The Squeeze Continues... ATH!

Bitcoin to Surge...

KR Opinion

In recent reports, I've discussed how the markets are being squeezed higher despite algorithms indicating a flat market. We're witnessing a solid surge driven primarily by NVIDIA and the so-called "Magnificent 7," which are posting impressive numbers. Many market participants who cannot explain these rallies often label them as bubbles. However, it's crucial to understand that such market conditions can persist, especially with low volume and volatility.

Yesterday, we saw a hint of increasing volatility, and we might see more in the coming days, with the Consumer Price Index (CPI) being released on Thursday and the Producer Price Index (PPI) on Friday. These events are likely to push prices higher. I'll cover this in more detail in the technical section shortly, but both the S&P and NASDAQ signal the potential for much higher prices.

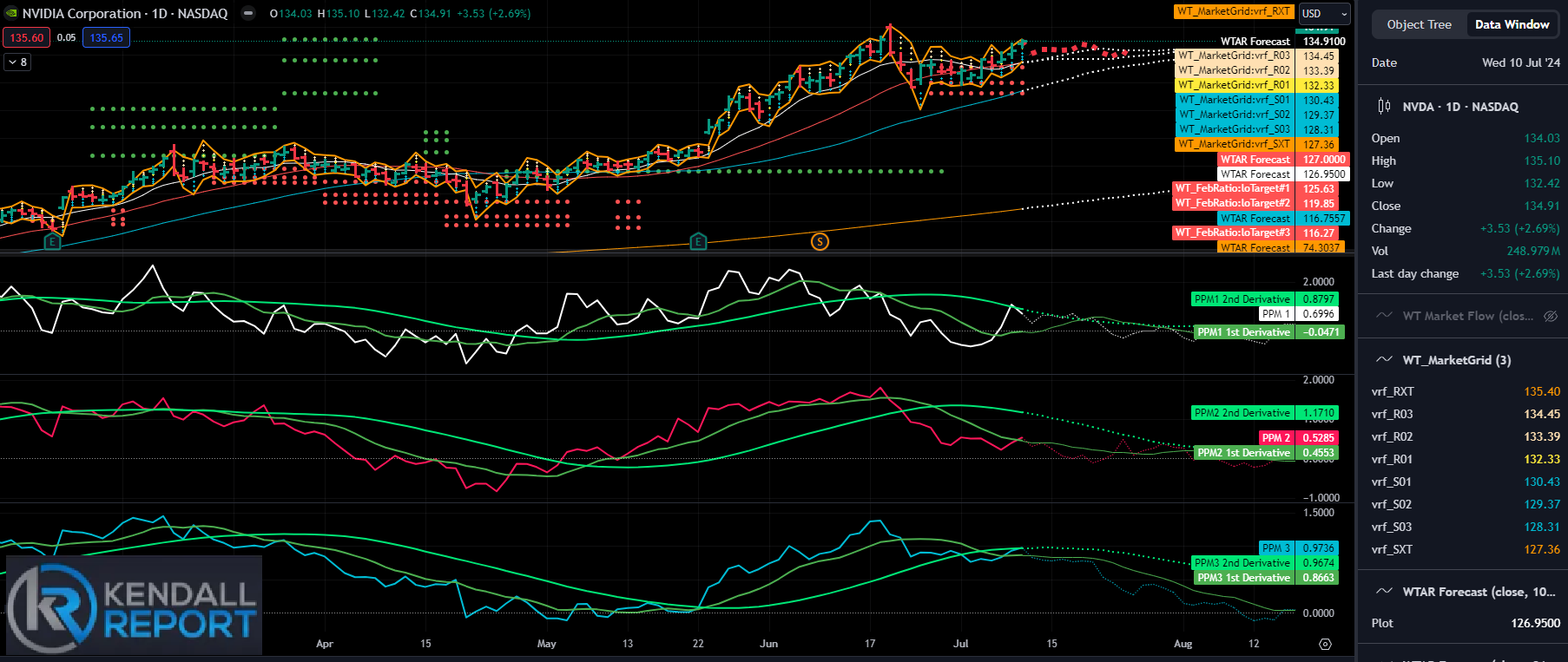

Let's focus on NVIDIA. Previously, I mentioned that we might see a flat or downward movement, but algorithms now suggest a potential pattern failure. The high on June 20th was 140.76; we saw a high of 135.10 last Thursday, nearing extreme levels on the weekly chart. We hit the R3 resistance at 135.14 with an intraday high of 135.10. The RXT number is 138.02, indicating we are meeting upward projections for this week. Although we might see some flatness in the coming two weeks, the strong momentum suggests the overall trend will remain intact, with less than a 10% chance of a trend failure in the intermediate term.

We are at least two weeks from testing the 10-week moving average, currently at 116.20 and rising approximately $5 per week. In two weeks, it will be at the 126+ level. Momentum remains strong, and Fibonacci targets at 156-169 suggest further long-term upward potential, though these levels may not be reached in the next few weeks.

The "Magnificent 7," including Apple and Microsoft, are also experiencing strong bids, indicating no significant turnarounds are expected until possibly the end of August or September.

Regarding the CPI numbers coming out today, I suspect they will align with expectations, with a potential slight surprise. As I've mentioned, we're looking at data from a month ago, so Thursday's numbers will be for June. We won't see the echo bounce in inflation until August or September, with those numbers being released in September and October. We'll be operating on these lower numbers for now.

A quick comment on Jay Powell's recent testimony: he reiterated that the Fed still needs more data before considering rate cuts. Fed funds futures have been a poor indicator, with a 73% probability that the Fed will lower rates in September, which I doubt will happen. Remember, the Fed has access to data before it's publicly released, so their actions in September will reflect their knowledge of August's inflation numbers. As we approach the July meeting, I'll update my expectations accordingly.

Important Announcement: Subscription Price Increase Starting August 1st

I have an important update regarding our subscription fees. Starting August 1st, the monthly subscription fee will increase to $19.97. However, there's still a fantastic opportunity to lock in significant savings by opting for an annual subscription. If you pay for a full year, the cost is only $80.00, which is just $6.67 per month.

Why the Increase?

After nearly six months of delivering high-quality content and evaluating the time and effort required, it’s clear that an adjustment is necessary. Additionally, compared to other services in this space, our new rate is still highly competitive—many charge double our monthly rate. This increase will allow us to continue providing exceptional value and ensure the sustainability of our work.

Act Now and Save!

By opting for the annual subscription before the end of this month, you can avoid the price increase and enjoy the same great content at a significantly reduced rate of $6.67 per month. After July, the annual subscription will still offer a discount, but the price will reflect the new monthly rate.

Thank you for your understanding and continued support. The initial $8 monthly fee was always intended as an introductory rate, and we’re thrilled to have so many of you on board. Maintaining this environment requires substantial effort; we believe this adjustment is fair and necessary.

We plan to release exciting content and new developments in the future, and we look forward to sharing them with you.

Best regards, Bob Kendall

Looking Back on Wednesday’s Action

The stock market performed robustly today, with the major indices each rising by more than 1.0%. This movement resulted in the S&P 500 (+1.02%) closing above 5,600 for the first time ever.

However, today's trading volume was below average, reflecting investor hesitation ahead of tomorrow's June Consumer Price Index release and Friday's commencement of earnings season.

Significant gains in mega-cap and semiconductor-related stocks bolstered the market. The PHLX Semiconductor Index (SOX) surged by 2.4%, and the Vanguard Mega Cap Growth ETF (MGK) increased by 1.0%. Leading the charge were NVIDIA (NVDA 134.93, +3.55, +2.7%), Apple (AAPL 232.98, +4.30, +1.8%), Microsoft (MSFT 466.25, +6.71, +1.5%), and Alphabet (GOOG 192.66, +2.22, +1.2%).

Bank stocks also outperformed the broader market in anticipation of earnings reports from major banks on Friday. This optimism drove the SPDR S&P Bank ETF (KBE) up by 2.0% and the SPDR Regional Banking ETF (KRE) to a 2.2% gain. Citigroup (C 66.98, +0.43, +0.7%) and JPMorgan Chase (JPM 207.80, +0.17, +0.1%) closed higher ahead of their reports, while Wells Fargo (WFC 59.72, -0.16, -0.3%) experienced a slight decline.

A broad array of stocks participated in the market's upward movement. The equal-weighted S&P 500 saw a 0.8% gain, with all 11 sectors closing higher. The information technology sector (+1.6%) led the advances, while the financial sector (+0.4%) trailed behind.

Fed Chairman Powell concluded his two-day semiannual testimony on monetary policy with an appearance before the House Financial Services Committee. Similar to his testimony before the Senate on the previous day, his remarks did not yield any surprises.

In the bond market, the yield on the 10-year Treasury note fell by two basis points to 4.28%, while the yield on the 2-year Treasury note remained unchanged at 4.63%. This price action was partly influenced by successfully reopening a $39 billion 10-year note auction.

·Nasdaq Composite: +24.2% YTD

·S&P 500: +18.1% YTD

·Dow Jones Industrial Average: +5.4% YTD

·S&P Midcap 400: +5.1% YTD

·Russell 2000: +1.2% YTD

Looking ahead, Thursday's calendar features the June Consumer Price Index at 8:30 ET. Other data include:

- 8:30 ET: Weekly jobless claims report

- 10:30 ET: Weekly EIA Natural Gas Inventories

- 14:00 ET: June Treasury Budget

Reviewing Wednesday’s economic data:

- The Weekly MBA Mortgage Applications Index dropped by 0.2% following a 2.6% decline last week.

- Wholesale inventories increased by 0.2% in May, below the KR Forecast consensus of 0.6%. This followed a revised 0.2% increase in April, initially reported as 0.1%.

- Weekly EIA Crude Oil Inventories showed a draw of 3.44 million barrels, compared to last week's significant draw of 12.16 million barrels

WaveTech Database

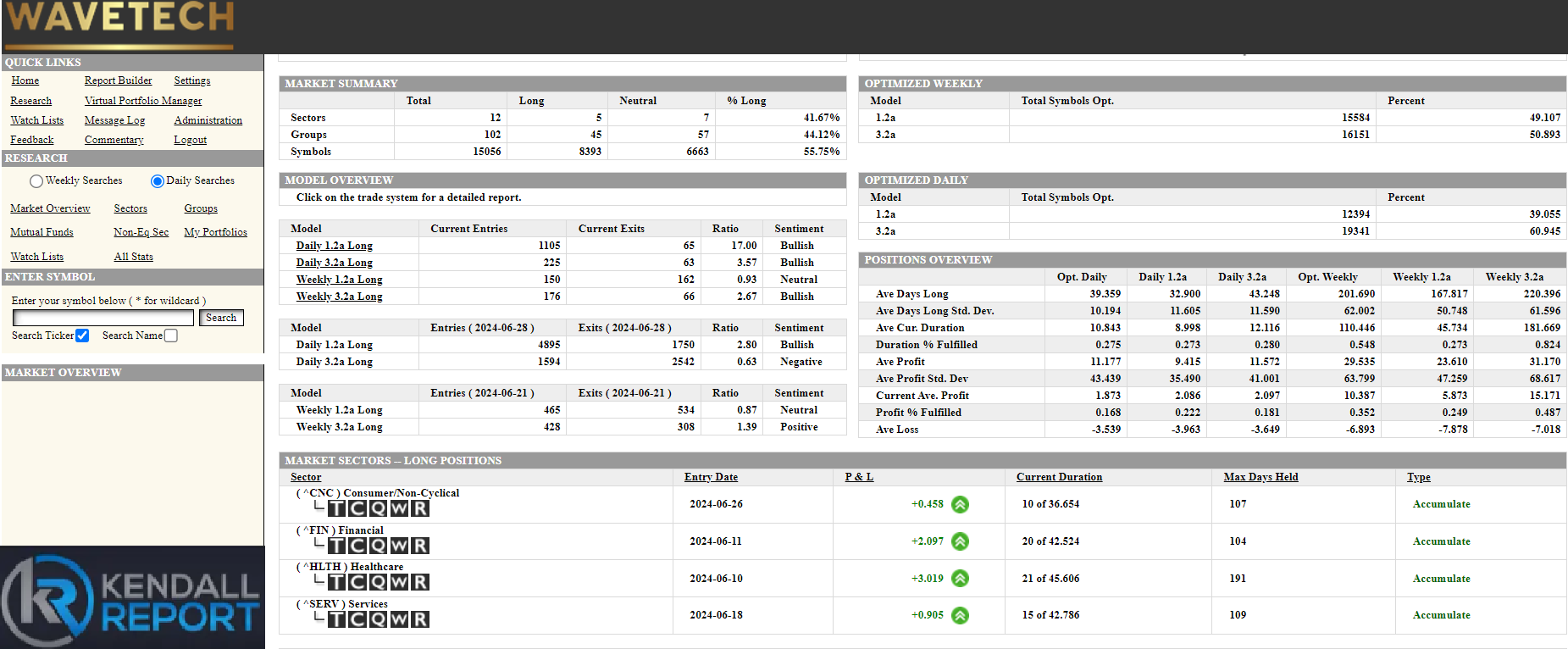

The Database continues to gain traction on a short-term basis, as evidenced by 1325 new entries and 128 exits, pushing the bullish percentage to 55.75%. Additionally, we received a new signal for the transportation sector, increasing the total to five sectors instead of four. This aligns with the broadening of sector participation that I mentioned previously, and we are now moving towards the 62% level.

As we approach the end of the week, the data will provide more insight into the intermediate models that will run on Friday. Despite my earlier expectations of some selling, we will likely remain stable unless there is a significant sell-off before Friday's close. We could see new entries rather than experiencing any rotation on an intermediate basis.

The current scenario and forward-looking expectations suggest that the short-term database has at least a 20- —to 30-day positive outlook. This implies that the overall indices and markets will likely remain positive in the near term.

S&P 500 Futures