Markets Remain Cautious

KR Opinion

In yesterday's report, I mentioned that NVDA's action is changing market sentiment. Indeed, it has, but this sentiment fluctuates daily. We saw an NVDA rally of over 6%, which pulled all indices up, with NASDAQ gaining over 1% and S&P 500 up by 4%.

However, this volatility is expected. Despite the price rebound, I still observe some rotation, suggesting the market is at support levels on both the S&P and the NASDAQ. Momentum seems to be dissipating despite yesterday's price rebound.

We also observed some interesting economic events, particularly in the real estate sector, where prices remain elevated due to inventory shortages. As we move into the middle of the week, we might see a potential reduction in real estate sales.

Sales volumes are down, but prices remain high, indicating that inventory shortages control the market. While some areas of the country are softer than others, these inventory issues remain the primary drivers.

No significant changes in the database indicate major shifts, but we see essential momentum starting to dissipate, which typically suggests lower prices ahead. Currently, the semiconductor sector's activity is the market's primary emotional driver.

Looking back on Tuesday’s Action

The S&P 500 (+0.4%) and Nasdaq Composite (+1.3%) closed near their daily highs, driven by gains in mega-cap and semiconductor-related stocks. Despite these gains, the overall market sentiment was negative, with declining issues outnumbering advancing ones by about 3-to-2 at the NYSE and the Nasdaq.

The equal-weighted S&P 500 fell by 0.7%, the Dow Jones Industrial Average dropped 0.8%, and the Russell 2000 declined by 0.4%. However, these losses were mitigated by solid performances from NVIDIA (NVDA 126.09, +7.98, +6.8%), which rebounded after recent losses and other mega-cap stocks.

Carnival (CCL 17.82, +1.43, +8.7%) was the top performer in the S&P 500 thanks to better-than-expected earnings, revenue, and strong guidance. Other cruise line stocks rose in sympathy, with Norwegian Cruise Line (NCLH 18.29, +0.89, +5.1%) and Royal Caribbean (RCL 160.73, +6.21, +4.0%) also among the top performers.

On the downside, Pool (POOL 310.74, -27.17, -8.0%) was the biggest decliner in the S&P 500 after cutting its FY24 guidance.

Eight S&P 500 sectors recorded declines, while the heavily weighted information technology (+1.8%) and communication services (+1.9%) sectors outperformed, supported by gains in their mega-cap components.

The market also reacted to the Conference Board's Consumer Confidence Index for June, which dropped to 100.4 from 101.3 in May due to weakened expectations for future income. Treasuries remained relatively stable in response to the data, with the 2-year note yield unchanged at 4.73% and the 10-year note yield falling one basis point to 4.24%.

Additionally, the Treasury market was absorbing the day's $69 billion 2-year note sale, which saw solid demand.

·Nasdaq Composite: +18.0% YTD

·S&P 500:+14.7% YTD

·S&P Midcap 400: +5.0% YTD

·Dow Jones Industrial Average: +3.8% YTD

·Russell 2000: -0.2% YTD

Reviewing today's economic data:

- April FHFA Housing Price Index: 0.2% (previous: 0.1%)

- April S&P Case-Shiller Home Price Index: 7.2% (KR Forecast: 6.9%, previous revised to 7.5% from 7.4%)

- June Consumer Confidence: 100.4 (KR Forecast: 100.0, previous revised to 101.3 from 102.0)

The key takeaway from the Consumer Confidence report is the weakening expectations for future income. If this perception continues or becomes a reality, it could negatively impact discretionary spending.

Economic Releases for Wednesday:

- 7:00 ET: Weekly MBA Mortgage Index (previous: 0.9%)

- 10:00 ET: May New Home Sales (KR Forecast: 650,000, previous: 634,000)

- 10:30 ET: Weekly crude oil inventories (previous: -2.55 million)

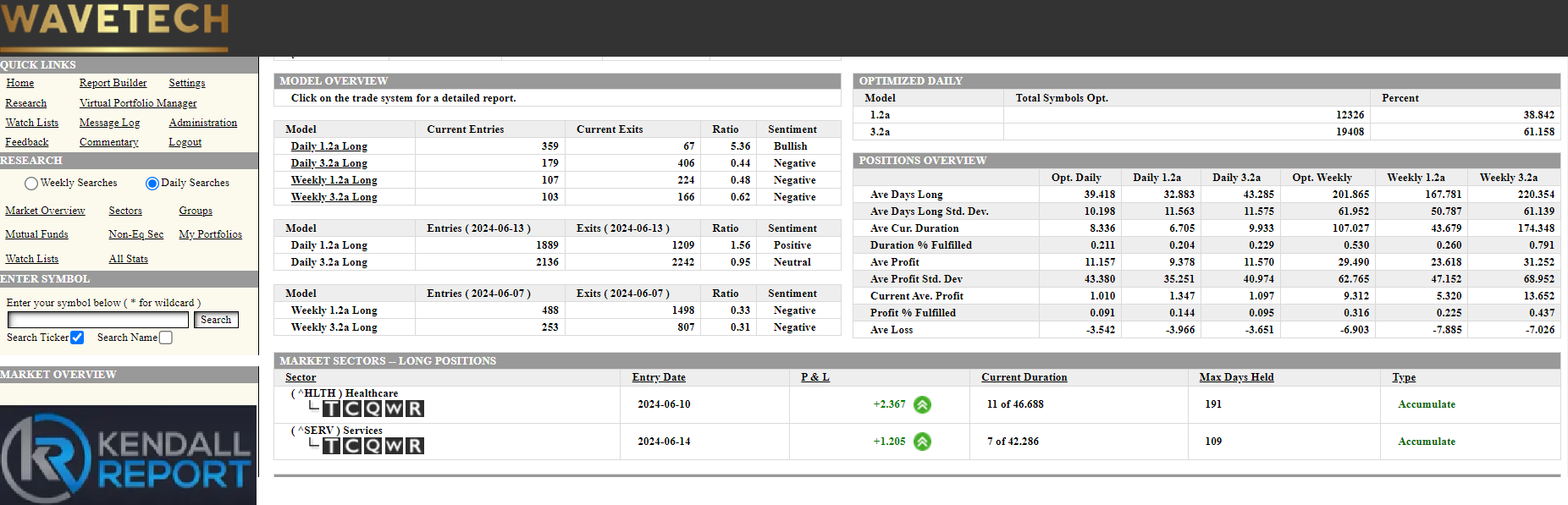

WaveTech Database

The database continues to experience significant rotation, evidenced by 478 new entries and 473 exits, maintaining the bullish percentage at 51.77%. This close balance between new entries and exits indicates a lack of clear directional momentum in the market.

A notable development is the exit signal from the technology sector, which now leaves only two sectors with long positions. This reduction in sector participation highlights the market’s challenges in achieving broader-based support.

The technology sector, often a market leader, moving to a sell signal, underscores the current instability and lack of confidence among investors.

This situation suggests that the market is struggling to gain traction. Without broader sector participation, sustaining upward momentum becomes difficult. The remaining sectors with long positions are not enough to drive a significant rally, and this limited participation hints at underlying market weakness.

As a result, I anticipate continued choppiness in the market over the coming weeks. The lack of widespread sector support and the rotation within the database point to a market that is likely to experience volatility and uncertainty. Investors should be prepared for potential fluctuations and remain cautious, as the current market dynamics suggest a period of instability ahead.

S&P 500 Futures