Russel Explodes Will it Continue

Will CPI Keep the Rotation going?

Important Announcement: Subscription Price Increase Starting August 1st

I have an important update regarding our subscription fees. Starting August 1st, the monthly subscription fee will increase to $19.97. However, there's still a fantastic opportunity to lock in significant savings by opting for an annual subscription. If you pay for a full year, the cost is only $80.00, just $6.67 monthly.

Why the Increase?

After nearly six months of delivering high-quality content and evaluating the time and effort required, it’s clear that an adjustment is necessary. Additionally, compared to other services in this space, our new rate is still highly competitive—many charge double my monthly rate. This increase will allow us to continue providing exceptional value and ensure the sustainability of our work.

Act Now and Save!

By opting for the annual subscription before the end of this month, you can avoid the price increase and enjoy the same great content at a significantly reduced rate of $6.67 per month. After July, the annual subscription will still offer a discount, but the price will reflect the new monthly rate.

Thank you for your understanding and continued support. The initial $8 monthly fee was always intended as an introductory rate, and we’re thrilled to have so many of you on board. Maintaining this environment requires substantial effort; we believe this adjustment is fair and necessary.

We plan to release exciting content and new developments in the future, and we look forward to sharing them with you.

Best regards, Bob Kendall

KR Opinion

The anticipated release of the CPI showed a downtick, which initially seemed highly bullish. Markets reacted positively, trading higher at first but fading throughout the session, with the S&P 500 and NASDAQ finishing down.

The standout performer was the Russell 2000, which saw a significant surge. This surge triggered a massive influx of new buys in the short-term database, driving the percent bullish to new highs. The mid and small-cap asset classes primarily drove this shift, as multiple new sectors showed strength.

The market perceived lower rates might be on the horizon, signaling that inflation might be under control and improving economic conditions. The employment and claims data came out slightly better than expected, with no major surprises except for the downtick in inflation.

I've been discussing the likelihood of decreasing inflation for some time, and the June numbers support this view. However, I still believe we will see an uptick in inflation in August and September. For now, the market sentiment has turned positive.

Despite the down session in the major indices, the database remained bullish. This is an exciting development because, typically, a down session would lead to a negative database. However, the small-cap stocks, often called "zombie companies," have shown a resurgence and may lead the markets in a new direction.

I'll be covering the Russell 2000 in more detail to provide perspective. It's crucial to watch this index before the market opens on Friday, especially with the upcoming CPI release. We might see a similar pattern where a better-than-expected number unexpectedly affects the market.

There's a common adage that good news can be bad news and vice versa. In this case, what was perceived as good news turned sour for the major indices, leading to significant profit-taking in the S&P 500 and NASDAQ.

Is this development material? Probably not. I've been suggesting that the major indices might flatten out in the current situation, even as they continue to hit all-time highs. Now, we can see some consolidation, making it essential to focus on Russell 2000.

The last time I covered it, I mentioned upward Fibonacci targets, and I'll provide more details shortly. The recent move has brought the index to the upper end of its previous range, driven by a significant money flow into small caps.

As we approach Friday, another major news release is expected, likely bringing more volatility. We saw an RTX sell signal on Wednesday and an STX buy signal on Thursday, indicating a potential for a broad trading range. While the markets were projected to end lower on Thursday, we are now setting up for normalization and a broad trading range.

Looking back on Thursday

“Good news turns bad.” Following a favorable CPI report for June, the S&P 500 and Nasdaq Composite still ended in the red with 0.9% and 2.0% declines, respectively. The report showed a 0.1% month-over-month decrease in total CPI, reducing the year-over-year growth rate to 3.0% from 3.3% in May. Core-CPI, excluding food and energy, also decelerated to 3.3% year-over-year from 3.4%.

This report sent market rates lower, reflecting optimism about the inflation trajectory and Federal Reserve policy. The yield on the 10-year Treasury note, which is highly sensitive to inflation expectations, dropped by nine basis points to 4.19%. Meanwhile, the 2-year Treasury note yield, more responsive to changes in the federal funds rate, fell by 12 basis points to 4.51%.

The Fed funds futures market now prices in a 92.7% probability of a rate cut at the upcoming June FOMC meeting, a significant increase from 73.4% the previous day.

Despite a broad market rally, mega-cap and semiconductor stocks declined due to profit-taking after their recent strong performance. The Vanguard Mega Cap Growth ETF (MGK) fell by 2.3%, and the PHLX Semiconductor Index (SOX) dropped by 3.5%.

This adverse price action in critical sectors weighed on the S&P 500 and Nasdaq Composite. In contrast, the Russell 2000 surged 3.6%, and the S&P Mid Cap 400 posted a 2.5% gain. The equal-weighted S&P 500 saw a 1.2% increase.

Tesla (TSLA), a significant player in the mega-cap space, was a notable laggard. It dropped 8.4% to $241.03 after Bloomberg reported a delay in its robotaxi plans until October. At its peak, Tesla's stock had been up nearly 3% earlier.

Meanwhile, rate-sensitive areas of the market benefited from the decline in rates. The S&P 500 real estate sector jumped 2.7%, and homebuilder stocks saw significant gains. The SPDR S&P Homebuilder ETF (XHB) surged 5.9% in response to the favorable movement in market rates.

·Nasdaq Composite: +21.8% YTD

·S&P 500: +17.1% YTD

·Dow Jones Industrial Average: +5.5% YTD

·S&P Midcap 400: +7.7% YTD

·Russell 2000: +4.9% YTD

Reviewing Thursday’s economic data:

- Weekly Initial Claims were 222K, with the KR Forecast at 234K; the prior was revised to 239K from 238K. Weekly Continuing Claims were 1.852 million; the prior was revised to 1.856 million from 1.858 million.

The key takeaway from the report is that initial claims continued backtracking from a high reached in June, suggesting that the labor market is holding up well despite the Fed's restrictive policy.

- June CPI was -0.1%, with the KR Forecast at 0.1%; the prior was 0.0%. June Core CPI was 0.1%, with the KR Forecast at 0.2%; the prior was 0.2%.

- The key takeaway from the report is that the market heard exactly what it hoped for, as CPI deflated slightly in June, contributing to additional disinflation on a year-over-year basis. The 3.0% year-over-year growth rate matched the low from 2023, which will be seen as supportive of a case for a rate cut from the FOMC.

Market participants will receive the following economic data on Friday:

- 8:30 ET: June PPI (KR Forecast 0.1%; prior -0.2%) and Core PPI (KR Forecast 0.1%; prior 0.0%)

- 10:00 ET: Preliminary July University of Michigan Consumer Sentiment (KR Forecast 67.5; prior 68.2)

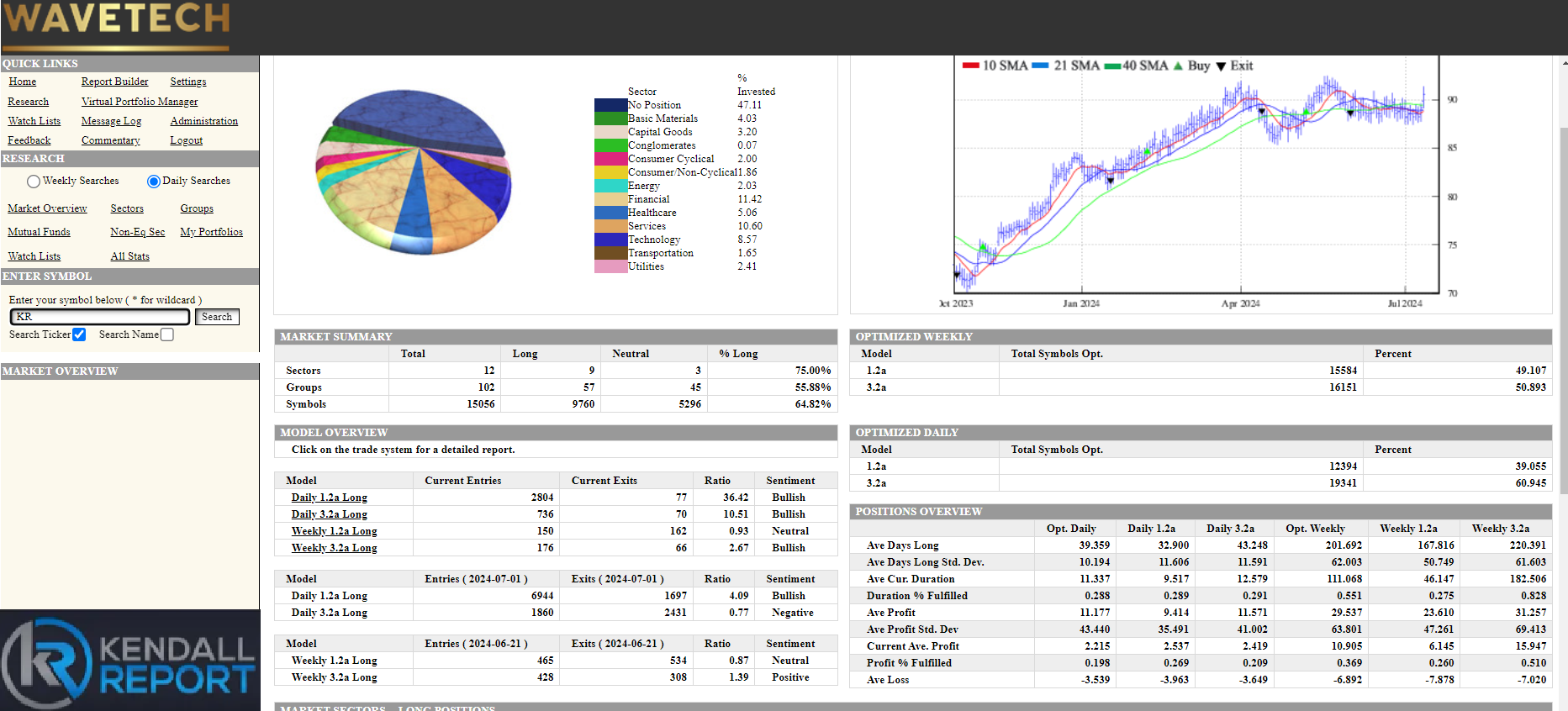

WaveTech Database

As I mentioned in the opening comments, despite the significant indices being down, we did not see a negative rotation in the database. On the contrary, there was a significant positive shift on a short-term basis. We saw 3,542 new buy signals and only 147 exits, indicating a strong bullish ratio.

Most of these stocks are within the mid-cap and small-cap asset classes. This positive influence is expected to carry over and affect the intermediate models that will be run after the close tomorrow. Therefore, we are unlikely to see a downtick in the intermediate database.

Instead, we will likely witness further rotation and an extension of the forward-looking intermediate trend model I've been discussing for months.

The continuation of the market's uptrend into at least September or October is becoming more plausible by the day. The recent surge in secondary stocks, particularly in the mid-cap and small-cap asset classes, supports this outlook.

New Sector Buys for the Short-Term Models.

I anticipate gaining more traction for Friday's intermediate run, pushing the intermediate bullish percentage well over 62%, potentially reaching as high as 64% or 66%. This expectation is based on the current momentum and the substantial number of new buy signals observed in the short-term database.

The ongoing strength in mid-cap and small-cap stocks is a key driver of this bullish trend. It indicates a robust market environment that should sustain the uptrend in the coming months.

S&P 500 Futures