“Resilience vs. Volatility: WaveTech Analysis Flags Standoff Between Bulls and Macroeconomic Pressures”

KR Opinion

The market demonstrated remarkable resilience Wednesday despite initial signs of a significant decline. Buyers stepped in after an early session drop to the RTX support level on the market grid, leading to a substantial recovery of early losses. While the higher-than-expected inflation data pushed the 10-year yield up to 4.6%, market participants maintained their buying momentum, continuing the fascinating support pattern at key technical levels.

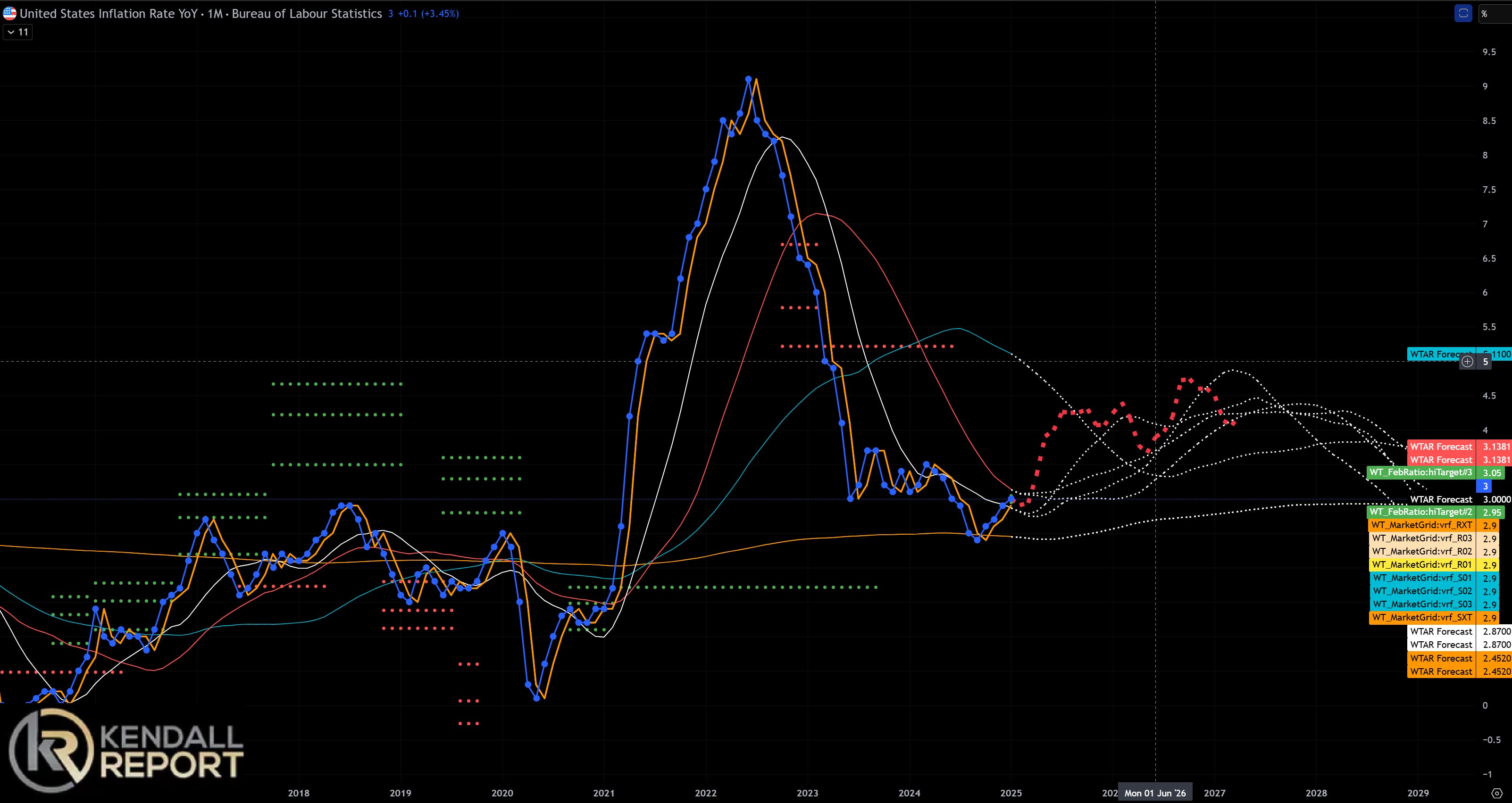

The broad market database, analyzing over 14,000 symbols, showed a slight negative rotation in short-term models, suggesting underlying stability despite market volatility. The inflation trajectory remains consistent with previous forecasts, with the red dot indicator suggesting a potential bounce to 3.8% or even 4.2%. This aligns with the ongoing discussion about inflation's echo effect that has been highlighted over the past six months.

Looking ahead, significant challenges remain, particularly regarding the post-election landscape. Current projections suggest a potentially negative third quarter, with concerns about a technical recession extending into 2026. The anticipated federal government workforce reduction of 80,000 to 100,000 employees is a key factor in this outlook. Historical patterns suggest that severance packages, while providing temporary financial cushions, often lead to delayed job searches and potentially problematic spending behaviors among affected workers.

The market's resilience persists despite the sharp move in 10-year yields from 4.4% to 4.6%. As we approach Thursday's economic releases, including PPI numbers and initial and continuing claims, the potential for increased volatility remains high, especially if the PPI data mirrors today's hotter-than-expected CPI figures.

The algorithmic indicators and database analysis suggest market stabilization, though the current sideways trading pattern appears firmly established. Breaking out of this range will likely require significant catalyst events or shifts in market sentiment. The WaveTech analysis confirms this stability pattern while highlighting the ongoing tension between bullish buying pressure and macroeconomic headwinds.

Looking Back on Wednesday Action

The financial markets experienced a challenging session following the release of January's Consumer Price Index data, which came in higher than anticipated. The inflation report showed total CPI rising to 3.0% year-over-year from December's 2.9%, while core CPI increased to 3.3% from 3.2%. This unexpected uptick in inflation triggered a significant response in the Treasury market, with the 10-year yield climbing from 4.53% to 4.64% and the 2-year yield rising by eight basis points to 4.37%.

The major stock indices reflected mixed performance, with the S&P 500 declining 0.3% and the Dow Jones Industrial Average falling 0.5%, though both recovered somewhat from their session lows. The Nasdaq Composite achieved a small gain, supported primarily by strength in major technology stocks.

Tech giants played a crucial role in the market's partial recovery, with Apple shares rising 1.8% to $236.87 and Meta Platforms gaining 0.8% to $725.38. Both stocks showed resilience by rebounding from earlier losses. Several individual stocks posted notable performances, particularly those reporting earnings. DoorDash surged 4.0% to $200.89, Gilead Sciences jumped 7.5% to $103.31, and Confluent saw an impressive gain of 25.1% to $37.65. All three reached new 52-week highs.

However, the broader market sentiment remained negative, as evidenced by declining performance in nine of the eleven S&P 500 sectors. The energy sector was the day's worst performer, dropping 2.7%, while the real estate sector, susceptible to interest rate movements, fell 0.9%. This sector-wide weakness underscored the market's ongoing concerns about inflation and its implications for monetary policy.

This market behavior reflects investors' heightened sensitivity to inflation data, its potential impact on Federal Reserve policy, and the continuing influence of major technology stocks in supporting market levels despite broader weakness.

· Dow Jones Industrial Average: +4.3% YTD

· S&P Midcap 400: +1.6% YTD

· Russell 2000: +1.2% YTD

· S&P 500: +2.9% YTD

· Nasdaq Composite: +1.8% YTD

Reviewing Wednesday's economic data:

Weekly MBA Mortgage Applications Index 2.3% (Prior 2.2%)

January CPI 0.5% (KR Forecast consensus 0.3%) (Prior 0.4%

January Core CPI 0.4% (KR Forecast consensus 0.3%) (Prior 0.2%)

Thursday's economic reports include:

8:30 ET: January PPI (KR Forecast consensus 0.2%; prior 0.2%), January Core PPI (KR Forecast consensus 0.3%; prior 0.0%), weekly Initial Claims (KR Forecast consensus 217,000; prior 219,000), and Continuing Claims (prior 1.886 mln)

10:30 ET: Weekly natural gas inventories (prior -174 bcf)

WaveTech Database