Markets Signal Caution Before the Election

Bitcoin Stalls!

KR Opinion

The market landscape intensifies as we enter Thursday, with a convergence of major earnings reports and crucial economic data. The performance of the "Magnificent 7" stocks has been mixed. Meta experienced significant pressure, while Microsoft and Alphabet managed to maintain slight positive biases, though without providing substantial market leadership.

Overnight trading has already pushed markets to technical extremes at STX levels, suggesting considerable early strain. This aligns with the previously discussed projection of a potential decline into next Tuesday, though the current price action suggests the downward momentum might accelerate beyond initial expectations. The London open brought notable selling pressure, though the extreme nature of early moves might set up for a technical bounce.

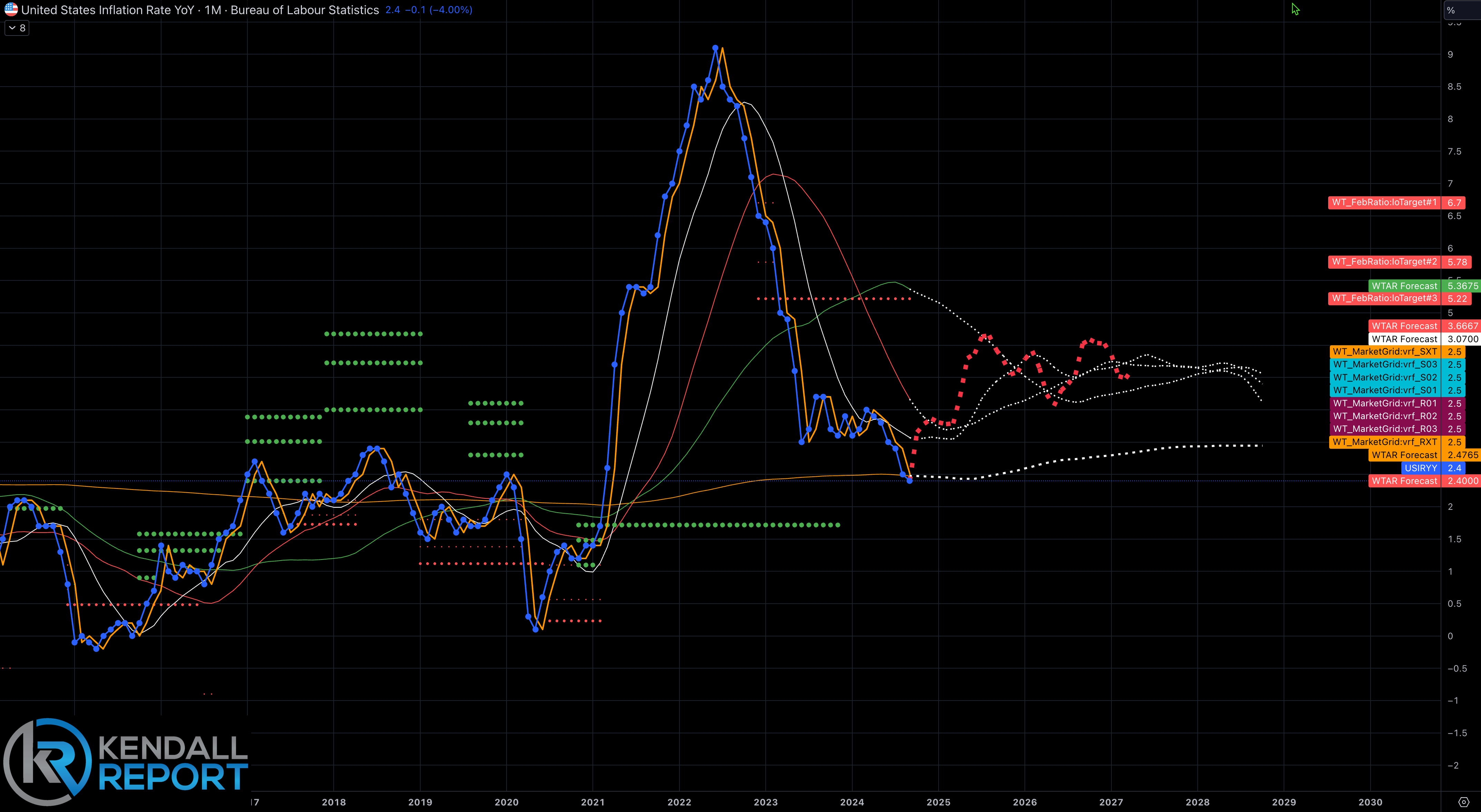

The morning's PCE numbers will be crucial, with expectations for continued moderation. However, looking further ahead, there's an increasing probability of inflationary pressures rebuilding as we move into 2025. This outlook is particularly relevant given political considerations, with discussions around potential tariff policies under a possible Trump administration potentially adding inflationary pressures across various metrics, including CPI and PCE measurements.

Next week's Federal Reserve meeting, scheduled for November 6th and 7th (adjusted for the election), adds another layer of complexity to the market environment. Current economic data, particularly labor market strength, suggests the Fed will likely skip this meeting rather than initiate rate reductions. Friday's employment numbers will provide crucial data points before the Fed gathering.

The impact of the Fed's previous 50 basis point adjustment remains a topic of discussion. It could potentially influence recent economic data, including the slightly weaker GDP reading.

However, multiple forces affecting macro indicators are shaping the broader economic picture. The apparent boost to economic metrics from the rate adjustment raises questions about the underlying strength of various economic measures.

Technical analysis suggests both the S&P 500 and NASDAQ are positioned for potential moves toward their respective 40-day moving averages, a projection that's been in place for several days. However, despite these technical indications, the markets have maintained a sideways trading range.

Market focus will increasingly shift between employment data, election implications, and Fed policy expectations. The technical setup and the concentration of significant events suggest increased market volatility. The convergence of these factors - monetary policy, political developments, and economic data - creates a complex trading environment requiring careful navigation through what appears to be an approaching period of heightened market movement.

Looking back on Wednesday’s Action

The financial markets delivered mixed performance today, with early gains giving way to afternoon weakness. Initial market optimism was fueled by Alphabet's strong quarterly results, which saw the stock advance 2.9% to 176.14, helping push the S&P 500 up 0.3% and the Nasdaq Composite higher by 0.4% at their respective session peaks.

Economic data played a significant role in the morning's upbeat tone. The ADP private-sector employment report exceeded expectations, showing 233,000 new jobs in October and upward revisions to September's figures. The preliminary third-quarter GDP report also demonstrated robust economic growth, particularly in consumer spending.

However, the market's early momentum gradually dissipated without any clear catalyst triggering the reversal. By the session's end, the S&P 500 had declined 0.3%, while the Nasdaq Composite retreated 0.6%. The equal-weighted S&P 500's modest 0.2% decline suggested the sell-off was relatively broad-based but not severe in magnitude.

The semiconductor sector emerged as a notable source of market pressure, with weakness persisting throughout the session. Advanced Micro Devices set a negative tone for chip stocks, tumbling 10.6% to 148.60 after reporting earnings and providing softer-than-expected fourth-quarter revenue guidance.

Treasury market activity added another layer of complexity to the trading day. The 10-year yield demonstrated significant volatility, touching a low of 4.20% before settling at 4.27%. Despite these bond market fluctuations, their impact on equity price action appeared somewhat muted.

The day's trading pattern reflects a market processing multiple inputs—strong earnings from some technology leaders, mixed signals from others, better-than-expected economic data, and ongoing interest rate volatility. This complex backdrop has created an environment where initial optimism can quickly fade as investors reassess positions and react to evolving market conditions.

The relatively contained nature of the declines, particularly in the equal-weighted index, suggests this represents more of a pause in the recent upward trend rather than the start of a more significant correction. However, the market's inability to hold early gains despite positive catalysts warrants attention as we progress through earnings season.

Nasdaq Composite: +24.0% YTD

S&P 500: +21.9% YTD

Dow Jones Industrial Average: +11.8% YTD

S&P Midcap 400: +12.8% YTD

Russell 2000: +10.2% YTD

Wednesday's Key Economic Releases

The mortgage market showed signs of stabilization, with the Weekly MBA Mortgage Applications Index declining marginally by 0.1%, a significant improvement from the previous week's 6.7% drop.

Labor market strength exceeded expectations as ADP Employment Change reported 233,000 new jobs in October, substantially above the KR Forecast consensus of 105,000. September's figures were revised upward to 159,000. The robust job gains spanned sectors, regions, and business sizes, indicating broad-based economic vitality inconsistent with recessionary conditions.

The third-quarter GDP advance reading was 2.8%, slightly below the KR Forecast consensus of 3.0%. The GDP Chain Deflator registered 1.8%, falling short of the expected 2.3%. Consumer spending emerged as the primary growth driver, with Personal Consumption Expenditures surging 3.7%—the strongest showing since Q1 2023 and well above the previous ten-quarter average of 2.3%. This robust consumption contributed 2.46 percentage points to the quarter's real GDP growth.

The housing sector delivered a surprise as Pending Home Sales jumped 7.4%, significantly exceeding the KR Forecast consensus of 2.5% and the previous month's 0.6% increase.

Thursday's Economic Releases

Personal Income and Spending data (8:30 ET) are expected to show 0.4% increases, up from 0.2% prior readings. PCE Prices and Core PCE Prices are each projected to rise 0.2%, slightly above their previous 0.1% gains.

The Employment Cost Index for Q3 is anticipated to rise 1.0%, marginally above last quarter's 0.9%. Weekly jobless claims are expected to tick slightly to 229,000 from 227,000, while continuing claims data will update from the previous 1.897 million.

The Chicago PMI release at 9:45 ET is forecast to improve slightly to 47.5 from 46.6, though remaining in contractionary territory. The day's data releases conclude with the weekly natural gas inventory report, following last week's 80 bcf build.

WaveTech Database