Markets Reject... No Top yet!

Bitcoin to move to 73,500

KR opinion

Reviewing the market's recent behavior, I'm struck by how accurately yesterday's report anticipated the market's inability to follow through on its new highs. Indeed, we saw a notable rejection from those peak levels yesterday. However, it's crucial to understand that this pullback doesn't appear to be the beginning of a more significant downward move.

Let me explain the technical signals we're seeing. We received an RTX sell signal on Monday, which suggests some short-term weakness. Interestingly, this was followed by an STX buy signal on Tuesday. Combining these signals points to a sideways pattern for at least one day. This conflicting information is quite telling - it suggests that the market is becoming increasingly range-bound, getting locked into tighter patterns.

It's important to note that the underlying trends remain positive despite some visible deterioration. We have yet to hit that critical breaking point. This resilience in the face of short-term weakness is crucial to watch.

One of the more intriguing developments from yesterday's session was the performance of small-cap stocks. The small-cap asset class stood out as the only sector or asset class closed in positive territory, while other indices were uniformly down. While it's just one day of outperformance, I'm closely monitoring this. I'd like to see if we're witnessing the emergence of a new pattern.

However, I want to caution against reading too much into this single day of small-cap outperformance. My analysis suggests that small-cap stocks still have considerable ground to cover before they're in a position to break out and make a substantial upward move. We're seeing a brief period of relative strength, possibly lasting a day or two. It's premature to declare this the start of a new trend or to expect a repeat of the scenario we saw a couple of months ago when small-caps were leading the market higher.

I anticipate choppier, range-bound activity as we approach Wednesday's trading session. This expectation is based on the conflicting technical signals we've received and the overall market environment we're currently navigating.

To expand on this outlook, several factors are at play. First, we're in the heart of earnings season, which often increases volatility as the market digests company-specific news. Second, we're seeing mixed economic data, creating some uncertainty about the pace of economic growth and the future path of monetary policy.

Additionally, geopolitical tensions and ongoing discussions about fiscal policy in Washington add complexity to the market environment. These combined factors likely contribute to the tighter trading ranges we're observing.

It's also worth noting that as we approach the year's final months, we often see changes in market dynamics. Some institutional investors may begin positioning for year-end, while others might be looking to lock in gains from a strong year for many market areas.

In this context, the behavior of small-caps becomes even more interesting. If we see sustained outperformance from this group, it could signal a broader risk-on sentiment in the market. However, given the challenges facing smaller companies—including potentially higher borrowing costs (long end of the yield curve) and economic uncertainties—any such move would need to be confirmed over a more extended period.

For now, nimble trading and careful risk management seem prudent in this somewhat choppy market environment.

Looking Back on Tuesday’s action

I reflect on several key points in today's market action. The semiconductor sector continues to be a crucial bellwether for the broader tech industry and, by extension, the market. The sharp reaction to ASML's earnings and the potential policy changes regarding AI chip sales underscore the sector's sensitivity to both micro and macro factors. This vulnerability was demonstrated by the 5.3% drop in the Philadelphia Semiconductor Index and the 4.5% decline in NVIDIA's stock.

Earnings season is in full swing, and we're seeing significant stock moves in response to results. The 8.1% drop in UnitedHealth dragged down the entire healthcare sector and is a prime example of how individual company performances can have a broader market. Folks will be watching the mortgage app numbers that are going to be released, but I don't see anything material to pay attention to implications. This volatility will likely continue as more companies report in the coming weeks, potentially leading to further sector rotations and market swings.

The divergence between large-cap and small-cap performance today is particularly noteworthy. While the major indices like the S&P 500 and Nasdaq Composite saw significant declines, the Russell 2000 managed to eke out a small gain. If this trend persists, it could signal a shift in market leadership or changing investor risk appetites.

The bond market's reaction, while modest, also bears watching. The slight flattening of the yield curve, with the 10-year yield dipping and the 2-year yield rising slightly, could be interpreted as the market pricing in a somewhat more cautious economic outlook. Any significant moves in yields could affect equity valuations, particularly in rate-sensitive sectors.

The potential restrictions on AI chip sales to certain countries, particularly in the Persian Gulf, add another layer of complexity to the tech sector outlook. This geopolitical dimension could continue influencing market sentiment, especially for companies with significant international exposure.

Nasdaq Composite: +22.0% YTD

S&P 500: +21.9% YTD

S&P Midcap 400: +13.8% YTD

Dow Jones Industrial Average: +13.4% YTD

Russell 2000: +11.0% YTD

Reviewing Tuesday’s economic data:

October NY Fed Empire State Manufacturing came in at -11.9, significantly below the KR Forecast consensus 2.0. The prior reading was 11.5.

Looking ahead to Wednesday's economic lineup, we have several key reports to watch:

The MBA Mortgage Applications Index will be available starting at 07:00 ET. The previous reading showed a decline of 5.1%, so market participants will be keen to see any improvement in mortgage activity.

At 08:30 ET, we'll get a series of essential price data:

September Import Prices will be released, with the previous month showing a 0.8% increase. We'll also see Import Prices excluding oil, which previously declined by 0.1%.

On the export side, we'll have September Export Prices, which previously fell by 0.7%, and Export Prices excluding agricultural products, which saw a 0.6% decrease last time.

Finally, the EIA Crude Oil Inventories report will be released at 10:30 ET. The prior reading showed a substantial buildup of 5.81 million barrels.

WaveTech Database

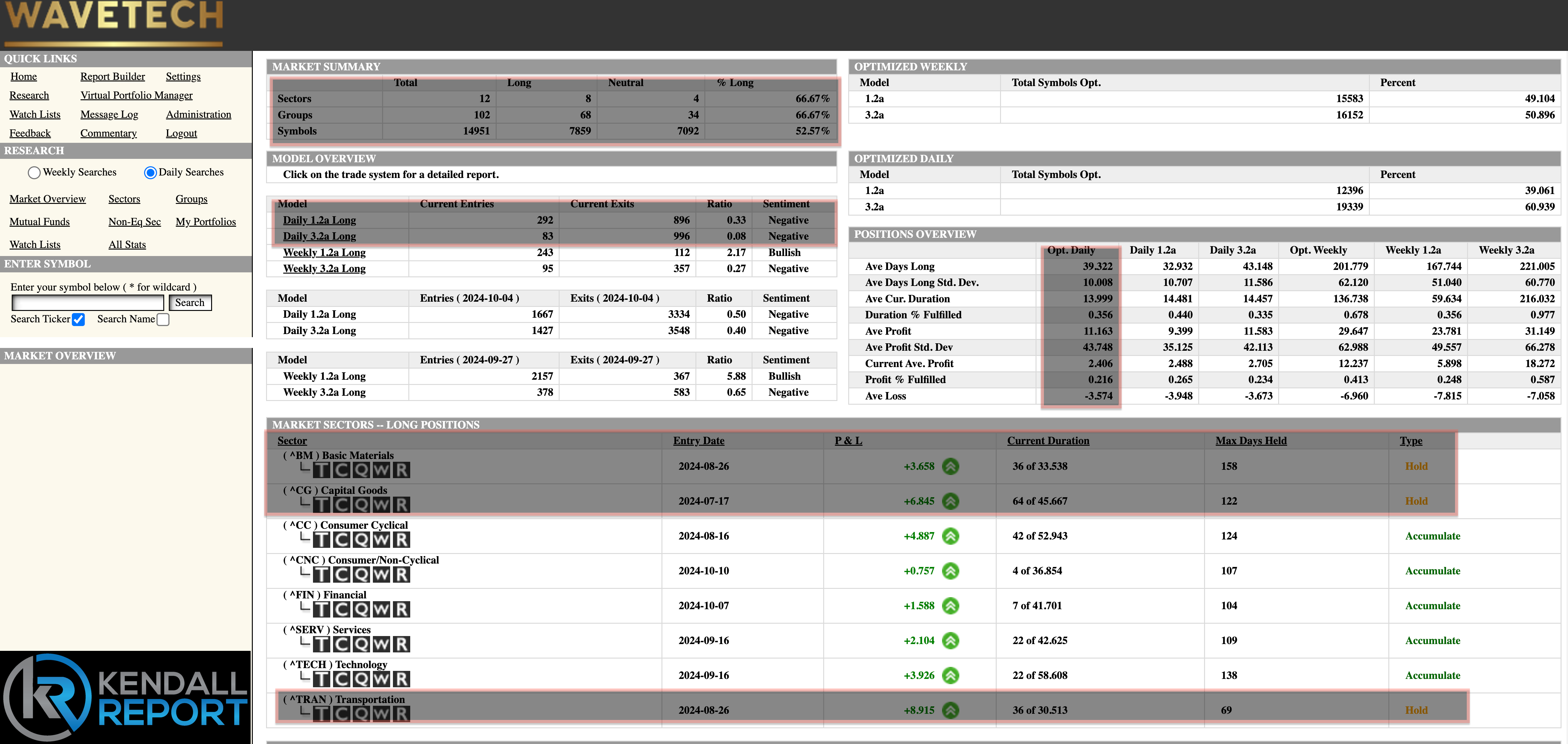

As I analyze yesterday's market action, I'm struck by the depth of the selling pressure we witnessed. Despite the major market indices being down around 1% - a significant but not unusual daily move - the activity beneath the surface was far more dramatic. Our database recorded a substantial 1,892 exits compared to only 375 new entries. This imbalance has pulled the overall percent bullish down to 52.57%, a level I've been anticipating for some time.

This shift in the bullish percentage is noteworthy. About a week ago, I mentioned the possibility of seeing this metric drop to the 58-52% range, and we've now reached that target. It indicates that market sentiment is becoming more cautious, and the breadth of the market's advance is narrowing.

Another increasingly apparent development is the state of three key sectors: basic materials, capital goods, and transportation. These sectors have now exceeded their normal holding periods in our models, putting them on a "caution list" for potential liquidation. This overextension suggests a further narrowing of market participation from a sector viewpoint.

Let's delve deeper into what this means. When sectors exceed their typical holding periods, it often indicates that they've captured most of the gains expected in the current market cycle. As a result, they become more vulnerable to profit-taking or a shift in market leadership. The fact that we're seeing this in three critical cyclical sectors is particularly telling - it could be an early warning sign of a broader economic slowdown or at least a reassessment of growth expectations.

I'm closely watching some key levels regarding overall market bullishness. The following significant number to keep an eye on is 48%. If the bullish percentage drops to this level, it would represent a material market breadth and sentiment deterioration.

However, the real line in the sand is at the 42% bullish level, which I consider the "extreme" number. If the market were to drop below this 42% bullish threshold, it would start to set the tone for the possibility of a more extensive corrective phase emerging. Such a move would suggest that bearish sentiment is becoming dominant, potentially leading to more sustained selling pressure.

It's important to note that we're still at that point. At the moment, the market still appears to be locked into a choppy, range-bound pattern. This type of market action is often seen during periods of uncertainty, where bullish and bearish forces are relatively balanced.

To put this in context, the current market environment is characterized by several competing factors. On the one hand, we generally have strong corporate earnings and signs of resilience in the U.S. economy. On the other, we're grappling with concerns about inflation, potential changes in monetary policy, and geopolitical uncertainties.

The behavior of the three sectors I mentioned earlier—basic materials, capital goods, and transportation—will be crucial to watch in the coming days and weeks. These sectors are often considered bellwethers for the broader economy. If we start to see significant weakness or liquidation in these areas, it could presage a more substantial shift in market dynamics.

Additionally, I'll be paying close attention to sector rotation. As these overextended sectors potentially pull back, will we see money rotating into defensive sectors like utilities and consumer staples? Or will we see a resurgence in technology and growth stocks? If it occurs, the nature of this rotation could tell us a lot about market participants' expectations for the economy and corporate earnings going forward.

In conclusion, while we've seen notable market breadth and sentiment deterioration, we're not yet at levels that would signal an imminent major correction. However, the market is clearly at a crucial juncture. The coming weeks will be critical in determining whether this is a healthy consolidation within an ongoing bull market or the early stages of a more significant downturn. As always, I'll closely monitor these trends and adjust my analysis as new data comes in.

S&P 500 Futures