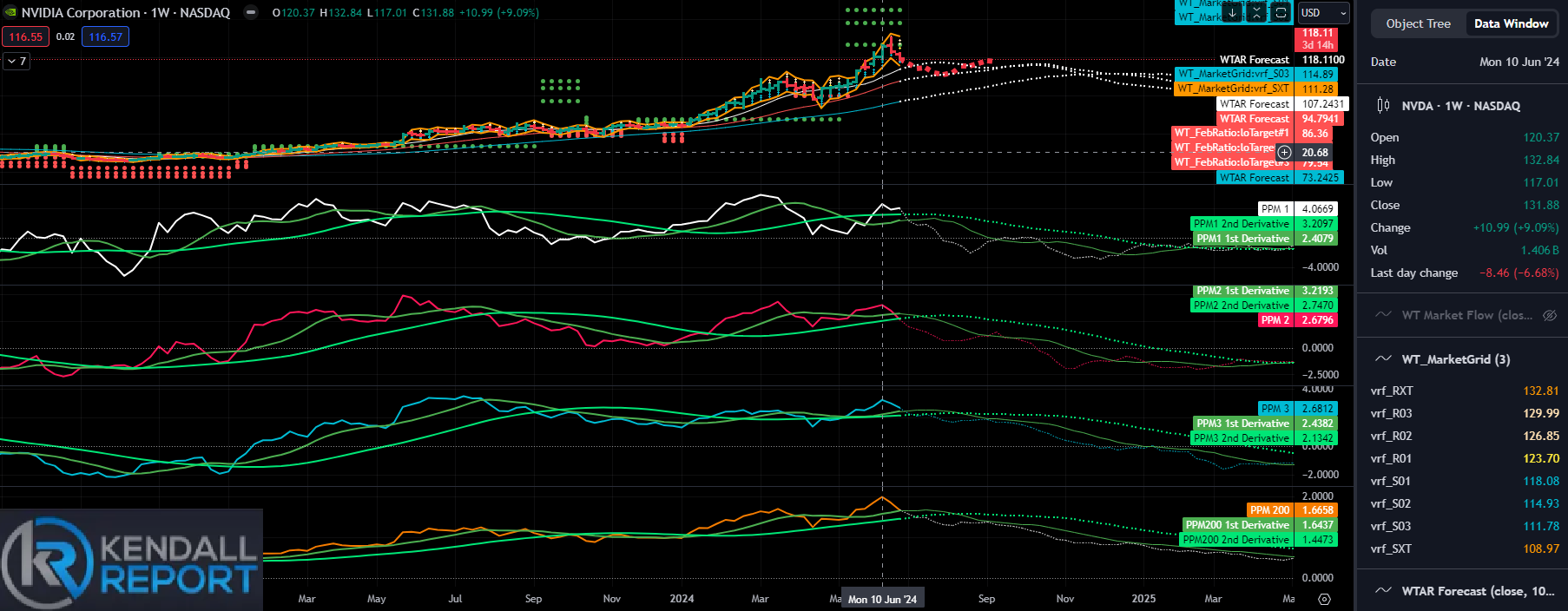

NVDA Triggers Sentiment Change...

Bitcoin bounces off Support...

KR Opinion

Yesterday's decline in NVIDIA (NVDA) and other tech stocks has significantly impacted market sentiment. Despite this, the S&P 500 was down only 0.3%, while the Nasdaq saw a more considerable drop. However, we observed a rotation in the market, with the Dow Jones and the Russell indexes posting gains, mainly driven by a rally in bank stocks.

No significant news is expected today, so we don't anticipate much volatility. However, if the pressure on semiconductor stocks continues, we could see further downside, particularly in the Nasdaq.

The market appears to be entering a correction phase, which may last for the next 5 to 8 sessions. We expect to see a move back toward the 21-day moving average, with momentum likely to decline substantially as we approach the end of June and the beginning of July.

Looking Back on Monday’s Action

Despite a weak performance at the index level, the stock market had a solid showing today. The S&P 500 fell by 0.3%, and the Nasdaq Composite dropped by 1.1%, closing their session lows. This decline was mainly due to profit-taking in mega-cap stocks, including a significant loss in NVIDIA (NVDA 118.11, -8.46, -6.7%).

Other significant stocks also saw declines: Amazon.com (AMZN 185.57, -3.51, -1.9%), Microsoft (MSFT 447.67, -2.11, -0.5%), and Broadcom (AVGO 1592.21, -61.17, -3.7%). Semiconductor stocks like Super Micro Computer (SMCI 826.98, -78.28, -8.7%) and Qualcomm (QCOM 200.84, -11.69, -5.5%) were notable laggards, contributing to the PHLX Semiconductor Index (SOX) dropping 3.0%.

However, buying activity was strong across other market segments. The Dow Jones Industrial Average gained 0.7%, the Russell 2000 rose 0.4%, and the equal-weighted S&P 500 increased by 0.5%.

Energy and bank stocks were among the top performers. The S&P 500 energy sector rose by 2.7%, and the financial industry increased by 1.0%. Energy shares benefited from rising commodity prices, with WTI crude oil futures up 1.2% at $81.63/bbl and natural gas futures up 3.7% at $2.81/mmbtu.

Bank stocks also outperformed ahead of the Fed's stress test results, with the SPDR S&P Bank ETF (KBE) rising 1.9%.

There was no significant economic data today, but Tuesday's calendar includes the June Consumer Confidence report (expected 100.0; prior 102.0) at 10:00 a.m. ET. Additionally, the U.S. Treasury will hold a $69 billion 2-year Treasury note offering tomorrow, with results at 1:00 p.m. ET.

In the bond market, the 10-year note yield fell by one basis point to 4.25%, while the 2-year note yield remained unchanged at 4.73%.

Economic Releases for Tuesday

The FHFA Housing Price Index for April will be released at 9:00 AM ET. There is no consensus estimate, and the previous month's increase was 0.1%.

Also, at 9:00 AM ET, the S&P Case-Shiller Home Price Index for April will be announced. The consensus estimate is 7.0%, up from the previous month's 6.9%.

The June consumer confidence report will be released at 10:00 AM ET. The consensus estimate is 101.5, a slight increase from the previous 100.0.

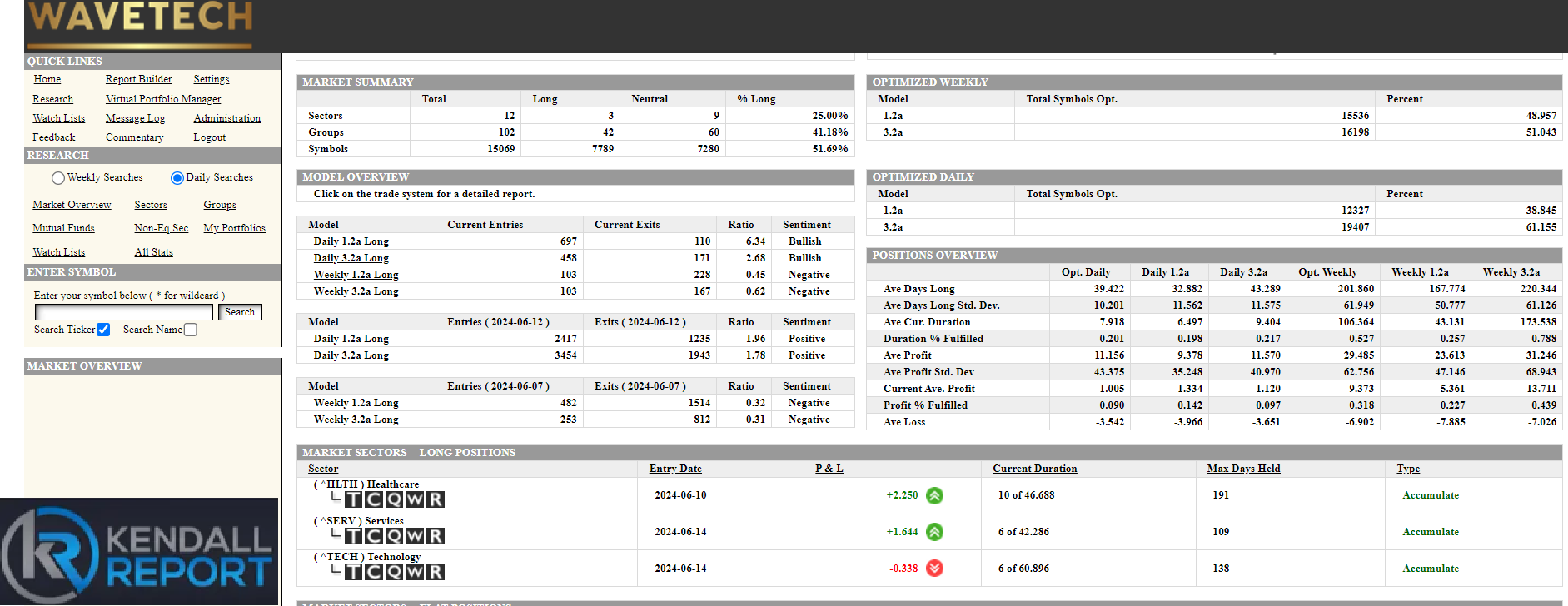

WaveTech Database

Despite mixed index performances yesterday, the short-term models indicated net buying activity with 1,155 new entries and 281 exits. The bullish percentage now stands at 51.69%. The sectors are holding steady, with only three sectors showing long positions, and there hasn't been any significant rotation in the markets.

It will be interesting to observe any potential rotation, especially if the semiconductor sector experiences further volatility, which could affect market dynamics. However, the models appear stable for now. We can maintain a positive, forward-looking expectation if the bullish percentage remains above 42%.

S&P 500 Futures