Markets to Move lower...

Will bitcoin hold support.

KR Opinion

Market conditions show significant volatility, with important technical developments occurring. Yesterday's session reached a critical technical level at 5801, followed by an impressive overnight recovery of 55 points. This bounce, while substantial, fits into a larger pattern, suggesting we may see continued market weakness leading up to the U.S. presidential election.

Tesla's performance deserves particular attention. Despite closing down 2% in Wednesday's regular session, the company's shares surged approximately 10% in after-hours trading following its earnings release. The company's report indicated improved stability in its business operations and successful achievement of key performance metrics.

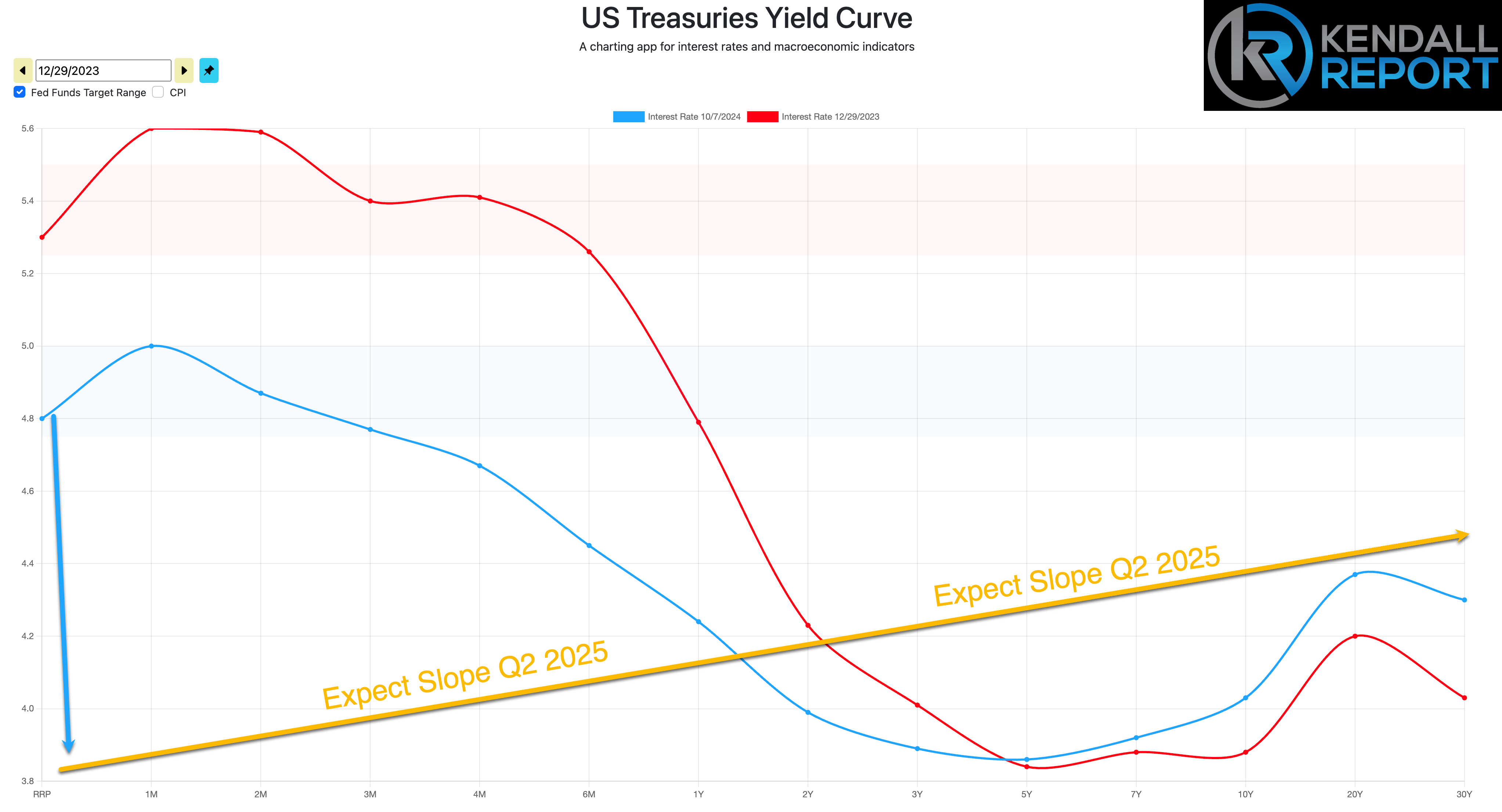

A concerning trend is emerging regarding central bank messaging. There appears to be a growing disconnect between their confident stance on inflation control and market realities, as evidenced by the 10-year Treasury yield reaching 4.25%. The database is showing nearly 4,000 sell signals, indicating significant market deterioration. This raises questions about whether the Federal Reserve's recent 50 basis point move was premature despite its initial positive reception.

As we look ahead to 2025, the yield curve continues to show a move toward normalization, with current rates for the 2-year at 4.07%, the 10-year at 4.24%, and the 30-year at 4.50%. With two more Federal Reserve meetings remaining this year, market participants closely watch for policy signals. Adding to the complexity, the upcoming election results may face delays, with three states indicating they might need up to 10 days to finalize vote counts, potentially creating additional market uncertainty.

China's economic situation adds another layer of complexity, as its accommodative monetary policy contrasts with that of other global central banks. This divergence in policy approaches could significantly impact global markets.

The combination of potential election uncertainty, yield curve dynamics, and divergent central bank policies suggests we may be entering a period of increased market volatility.

The previous confidence in inflation control may need to be reassessed as we approach Q1 2025, mainly if inflation metrics show signs of acceleration. While encouraging short-term stability, the aggressive nature of dip-buying at technical support levels doesn't necessarily end the broader market concerns emerging from the technical indicators and institutional selling patterns.

Looking Back on Wednesday’s

Wall Street faced significant headwinds as major stocks retreated and Treasury yields continued their upward climb. The day saw the 2-year Treasury yield touch 4.09% while the 10-year reached 4.255%, with a disappointing 20-year bond reopening adding to the week's downward pressure.

Despite recovering somewhat from earlier lows that saw the Dow Jones Industrial Average drop more than 500 points, markets struggled to find positive momentum. The lack of buying interest extended beyond stocks into commodities, particularly affecting oil and precious metals markets.

Technology and consumer-focused companies bore the brunt of today's selling pressure. Tesla fell 2.0% ahead of its earnings report, while Amazon dropped 2.6%. McDonald's shares declined 5.2% amid reports of an E. coli outbreak. Apple shares weakened by 2.2% on iPhone 16 demand concerns, and NVIDIA fell by 2.8%.

Some bright spots emerged in defensive sectors, with real estate and utilities gaining 1.0%. AT&T provided a rare positive note, climbing 4.6% following its earnings announcement. However, these gains were overshadowed by broader market weakness.

Boeing added to the market's woes, falling 1.8% after its new CEO indicated a lengthy path to recovery for the aerospace giant. The day's negative sentiment was reflected in the CBOE Volatility Index, which jumped 6.7% to 19.41.

Market breadth confirmed the day's pessimistic tone, with declining stocks outnumbering advancing ones by roughly three to one on the NYSE and Nasdaq exchanges. The day's trading pattern suggests investors remain cautious amid ongoing concerns about interest rates and corporate earnings.

Nasdaq Composite: +21.8% YTD

S&P 500: +21.5% YTD

Dow Jones Industrial Average: +12.9% YTD

S&P Midcap 400: +12.3% YTD

Russell 2000: +9.2% YTD

Reviewing Wednesday’s economic Releases:

According to the KR Forecast, September existing home sales declined 1.0% from August to a seasonally adjusted annual rate of 3.84 million units. This fell short of the expected 3.90 million units and represents a 3.5% decrease compared to September last year. August's figures were revised slightly upward to 3.88 million from the initially reported 3.86 million.

The housing market continues to show interesting dynamics. While more inventory becomes available to buyers, the market remains tight overall. This is evidenced by continued increases in median home prices and notably low mortgage delinquency rates.

Adding to the housing market picture, mortgage application activity showed weakness across the board. The overall index dropped 6.7% for the week, with refinancing applications down 8% and purchase applications declining 5%.

Market watchers should note several key reports before tomorrow's economic releases. The day begins with the weekly jobless claims data at 8:30 AM Eastern. This will follow the preliminary October readings for U.S. Manufacturing and Services PMIs at 9:45 AM. The morning's economic releases conclude with September's new home sales report at 10:00 AM.

WaveTech Database

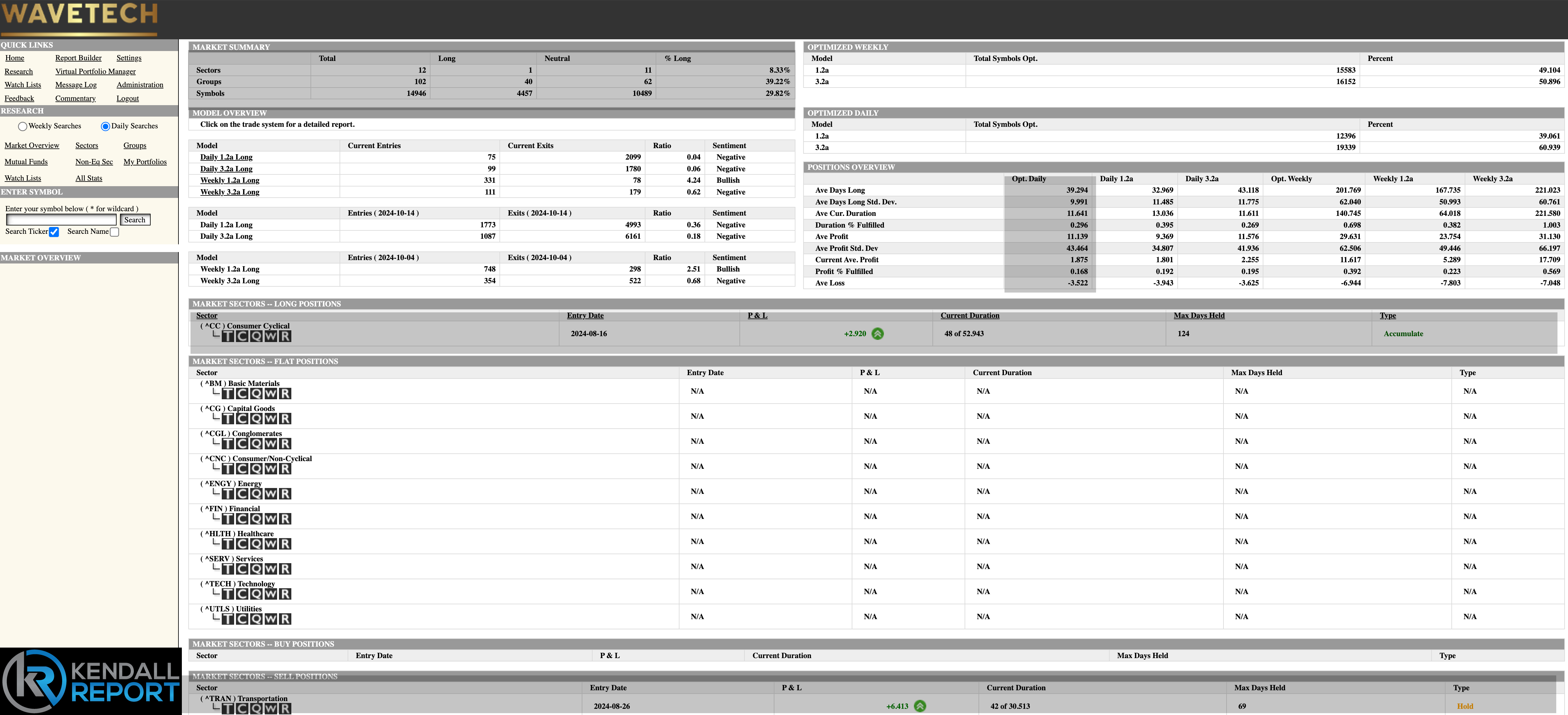

The market's technical indicators reveal extensive deterioration across multiple sectors and individual securities. The transportation sector's shift to negative territory is of particular significance despite its previous position of strength. This leaves the consumer cyclical sector as the sole positive performer, maintaining its upward trend for 48 days against a typical holding period of 53 days, suggesting potential vulnerability.

The database analysis showed a dramatic sentiment reversal, with 3,879 securities generating exit signals compared to 179 new entries. This substantial imbalance has driven the short-term database reading down to 29.82%, indicating a severe weakening in market breadth.

The intermediate-term model updates scheduled for Friday may see the current % bullish reading of 82% face downward pressure. While 42% represents a key threshold, reaching this level typically requires an extended period - potentially several weeks to two months - barring a sharp market decline.

The S&P 500's recent touch of a critical weekly technical extreme level catalyzed an impressive overnight bounce that extended into regular trading. However, short-term database signals suggest this recovery might be temporary. The emerging pattern points toward a consolidation phase with an expected downward bias over the next several trading sessions.

This divergence between immediate market resilience and underlying technical deterioration creates a complex dynamic. While buying interest persists at technical support levels, the broader market structure shows weakness. The substantial number of exit signals and minimal new entries indicate institutional investors may reduce their market exposure across a wide spectrum of securities.

This pattern of technical deterioration typically unfolds gradually, beginning with short-term indicators before potentially impacting intermediate-term trends. The current environment, characterized by widespread technical exits and limited sector strength, suggests the early stages of a more significant market adjustment period. The focus now shifts to whether this short-term weakness will influence longer-term market dynamics, particularly as we approach Friday's intermediate model updates.

S&P 500 Futures