Tech Stocks in Focus!

Bitcoin Breaks 73,500 will it continue?

KR Opinion

The market continues demonstrating remarkable resilience as we enter a pivotal period marked by major earnings releases and significant economic reports. Despite algorithmic projections suggesting potential corrections toward the 21-day and 40-day moving averages on the S&P and NASDAQ, price action maintains its drift with a persistent upward bias.

Tuesday’s session saw the NASDAQ Composite achieve a new high, though NASDAQ 100 futures notably lagged below their peak levels. The Russell's relative underperformance underscores the market's current preference for large-cap names as we enter this crucial reporting period.

Taking bearish positions in the current environment has proven challenging, as meaningful downside pressure remains absent. While some profit-taking or repositioning might materialize ahead of the election, market momentum appears to be intensifying rather than diminishing. The range-bound configuration persists, suggesting a contained trading environment despite numerous potential catalysts on the horizon.

Recent JOLTS data indicated modest softening in the labor market, though the impact appears limited in scope. The downward revision to previous months' data provides additional context but doesn't fundamentally alter the market narrative. More significant is the Federal Reserve's recent 50 basis point adjustment, which some market participants view as politically timed, given its proximity to the election and the subsequent improvement in various economic metrics.

The ten-year yield's push above 4.30% to reach 4.40% challenges previous assumptions about yield curve flattening. Recent Fibonacci projections suggest potential moves toward the 4.40-4.50% range, contrary to widespread expectations of back-end curve flattening. This development adds another layer of complexity to an already intricate market environment.

As we approach next Tuesday's election, the combination of approaching political events, critical earnings reports, and evolving interest rate dynamics suggests continued market choppiness. While the overall bias remains moderately positive, traders should prepare for increased volatility through election day. While not definitively clear, the technical setup continues to argue against taking aggressive bearish positions, given the market's persistent strength.

The timing of the Fed's 50 basis point adjustment has drawn particular attention, especially considering its proximity to the election and the subsequent improvement in economic indicators. This has led some market participants to question the necessity and timing of such aggressive monetary action, particularly as longer-term yields continue their upward trajectory.

Market participants should anticipate continued choppy trading conditions while maintaining awareness of the market's demonstrated upward bias despite occasional volatility. The potential for further yield curve steepening remains in play, even as attention focuses primarily on major tech earnings and upcoming economic data releases.

The current environment demands a balanced approach, recognizing the persistent underlying strength and the potential for short-term volatility. While corrective moves remain possible, the market's demonstrated resilience suggests maintaining a constructively biased outlook while remaining prepared for increased price swings in the near term.

Looking Back on Tuesday’s Action

The Nasdaq Composite touched a historic milestone today, though futures markets painted a more cautious picture, finishing 0.8% above Monday's close. Broader market performance was more subdued, with the S&P 500 adding a modest 0.2%, representing approximately ten points. The day's gains were primarily driven by technology heavyweights and semiconductor companies, with the PHLX Semiconductor Index surging 2.3% while the Vanguard Mega Cap Growth ETF advanced 0.9%.

Alphabet emerged as a standout performer, gaining 1.7% to reach $171.14 as investors positioned themselves ahead of the company's earnings announcement after the closing bell. However, market internals revealed underlying weaknesses beneath these headline gains. The New York Stock Exchange saw decliners outpace advancers by a two-to-one margin, while Nasdaq's declining issues exceeded advancing ones by a four-to-three ratio. This divergence was further reflected in the performance of the Dow Jones Industrial Average and Russell 2000, which fell 0.4% and 0.3%, respectively.

Fixed income markets continued to influence equity sentiment, though Treasury yields ultimately settled near unchanged levels following a solid showing at the day's seven-year note auction. The $44 billion sale marked a welcome departure from recent tepid auction demand. The benchmark ten-year yield held steady at 4.27%, while the two-year yield eased two basis points to 4.12%. Earlier pressure on bonds came from stronger-than-expected October Consumer Confidence data.

Corporate earnings painted a mixed picture across sectors. Notable declines came from several industry leaders: homebuilder D.R. Horton tumbled 7.2% to $167.32, automotive giant Ford dropped 8.4% to $10.41, and pharmaceutical company Pfizer slipped 1.4% to $28.46. Even a Dow component, McDonald's couldn't escape the pressure, declining 0.6% to $295.00.

The day wasn't without its bright spots in earnings news. Apparel conglomerate V.F. Corp surged an impressive 27% to $21.63, while cruise operator Royal Caribbean continued its strong performance, climbing 3.2% to $210.10.

This mixed performance across sectors and the disconnect between major indices and market breadth suggests investors are becoming increasingly selective as the earnings season progresses.

The strong showing in technology and semiconductor stocks indicates continued faith in growth sectors, even as broader market participation shows signs of fatigue. With more high-profile earnings reports and crucial economic data ahead, market participants appear to be cautious despite the Nasdaq's record achievement.

The day's trading patterns reflect a market navigating multiple crosscurrents: strong performance in select technology leaders, weakness in traditional industrial and consumer sectors, and the ongoing influence of interest rates on overall market sentiment. This complex environment suggests investors carefully weigh growth prospects against valuation concerns as the earnings season unfolds.

Nasdaq Composite: +24.7% YTD

S&P 500: +22.3% YTD

Dow Jones Industrial Average: +12.1% YTD

S&P Midcap 400: +13.0% YTD

Russell 2000: +10.4% YTD

Tuesday’s Economic releases

Housing market data showed modest strength in August, with the FHFA Housing Price Index rising 0.3%, slightly above the revised prior month's 0.2% increase. The S&P Case-Shiller Home Price Index registered a 5.2% increase, exceeding the KR Forecast consensus of 5.1% and showing continued momentum in home prices, though at a slower pace than the previous 5.9% gain.

Consumer confidence surged in October, reaching 108.7, substantially above the KR Forecast consensus of 99.0. The reading marked a significant improvement from September's revised 99.2 figure.

The surge in confidence spanned across age demographics and most income brackets, with consumers expressing notably more optimistic views about future business conditions. This broad-based improvement suggests potential support for consumer spending patterns.

Labor market dynamics showed some moderation, with September's JOLTS report revealing job openings at 7.443 million, down from the revised 7.861 million in August. The international trade picture saw the goods deficit widen to $108.2 billion, deteriorating from the revised September figure of $94.2 billion.

Inventory levels showed mixed trends, with retail inventories increasing 0.8% while wholesale inventories declined 0.1%, contrasting with the previous month's 0.2% gain.

Wednesday’s Economic Calendar

Wednesday brings several significant economic releases. The day begins with the weekly MBA Mortgage Index, following last week's 6.7% decline. The ADP Employment Change report, expected at 105,000 new jobs according to KR Forecast consensus, will provide an early look at October's labor market conditions.

The preliminary third-quarter GDP reading takes center stage, with expectations holding steady at 3.0%. The accompanying GDP Chain Deflator, a key inflation indicator, is projected to show some moderation at 2.3%, down from the previous 2.5%.

Housing market activity will remain in focus with September's Pending Home Sales data. Forecasts suggest a 2.5% increase, building on August's 0.6% gain. Energy markets will digest the weekly crude oil inventory report following last week's 5.47 million barrel build.

This comprehensive slate of economic data should provide valuable insights into economic momentum across housing, employment, and broader growth trends, potentially influencing market sentiment and Federal Reserve policy considerations.

WaveTech Database

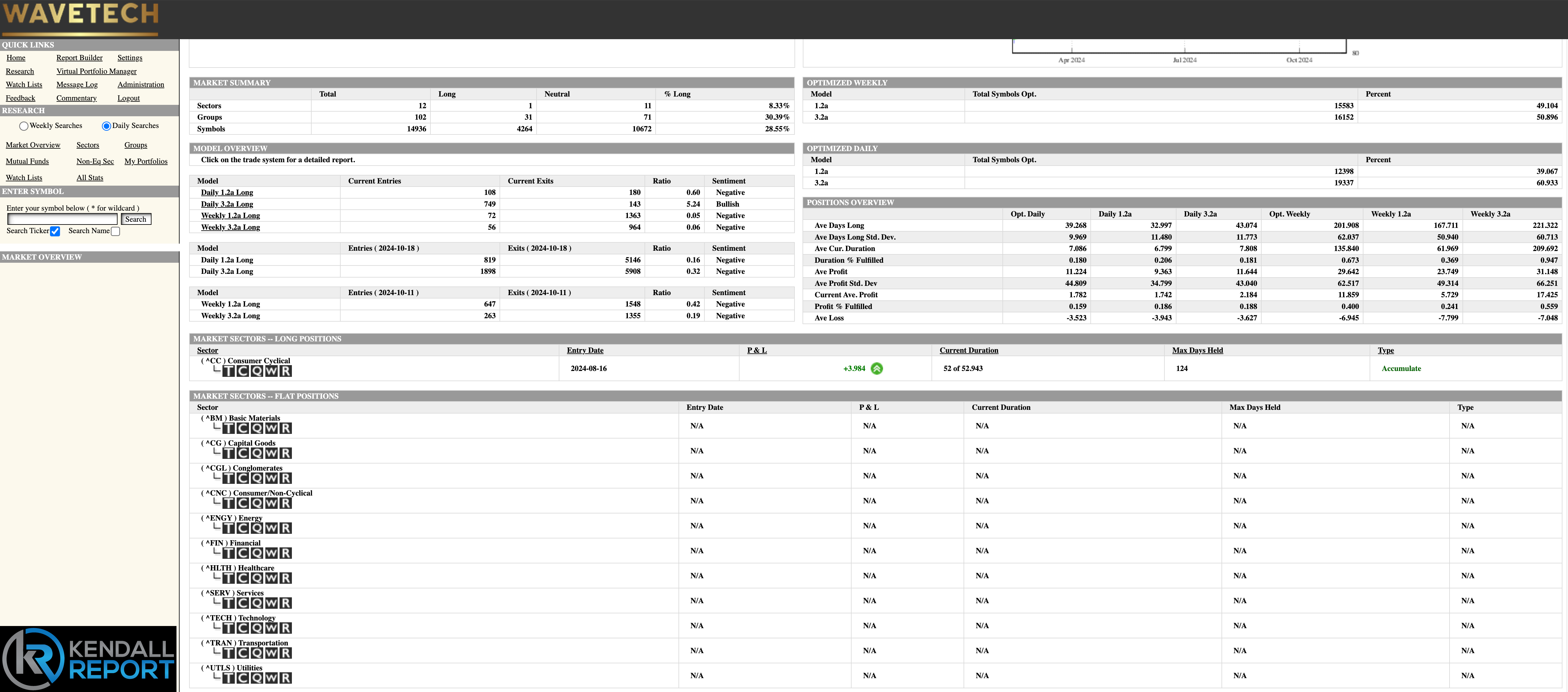

The database analysis reveals an emerging stabilization pattern. Recent activity shows 857 new entries against 323 exits, pushing the bullish percentage up to 28.55%. This movement provides important context for current market conditions, though it is not as robustly bullish as general market sentiment suggests.

In the sector analysis, consumer cyclical remains our sole long position, and it's now reaching a significant duration milestone. The sector's performance metrics tell an interesting story: current returns stand at 3.9%, notably below the typical expectation of 7.5% for similar duration periods. This places current performance approximately 30% below historical norms for comparable timeframes.

While necessary for tracking purposes, these metrics don't signal significant market shifts. Instead, they confirm our position within a choppy trading range. The bullish percentage at 28% aligns with this range-bound interpretation, suggesting a market that's neither breaking down nor breaking out decisively.

The current market environment presents an interesting disconnect between perception and technical reality. While market sentiment might feel bullish, the technical indicators paint a more nuanced picture. The occasional new highs don't represent significant breakouts but incremental moves within an established trading range.

This pattern of behavior suggests a market that's maintaining its composure while lacking the momentum for a decisive directional move. The database readings indicate a stable but not aggressively bullish environment despite what surface-level market action might suggest. The gap between the consumer cyclical sector's current returns and historical norms supports this measured interpretation of current conditions.

Stabilizing the database metrics, particularly the bullish percentage at 28.55%, provides a framework for understanding current market behavior. While new highs are occasionally printed, they occur within the context of this broader consolidation pattern rather than representing a new, more aggressive phase of the market advance.

S&P 500 Futures

A detailed analysis of the S&P 500 reveals an interesting technical narrative developing since last Wednesday's significant downward reversal and subsequent rebound. The index has maintained a position above the 21-day moving average, suggesting continued resilience within the broader pattern structure. Despite this strength, algorithmic projections continue pointing toward a retest of the 21-day moving average, with an ultimate move toward the 40-day moving average.