

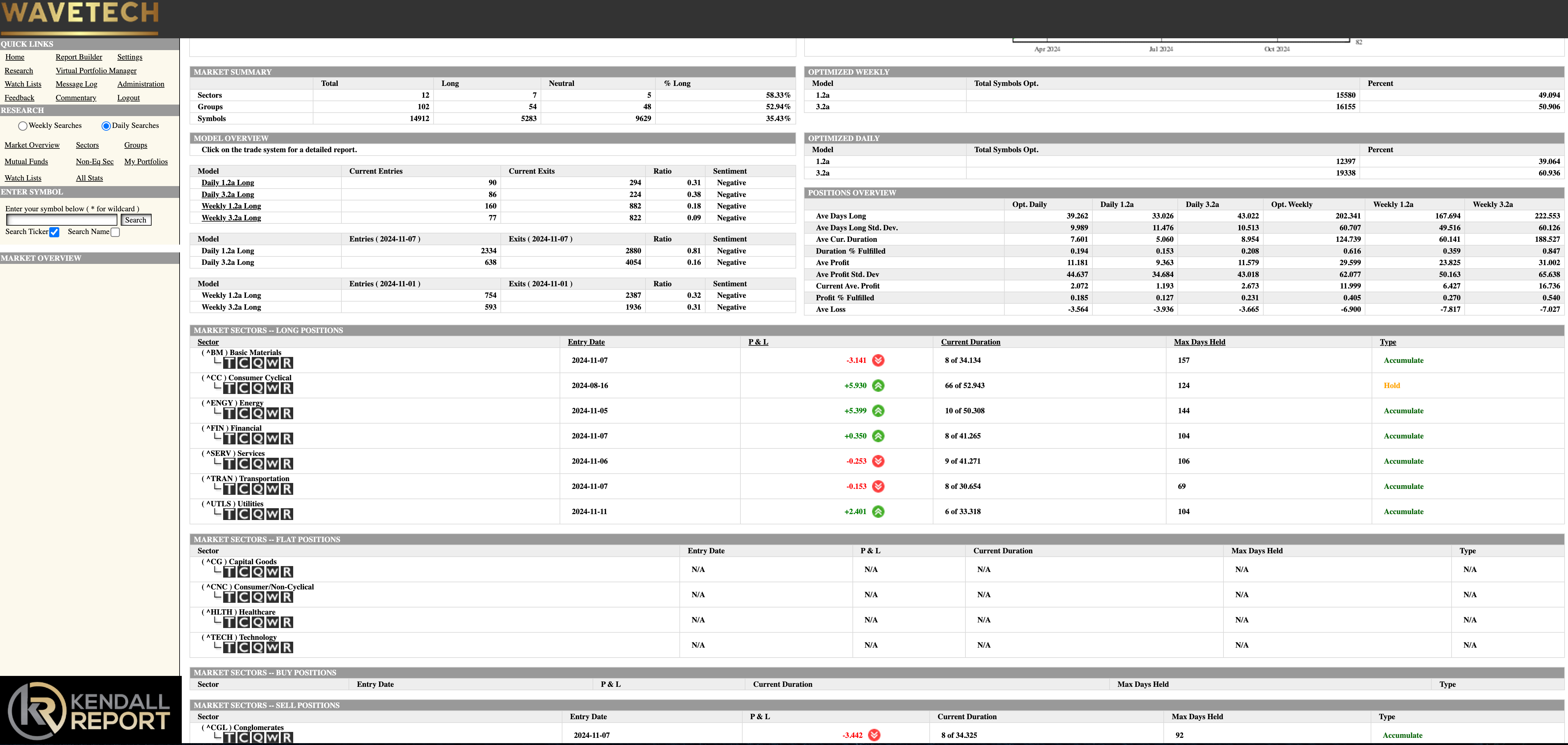

Our quantitative database metrics show deteriorating market breadth, with a net negative shift as 528 stocks moved below their model thresholds while only 176 crossed above. This movement has reduced our aggregate bullish indicator to 35.43%, suggesting weakening market participation across our measured universe.

Quantitative modeling highlights 28% as a crucial statistical threshold for our bullish indicator. A decline below this level would trigger several risk models and indicate an increased probability of short-term market weakness. However, our current factor analysis suggests we're more likely to enter a consolidation phase over several subsequent trading sessions.

Our event-driven models aren't flagging any significant catalysts in the immediate term that would typically generate heightened volatility measures. Based on our cross-asset correlation matrices and factor exposures, the current market configuration points toward continued rotational price action rather than directional momentum.

This market behavior aligns with typical transitional periods in our historical databases, where individual security and sector factor rankings become more significant drivers than broad market beta exposure. For portfolio managers, this environment typically demands increased attention to factor tilts and may present opportunities through targeted factor rotation rather than directional market positioning.

While the declining bullish percentage raises some concerns in our risk models, it should be contextualized within normal statistical ranges for consolidation periods following sustained advances. The 28% threshold represents a key level in our probability models, and movement around this area could provide significant signals about near-term market direction.

Current model outputs suggest maintaining balanced factor exposures, with particular attention to sector and style rotation effects. The grinding price action we observe typically registers in our models as a consolidation phase, often preceding more decisive directional moves once new factor leadership emerges.

Our risk models suggest that trading strategies during such periods benefit from reduced position sizing and increased focus on relative value opportunities rather than directional beta exposure. Risk management protocols become especially critical during these transitional market phases, as factor correlations can shift rapidly.

This analysis synthesizes signals from our momentum, volatility, correlation, and factor models to comprehensively view current market conditions and potential inflection points ahead.

S&P 500 Futures