PPI and CPI to Keep Markets Positive...

PPI and CPI to Keep Markets Positive...

Bitcoin continues to struggle

KR Opinion

Looking back on last week, the S&P 500 and NASDAQ Composite surged, driven significantly by the "Mag 7" stocks, pushing the markets harder than in recent weeks. A robust WaveTech database and vital technical elements support the market's upward movement.

In the YouTube video I'm sharing below, I discuss longer-term trends and expectations in detail. Overall, the outlook suggests that the markets will likely remain robust over the next couple of months, at least through the end of August and possibly into early September, as we approach the end of Q3.

This week, market participants will focus on the Producer Price Index (PPI) and Consumer Price Index (CPI) reports, due Thursday and Friday. These reports will likely keep the markets cautious or consolidating as they await the new data.

I've been discussing an "echo bounce" in inflation over the past few months, which I expect to materialize in August and September. However, we won't see these reports until September and October, as they reflect the previous month's data. I believe these future reports will show an acceleration in inflation.

For the current scenario, with reports focusing on June and the upcoming month, I expect inflation to stay relatively in check. The forecasts suggest a 0.2% increase in CPI and a 0.1% month-over-month increase.

There don't appear to be any significant disruptions to the underlying market trends, so the market should remain relatively stable until Thursday when we receive the claims and continuing claims data, followed by CPI and then PPI on Friday.

These numbers are expected to be reasonably supportive, and I don't anticipate any major issues. I will provide updates as we see this week's market action unfold. Looking Back on Last Week

title="YouTube video player" frameborder="0" allow="accelerometer; autoplay; clipboard-write; encrypted-media; gyroscope; picture-in-picture; web-share" referrerpolicy="strict-origin-when-cross-origin" allowfullscreen></iframe>

Looking back on Last Week’s action

The S&P 500 (+2.0%) and Nasdaq Composite (+3.5%) reached new all-time highs during last week’s holiday-shortened week, primarily driven by gains in mega-cap stocks. However, the equal-weighted S&P 500 saw a 0.4% decline. The Vanguard Mega Cap Growth ETF (MGK) rose by 3.9%, with Tesla (TSLA) standing out by surging 27% due to better-than-expected Q2 delivery numbers.

This strong performance in mega-cap stocks boosted the S&P 500's communication services (+3.9%), consumer discretionary (+3.8%), and information technology (+3.9%) sectors to lead the 11 sectors.

Despite the gains, there were growth concerns this week. The June ISM Manufacturing Index indicated a contraction (below 50 reading), and the June Employment Situation Report showed a weakening labor market. The primary concern for investors is the potential impact of slowing economic activity and consumer spending on earnings growth.

Nevertheless, the jobs report influenced market expectations for interest rate cuts. According to the CME FedWatch Tool, the probability of a 25-basis point rate cut at the September FOMC meeting increased to 76.3% from 64.1% the previous week.

Treasury yields fell in response to the data, with the 10-year note yield decreasing by seven basis points to 4.27% and the 2-year note yield dropping 12 basis points to 4.60%. Despite the rate decline, worries about an economic slowdown and a softening labor market prevented broad support for equities.

·Nasdaq Composite: +22.3% YTD

·S&P 500: +16.7% YTD

·Dow Jones Industrial Average: +4.5% YTD

·S&P Midcap 400: +4.1% YTD

·Russell 2000: -0.02% YTD

Upcoming Economic Events and Forecasts

July 8

- 15:00 ET: Consumer Credit for May will be released, with low trading impact expected. The KR Forecast is unavailable, but the consensus anticipates a $9.5 billion increase compared to the prior value of $6.4 billion.

July 9

- 06:00 ET: NFIB Small Business Optimism report for June will be published. This report is expected to have a low trading impact, with no available KR Forecast or consensus figures, following a prior reading of 90.5.

July 10

- 07:00 ET: The MBA Mortgage Applications Index for the week of July 6 will be announced, with a low trading impact. No KR Forecast or consensus figures are available for this report, which previously showed a 2.6% change.

10:00 ET: The May wholesale Inventories report will be released with a low trading impact. The KR Forecast and consensus both expect a 0.6% increase following a prior 0.1% increase.

- 10:30 ET: EIA Crude Oil Inventories for July 6 will be reported, with a high trading impact expected. No KR Forecast or consensus figures are available, but the previous report showed a decrease of 12.16 million barrels.

July 11

- 08:30 ET: The Initial Claims report for the week of July 6 will be released, with a high trading impact expected. The KR Forecast is 235,000, and the consensus is 234,000, compared to the prior value of 238,000.

- 08:30 ET: The continuing claims report for the week ending June 30 will be published, and a high trading impact is expected. No KR Forecast or consensus figures are available, with the previous report showing 1.858 million claims.

- 08:30 ET: Consumer Price Index (CPI) for June will be announced, expected to have a high trading impact. The KR Forecast and consensus predict a 0.1% increase, following a previous reading of 0.0%.

- 08:30 ET: The June Core CPI will also be released, with a high trading impact. The KR Forecast and consensus predict a 0.2% increase, consistent with the prior reading.

10:30 ET: EIA Natural Gas Inventories for the week of July 6 will be published. They are expected to have a low trading impact. No KR Forecast or consensus figures are available, but the previous report showed an increase of 32 billion cubic feet.

- 14:00 ET: The June Treasury Budget will be released, with low trading impact. No KR Forecast or consensus figures are available, but the prior report showed a deficit of $347.1 billion.

July 12

- 08:30 ET: Producer Price Index (PPI) for June will be released, with high trading impact expected. The KR Forecast and consensus both predict a 0.1% increase, following a prior decrease of 0.2%.

- 08:30 ET: The June core PPI will be announced, also with a high trading impact. The KR Forecast and consensus predict a 0.1% increase, consistent with the previous reading.

- 10:00 ET: The preliminary University of Michigan Consumer Sentiment index for July will be published and is expected to have a high trading impact. The KR Forecast predicts a reading of 67.0, with the consensus at 67.5, compared to the prior value of 68.2.

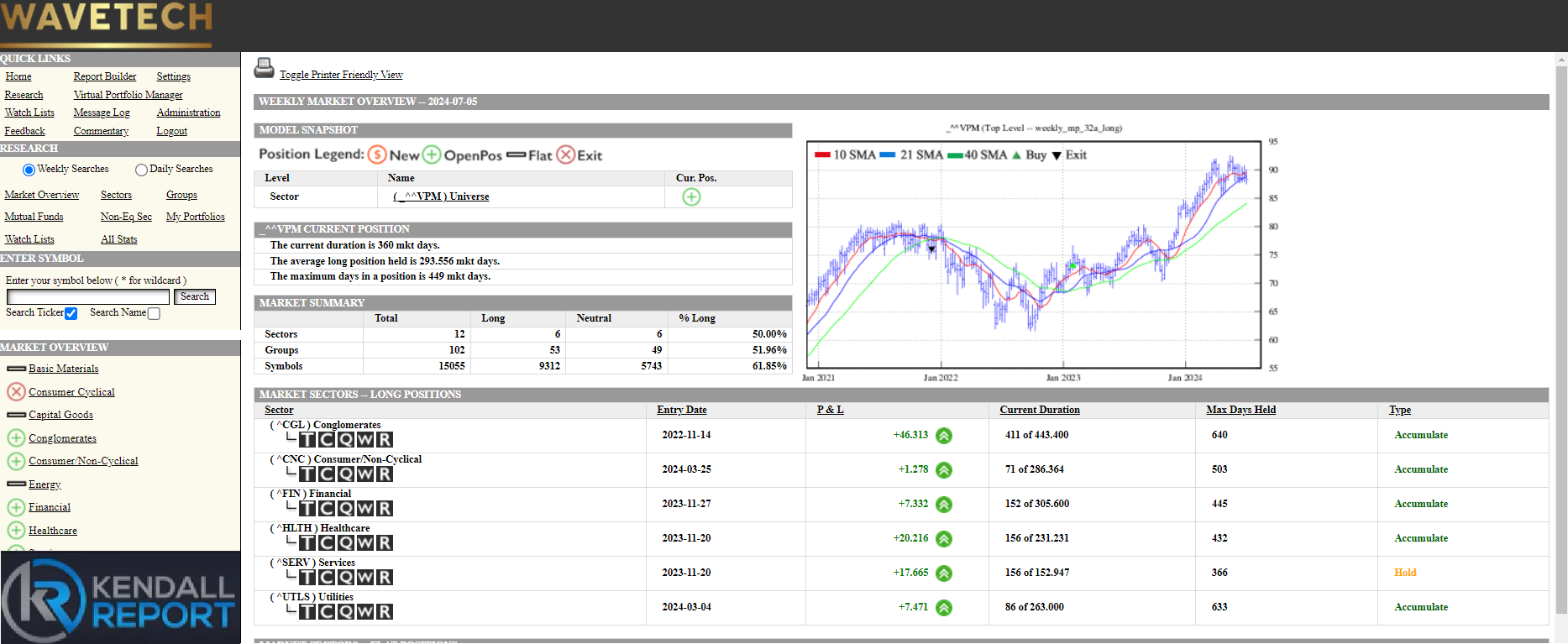

WaveTech Database

Another week brings the same story. For about six weeks, I anticipated the intermediate database would experience reasonable selling, indicating a rotation in its holdings. However, this hasn't materialized. Instead, we've seen gradual buying and selling each week. The database is 61.85% bullish, with 321 new entries and 227 exits.

The short-term database has generated 11,148 new entries with 500 exits, moving its bullish percentage to 51.14%. This increased traction in the short-term models suggests that the underlying trends remain strong, with no significant shifts in the database.

One notable change is an exit signal in the consumer cyclical sector, down about 7.5%. This trade has exited, leaving us six of the 12 sectors long.

S&P 500 Futures

Keep reading with a 7-day free trial

Subscribe to The Kendall Report to keep reading this post and get 7 days of free access to the full post archives.