Markets to Hesitate...

Everyone Waiting on Tesla Earnings

KR Opinion

In yesterday's commentary, I discussed the potential for a two-day rally, and it appears we experienced nearly all of it in one day, with the market gaining 1%. This gain reflects most of my expectations for the two-day market rally. However, overnight, we are seeing some weakness.

This week, there isn't much significant news other than the PCE numbers on Friday. We also have Tesla's earnings report after the market closes on Tuesday. I expect a lot of enthusiasm was already pumped into Tesla today, which could lead to disappointment as we approach Wednesday's opening. Given Tesla's high volatility and status as a meme stock, anything is possible.

I anticipate choppy markets ahead as we progress through the week. I do not expect a complete reversal or a rally toward new highs. Instead, I foresee some backfilling over the next couple of days. As we approach the month's final week, the forecast suggests a potential decline into some key support levels, which I will discuss later.

While the equity markets managed to rally, we essentially saw stabilization across most other markets. Expect a reasonably stable day ahead, with the possibility of some downside action, likely staying within the support levels that I will cover in the technical section.

Looking Back on Monday

The stock market rebounded today after last week's declines, with mega-cap stocks and semiconductor shares leading the upside action after underperforming last week. Many other stocks joined the rally as well. The S&P 500 closed 1.1% higher, while the Invesco S&P 500 Equal Weight ETF (RSP) closed 0.8% higher.

Notable winners included NVIDIA (NVDA) which rose 4.7% to $123.54, Meta Platforms (META) which increased by 2.2% to $487.40, and Microsoft (MSFT) which gained 1.3% to $442.94. Despite today's gains, NVDA shares are flat for July, META shares are down 3.3%, and MSFT is down 0.9%.

Overall, nine of the eleven S&P 500 sectors posted gains. The information technology sector (+2.0%) and the communication services sector (+1.2%) led the way, boosted by the stocks as mentioned above. The industrial sector (+1.1%) and the real estate sector (+1.0%) also rose by at least 1.0%. However, the energy sector logged the most significant decline, falling 0.3% amid declining oil prices ($78.43/bbl, down $0.26).

In other news, market participants are digesting the announcement that President Biden has exited the 2024 presidential race and endorsed Kamala Harris for candidacy. This news had muted responses in the equity and bond markets. The 10-year note yield increased by two basis points to 4.26%, and the 2-year note yield increased by one basis point to 4.52%.

There were no significant US economic data releases on Monday.

Tuesday's economic data will include the June Existing Home Sales report at 10:00 ET. Additionally, several companies including General Motors (GM), UPS (UPS), Albertsons (ACI), Lockheed Martin (LMT), Coca-Cola (KO), and Philip Morris International (PM) are set to report earnings before the market opens on Tuesday.

Nasdaq Composite:+20.0% YTD

S&P 500: +16.7% YTD

S&P Midcap 400: +9.7% YTD

Russell 2000: +9.6% YTD

Dow Jones Industrial Average: +7.2% YTD

Announcement: Subscription Price Increase Starting August 1st

I have an important update regarding our subscription fees. Starting August 1st, the monthly subscription fee will increase to $19.97. However, there's still a fantastic opportunity to lock in significant savings by opting for an annual subscription. If you pay for a full year, the cost is only $80.00, which breaks down to just $6.67 per month.

Why the Increase?

After nearly six months of delivering high-quality content and evaluating the time and effort required, it’s clear that an adjustment is necessary. Additionally, compared to other services in this space, our new rate is still highly competitive—many charge double my monthly rate. This increase will allow us to continue providing exceptional value and ensure the sustainability of our work.

Act Now and Save!

By opting for the annual subscription annual subscription before the end of this month, you can avoid the price increase and enjoy the same great content at a significantly reduced rate of $6.67 per month. After July, the annual subscription will still offer a discount, but the price will reflect the new monthly rate before the end of this month; you can avoid the price increase and enjoy the same great content at a significantly reduced rate of $6.67 per month. After July, the annual subscription will still offer a discount, but the price will reflect the new monthly rate.

Thank you for your understanding and continued support. The initial $8 monthly fee was always intended as an introductory rate, and we’re thrilled to have so many of you on board. Maintaining this environment requires substantial effort; we believe this adjustment is fair and necessary.

I've mentioned in my newsletter over the past 10 days that we will expand some of the content. One of the things I plan to do is focus on individual stocks. I'll update a selective group of stocks regularly, using WaveTech to stay current on trades and their cycles.

As we progress, we'll start providing more specific buy and sell indications on a selected set of stocks, initially focusing on intermediate trades updated weekly. I will also review the portfolio environment and provide comments on selected stocks.

The goal is to understand individual stocks, asset classes, and other crucial aspects needed to navigate the markets better. We are entering a more dynamic environment in the coming months, which will require strong sell discipline.

WaveTech Database

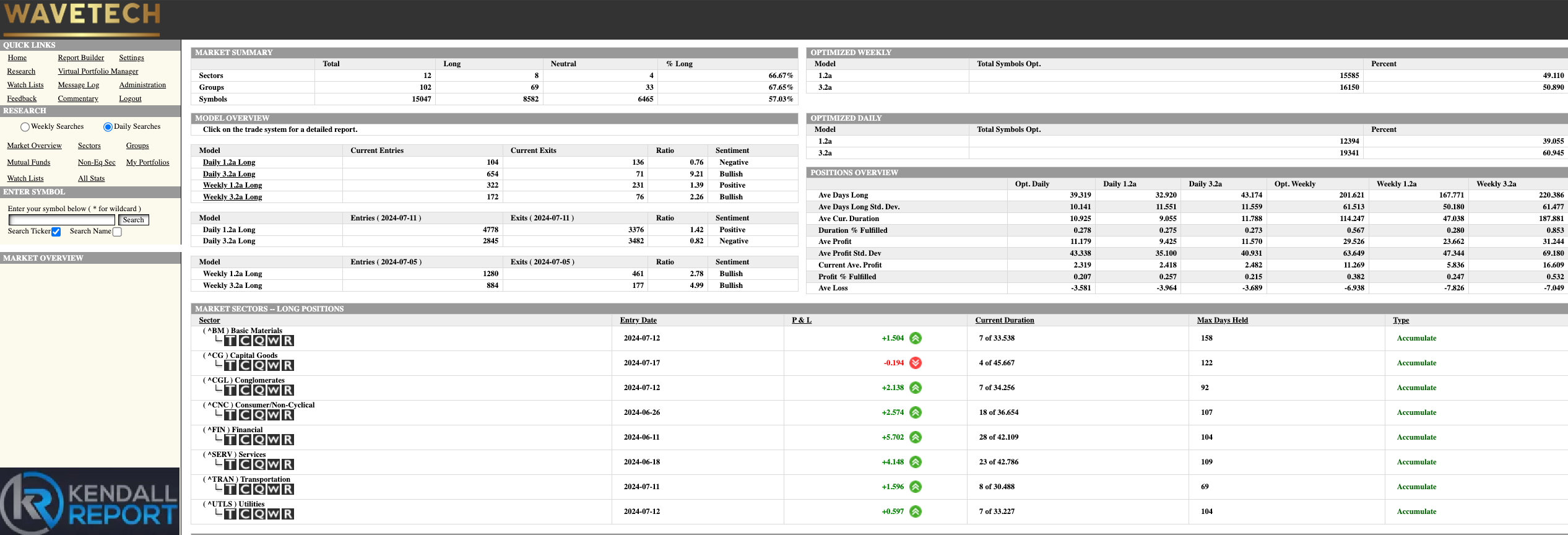

With yesterday's market rally, we observed stabilization in the database, with 758 new entries and 207 exits. The percentage of bullish entries is now at 57.03%. Typically, within a cycle like this, the database randomly fluctuates between 52% to 62% as trends unfold.

We currently have eight sectors in the long position, indicating positive rotation at the sector level. Additionally, the industry groups are also showing strength, with 67.65% bullish entries across 69 industry groups. This overall profile suggests a continuation of the uptrend.

However, at this phase, it appears we might see more consolidation before any significant resumption of the uptrend. Despite this, the intermediate and short-term databases remain very robust, so we are not anticipating any major declines. The market will likely remain choppy for a couple of days until it establishes a pattern indicating a recovery and potential rally.

I previously mentioned the 323 patterns, and today marks the second day of these two patterns. We might see up to three days of potential declines, but this does not necessarily mean a substantial drop. For more details, please refer to the S&P technical section.

S&P 500 Futures

The S&P 500 rallied sharply yesterday, pushing up over 1% as the market returned to the 5616 level, which was S3 on the market grid. Overnight action is slightly weaker, suggesting we might have climaxed with a one-day rally rather than extending it to two days.

- Resistance Levels: