Markets to Stall?

Markets to Stall?

Bitcoin Hits 64k! Can it Continue?

KR Opinion

As I reflect on yesterday's market action, I'm struck by the sheer robustness of the rally. At one point, the S&P 500 was up nearly 2%, which is a significant move by any measure. While we did see some retreat from these lofty levels by the close, the overall sentiment was unmistakably bullish.

What particularly caught my attention was the sense of panic in the air. Many market participants had been caught on the wrong side of this move, leading to liquidity in the order book drying up rapidly. The result was a massive bidding frenzy, with buyers seemingly indifferent to price. This buying pressure started building in London overnight and accelerated dramatically as we entered the U.S. trading session.

I've been pondering whether rate cuts would be bullish for the market, and the Federal Reserve's decision to implement a 0.5% rate cut on Wednesday has me more concerned than anything else. This ties into a narrative I've been discussing regarding the accuracy of economic data over the past year.

I am concerned that unemployment figures, GDP, and other metrics must be corrected and substantially revised. What troubles me most is that based on Powell's comments during Wednesday's conference call, there seems to be little interest in transparency or taking responsibility for these potential inaccuracies. This lack of clarity continues to be a critical factor we must closely monitor.

Turning to yesterday's economic releases, we saw several surprises. Initial and continuing claims came in better than expected, and the Philadelphia Fed index significantly outperformed expectations. On the surface, these numbers paint a picture of a robust economy. However, given my concerns about data accuracy, the real question we must grapple with is how we should interpret and react to these figures.

In my recent YouTube video, I delved into this topic in detail, which I encourage you to watch for a more comprehensive discussion. But in essence, I'm finding it challenging to fully embrace these numbers at face value, especially in light of the market's exuberant reaction yesterday.

There's a possibility that yesterday's rally pushed things too far, too fast. As a result, I wouldn't be surprised to see some sideways consolidation in the near term as the market digests these moves and we get a clearer picture of whether higher prices are sustainable in this pattern.

That said, our algorithmic indicators are still suggesting the potential for higher prices, particularly as we move into the first week of October. The intermediate-term charts point to at least two or three more weeks of potential upside. However, we must balance this technical outlook with the broader contextual factors.

One such factor is the approaching election. As we approach this event, the markets will likely experience increased volatility, if not outright caution. Observing how market sentiment evolves as we approach this critical juncture will be fascinating.

As we head into Friday, it's worth noting that there are no scheduled economic releases. This means we won't have any fresh data to drive sentiment. Instead, I expect the market narrative to continue focusing on the implications of the recent interest rate cut.

The prevailing view is that this rate reduction will help maintain positive economic momentum. While I agree that a recession doesn't appear to be on the immediate horizon, I view this rate cut more as a "window dressing" move than a necessary economic stimulus. Looking ahead, there's a possibility of a pause in rate cuts in November, depending on the data we see in the next two employment reports and upcoming CPI, PPI, and PCE numbers.

In conclusion, while the market's reaction has been undeniably positive, we're entering a period that calls for careful analysis and perhaps some hesitation. The disconnect between market exuberance and underlying economic realities continues to be a source of concern for me.

Looking back on Thursday’s action

As I analyze today's market action, I'm struck by the robust performance across major indices. The S&P 500 and Dow Jones Industrial Average reached new all-time highs, surging 1.7% and 1.3%, respectively, while the Nasdaq Composite posted an impressive 2.5% gain.

This rally directly responded to yesterday's Federal Open Market Committee (FOMC) decision to cut the target rate for federal funds by 50 basis points, bringing it to the 4.75-5.00% range. The market's enthusiastic reaction reflects a growing belief that the economy is on solid footing and that the Fed will continue to adjust rates as needed to maintain this positive economic backdrop.

Today's economic data reinforces this optimistic outlook. Weekly jobless claims remained steady below levels typically associated with recessions, the Philadelphia Fed Index returned to expansion territory in September, and while existing home sales for August came in slightly below expectations, they still indicated a tight housing market.

The rally was broad-based, with almost all sectors participating. A palpable 'fear of missing out' sentiment drove buying. Mega-cap stocks and chipmakers were standouts. The Vanguard Mega Cap Growth ETF rose 2.5%, while the PHLX Semiconductor Index jumped 4.3%.

Apple was a notable performer, surging 3.7% after T-Mobile's CEO indicated that iPhone 16 sales in the first week outpaced last year's models. This strength in Apple helped propel the S&P 500 information technology sector to a 3.1% gain. Other top-performing sectors included consumer discretionary (+2.2%), communication services (+1.9%), and industrials (+1.8%).

In contrast, defensive sectors like utilities and consumer staples both declined 0.6%, underscoring the risk-on sentiment pervading the market today.

In the bond market, we saw some divergence, with the 10-year yield settling five basis points higher at 3.73%, while the 2-year yield remained unchanged at 3.60%.

Despite this broad rally, FedEx stood out as a significant underperformer, dropping nearly 10% after missing estimates and delivering downbeat guidance for fiscal year 2025.

This market action suggests renewed optimism about economic growth prospects and the Fed's ability to navigate a 'soft landing'. However, as always, it's crucial to remain vigilant. While the current sentiment is bullish, unexpected economic data or geopolitical events could quickly shift the landscape. I'll closely monitor how these trends develop in the coming days and weeks.

· Nasdaq Composite: +20.0% YTD

· S&P 500: +19.8% YTD

· S&P Midcap 400: +12.3% YTD

· Dow Jones Industrial Average: +11.5% YTD

· Russell 2000: +11.1% YTD

Thursday’s economic releases

The Weekly Initial Claims came in at 219,000, significantly lower than the KR Forecast consensus of 232,000. The prior week's figure was revised slightly upward to 231,000 from 230,000. Weekly Continuing Claims decreased to 1.829 million, down from the revised previous figure of 1.843 million.

What's particularly noteworthy about these claims numbers is their implications for the broader economic picture. The low initial claims reading doesn't suggest an elevated likelihood of recession or economic downturn. This aligns with the sentiment expressed by Fed Chair Powell and supports the narrative of a resilient labor market.

Turning to the Q2 Current Account Balance, we saw a deficit of $266.8 billion, widening from the revised prior figure of $241.0 billion. This increase in the current account deficit could have implications for currency markets and trade dynamics.

The September Philadelphia Fed Index surprised to the upside, coming in at 1.7. While this is below the KR Forecast consensus of 3.0, it marks a significant improvement from the prior reading of -7.0. It indicates a return to expansion territory for manufacturing activity in the region.

In the housing market, August’s existing home sales came in at 3.86 million, slightly below the KR forecast consensus of 3.90 million and down from the revised prior figure of 3.96 million. The key takeaway is that more inventory becomes available as mortgage rates decline. However, the market remains tight, as evidenced by the ongoing increase in median home prices.

The August Leading Indicators showed a decline of 0.2%, slightly better than the KR Forecast consensus of -0.3% and an improvement from the prior month's -0.6%. This suggests a moderating pace of economic deceleration.

As we look ahead, it's worth noting that no significant U.S. economic data is scheduled for release on Friday. This could mean market participants will have time to digest today's releases and the implications of yesterday's Federal Reserve decision.

Today's data paints a picture of an economy that continues to show resilience in key areas, particularly the labor market while exhibiting some signs of moderation in others. The housing market data, in particular, suggests a delicate balance between increased inventory and sustained demand. As always, we'll continue to monitor these trends closely and assess their potential impact on monetary policy and market dynamics.

WaveTech Database

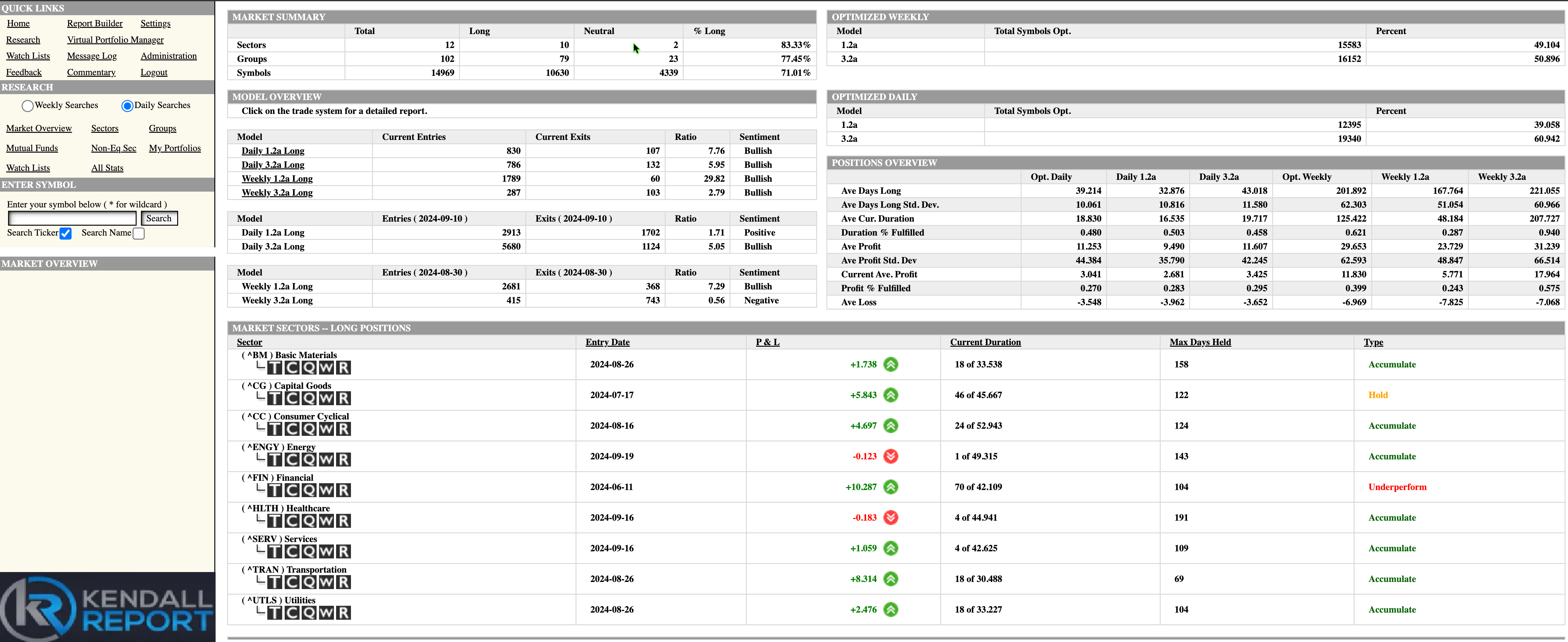

As I delve into the latest WaveTech database results, I'm struck by the continued momentum we're witnessing in the market. Yesterday's robust action has translated into impressive numbers, with 1,616 new entries and only 239 exits. This net positive flow has pushed our percent bullish metric to 71.01%.

This surge in bullish sentiment is exciting when we consider the context. A few days ago, I discussed how we typically see the bullish percent range between 68% and 72% before encountering some resistance. Now that we've reached the upper end of this range, it's worth pondering whether we're approaching a potential inflection point.

What's catching my attention is the status of several sectors we're currently long. Many of these have reached or exceeded their expected holding periods, which could signal impending shifts in market leadership. Let's break this down a bit:

The capital goods sector has entered a "hold" phase, which suggests that the easy money may have already been made while it's still performing well. We'll need to monitor this sector closely for signs of a potential topping or a continuation of its uptrend.

Even more intriguing is the financial sector, which has now moved into an "underperform" status. This doesn't necessarily mean it's time to sell but indicates that the sector has exceeded its average holding period. Typically, we expect financials to be held for about 42 days, but we're now at day 70. This extended duration could indicate that the sector's outperformance may be waning.

These capital goods and financial, combined with the overall database reaching extremely bullish levels, suggest that we're likely on the cusp of seeing some sector rotation. It's a natural part of the market cycle, and I'll be watching closely to see which areas of the market step up to take leadership.

It's worth noting that not all sectors are in the same boat. Some are still in the early or middle stages of their cycles. Energy, for instance, just turned bullish a day ago. This aligns with comments I've made in recent YouTube videos and other analyses, highlighting the potential for energy to show increased strength over the next couple of months.

This divergence in sector performance and cycle positioning creates an interesting dynamic. While some areas of the market may get a bit long in the tooth, others are just starting to hit their stride. This suggests that while we might see some near-term choppiness as leadership shifts, the overall market trend could remain supportive.

However, it's crucial to remain vigilant. When the overall database reaches these extreme bullish levels, it often precedes at least a short-term pause or consolidation in the broader market. The key will be watching how smoothly the baton is passed from current leaders to emerging ones.

In conclusion, while the current bullish sentiment is undoubtedly strong, the market may be undergoing a recalibration phase. The potential sector rotation we're seeing signs of could provide new opportunities for those who are prepared and vigilant.

S&P 500 Futures

Keep reading with a 7-day free trial

Subscribe to The Kendall Report to keep reading this post and get 7 days of free access to the full post archives.