KR Opinion

As we approach Wednesday's trading session, all eyes are on NVIDIA's (NVDA) upcoming earnings report. This highly anticipated event will have significant implications for the tech giant and potentially for the broader market.

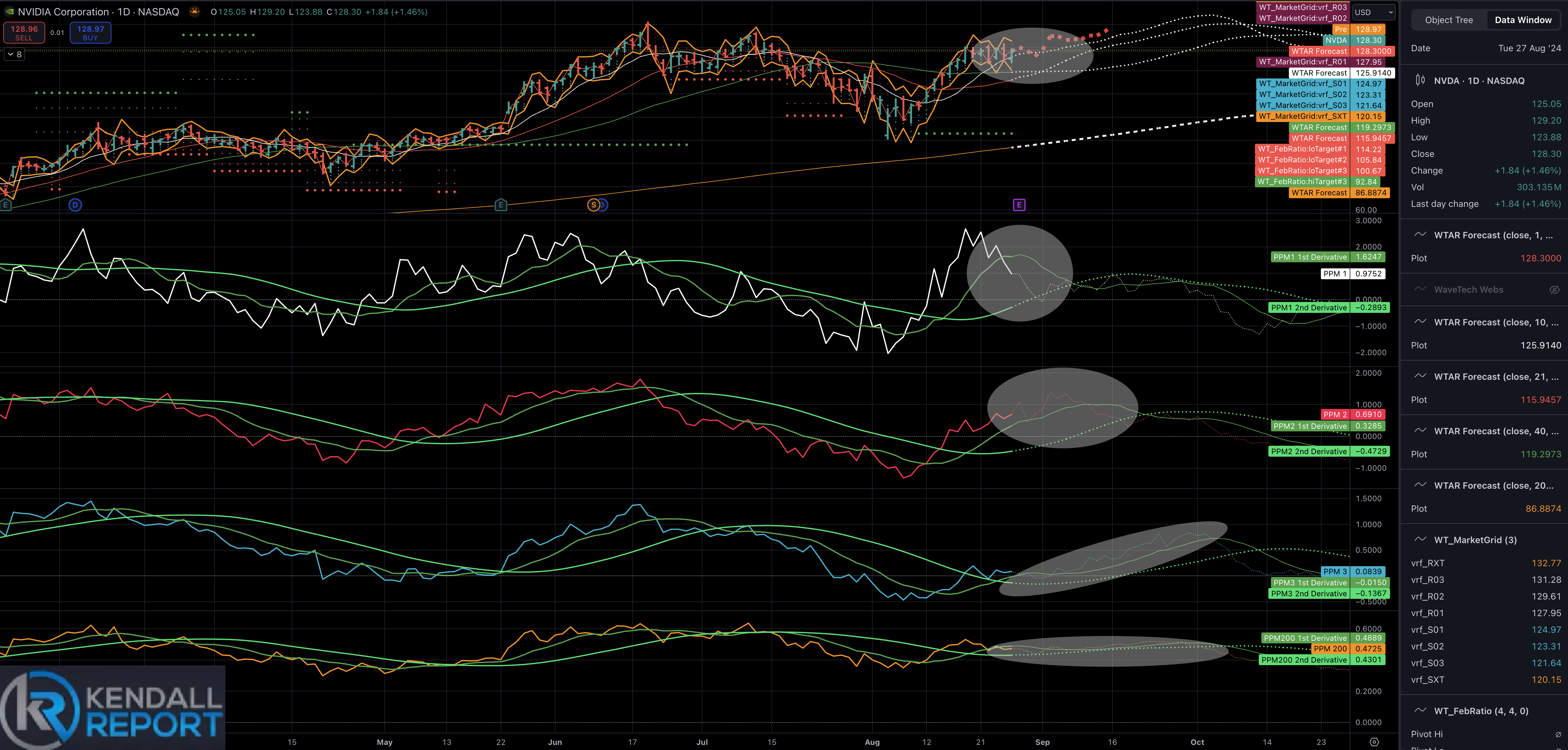

NVIDIA Stock Analysis:

NVDA's daily chart shows a positive configuration, maintaining an upward slope. Tuesday's trading saw an encouraging reversal - the stock dipped below its 10-day moving average but rebounded strongly. However, it's worth noting that momentum is beginning to wane slightly.

Key levels to watch for NVIDIA:

- Support: $126.95 - $125.54

- Resistance: $131.07 - $132.52

While there's still a slight upward bias, most of the earnings impact will be felt on Thursday, as the report comes after Wednesday's market close. We may see some pre-earnings jitters as traders adjust their positions before the announcement.

Despite the positive expectations surrounding NVIDIA, we're observing a gradual erosion of upward momentum in the broader market. This trend, which I've highlighted for several sessions, has yet to breach key support levels. However, it suggests we may be in for a moderate decline over the coming days.

It's important to emphasize that this doesn't appear to be the formation of a significant market top. Instead, it is a natural cooling-off period after recent gains.

Upcoming Market Catalysts:

1. NVIDIA Earnings: The after-hours report on Wednesday will likely set the tone for Thursday's trading session.

2. Weekly Jobless Claims: As we approach the end of the week, the usual unemployment data releases are taking on increased significance. These figures have been more pronounced, impacting market sentiment in recent months than earlier in the year.

In conclusion, while the NVIDIA earnings report is the headline event, it's crucial to monitor the broader market dynamics. The subtle shift in momentum we're seeing could lead to short-term volatility, mainly as we process the NVIDIA news and late-week economic data.

Looking Back on Tuesday’s Action

In Tuesday’s market action, we saw modest gains in major indices as investors remained cautious ahead of the long weekend. The S&P 500, Nasdaq Composite, and Dow Jones Industrial Average closed slightly higher, while the Russell 2000 bucked the trend with a 0.7% decline.

Trading volume was lighter than usual, reflecting the approaching Labor Day holiday and a general lack of market-moving news. Investors also seemed to be holding their breath in anticipation of NVIDIA's earnings report, due after Wednesday's close.

Despite the cautious sentiment, there were some bright spots in the market. The semiconductor sector showed strength, with the PHLX Semiconductor Index rising 1.1%. This gain helped to offset some of the losses the industry has experienced earlier in the week.

Mega-cap stocks also performed well, particularly in the technology and healthcare sectors. Apple made headlines by announcing Kevan Parekh as its new CFO, while Eli Lilly drew attention by introducing a savings program for its weight loss drug, Zepbound. The program offers significant discounts for non-covered patients with valid prescriptions.

Sector performance was mixed across the S&P 500. Information technology and financials led the pack, representing nearly half the index's weight. On the other hand, the energy sector struggled as oil prices fell, with WTI crude futures dropping 2.3% to $75.61 per barrel.

In the bond market, we saw some movement in yields. The 2-year Treasury note yield decreased by three basis points to 3.90%, while the 10-year note yield increased one basis point to 3.83%. These changes followed a well-received $69 billion 2-year note auction.

As we head into the holiday weekend, market participants will closely watch for any developments that could impact trading when markets reopen. The upcoming NVIDIA earnings report remains a focal point, with potential ripple effects across the S&P 500: +18.3% YTD

· Nasdaq Composite: +18.0% YTD

· S&P Midcap 400: +10.6% YTD

· Dow Jones Industrial Average: +9.5% YTD

· Russell 2000: +8.6% YTD

Tuesday's economic data brought a positive surprise in consumer sentiment. The Conference Board's Consumer Confidence Index for August came in at 103.5, surpassing the KR Forecast consensus estimate of 100.0. This marks an improvement from July's upwardly revised figure of 101.9.

However, the report had its caveats. A critical insight from the data suggests that consumers are becoming increasingly wary about labor market conditions. This growing concern could impact consumer spending habits in the future. If this anxiety about the job market persists, we might see consumers deferring discretionary purchases, which could have broader economic implications.

Looking ahead to Wednesday, the economic calendar is relatively light:

At 7:00 AM ET, we'll see the release of the weekly MBA Mortgage Applications Index. This report provides insights into the demand for home purchases and refinancing activity.

Later, at 10:30 AM ET, the Energy Information Administration (EIA) will release its weekly Crude Oil Inventories report. This data is crucial for understanding supply and demand dynamics in the oil market, which can influence energy sector stocks and broader market sentiment.

WaveTech Database

Keep reading with a 7-day free trial

Subscribe to The Kendall Report to keep reading this post and get 7 days of free access to the full post archives.