The Strike Kicks In

Markets to Remain on the Defensive

KR Opinion

Union Strikes, Inflation, and Market Trends

The longshoremen's strike has commenced, with expectations of at least a week of logistical disruptions for each day of the walkout. The union leader's approach has been likened to a "New York mobster," raising eyebrows and concerns. He says he will “Crush us.” The timing of this strike, so close to the election and a major natural disaster, is quite concerning and has prompted speculation about whether other sectors might follow suit with similar demands for substantial wage increases.

This situation recalls the phenomenon of "strike season" in 1980s Australia. During that time, various sectors would strike in succession, each demanding wage increases. This led to significant disruptions, including food shortages and the need for emergency measures to provide essential items like milk for children.

In the current landscape, unions appear to feel more empowered, possibly due to perceived support from the Democratic Party. However, President Biden has threatened to invoke the Taft-Hartley Act, which could force strikers back to work for 90 days. The union leader's response suggests potential resistance to this measure, hinting at the possibility of reduced productivity even if work resumes.

The economic implications of these developments are significant. There's potential for widespread strikes across various sectors, which could have far-reaching economic effects. Concerns about an "echo bounce" in inflation have been growing, and recent economic indicators add to the complex picture. The JOLTS report showed increased job openings and the labor market remains firm.

Market reactions to these developments have been notable. Geopolitical risks, such as the recent conflict between Iran and Israel, have added to market volatility.

The S&P 500 experienced a significant intraday drop of 1.8% before recovering to close down 0.9%. Technical analysis suggests the potential for a further decline, with predictions of another 50 to 75 points lower.

Looking ahead, there's speculation about an "October surprise" in the context of the upcoming election, which could be this disruption caused by the Strike.

This situation presents a complex economic scenario with various interacting elements that could significantly impact markets and the broader economy in the near term.

The interplay between labor disputes, inflationary pressures, and geopolitical tensions creates a challenging economic forecasting and market prediction environment. As these situations evolve, their effects on the economy and financial markets will likely trigger higher volatility.

Looking Back on Tuesday’s action

The stock market kicked off the fourth quarter on a subdued note, with growing expectations for consolidation after a robust third quarter. Today's headlines provided ample fuel for market uncertainty, initially driven by reports of White House concerns about a potential Iranian strike on Israel. While these concerns materialized, subsequent reports indicated that Israel's defense systems successfully intercepted most of Iran's missiles.

The day's price action across equities, bonds, and commodities reflected the uncertainty surrounding the Middle East situation but showed some relief that Iran's attacks were largely unsuccessful. Significant indices closed lower, though they recovered from their worst session levels. Treasuries experienced some safe-haven buying, but these gains diminished somewhat by the close. Oil prices settled sharply higher yet pulled back from their session highs.

The market-cap weighted S&P 500 declined 0.9%, rebounding from an intraday low that saw it down as much as 1.8%. The equal-weighted S&P 500 fared slightly better, settling 0.5% lower after trading down as much as 1.1%. In the bond market, the 10-year Treasury yield, which had dropped to 3.70% after the open, settled at 3.74%, six basis points lower than Monday's close. WTI crude oil futures, after trading above $71.00 per barrel at their highs, settled at $69.74 per barrel.

Growth concerns sparked by the commencement of the East Coast and Gulf Coast dockworkers' strike and another contraction reading in the ISM Manufacturing PMI for September contributed to the day's downbeat tone.

The tech sector faced additional pressure, with Apple shares declining 2.9% following a Barclays report suggesting sluggish demand for the iPhone 16. This downturn in Apple's stock weighed heavily on the S&P 500 information technology sector, which fell 2.7%. Other tech giants like Microsoft and NVIDIA also experienced significant declines.

The market's reaction today reflected a complex interplay of geopolitical uncertainties and economic indicators while showing some relief that the situation in the Middle East didn't escalate further. As investors continue to balance various risks and uncertainties, this cautious start to the fourth quarter underscores the ongoing challenges in navigating the current market environment.

·S&P 500: +19.7% YTD (+5.5% for 11.9% YTD

·Nasdaq Composite: +19.3% YTD

·S&P Midcap 400: +11.3% YTD

·Russell 2000: +8.4% YTD

Reviewing today's economic data:

Employment Trends:

August's job openings increased to 8.04 million, up from July's revised figure of 7.711 million. This suggests a slight improvement in labor market conditions.

Manufacturing Sector:

The S&P Global US Manufacturing PMI declined to 47.3 in the final September reading, down from 47.9 in the preliminary report. This indicates a continued contraction in the manufacturing sector.

The September ISM Manufacturing Index remained unchanged at 47.2%, below the expansion threshold of 50.0%. This marks the sixth consecutive month of contraction in the manufacturing sector. The weakening employment index within this report further underscores the challenges faced by the industry.

Construction Activity:

August saw a marginal decline of 0.1% in total construction spending compared to the previous month. Private construction decreased by 0.2%, while public construction rose by 0.3%. The year-over-year increase in total construction spending stands at 4.1%. Notably, new single-family construction continued to weaken despite lower interest rates.

Looking Ahead to Wednesday

7:00 ET - MBA Mortgage Applications Index:

This weekly report will provide insights into the housing market's health. Last week's significant increase of 11.0% sets a high bar for comparison.

8:15 ET - ADP Employment Change:

According to KR Forecast, September's employment figures are anticipated to show an addition of 95,000 jobs, while the consensus estimate is 120,000. This report serves as a precursor to the official jobs report later in the week.

10:30 ET - EIA Crude Oil Inventories:

Following last week's substantial drawdown of 4.47 million barrels, this high-impact report will be closely monitored for its potential effects on energy sector stocks and oil-exporting countries' currencies

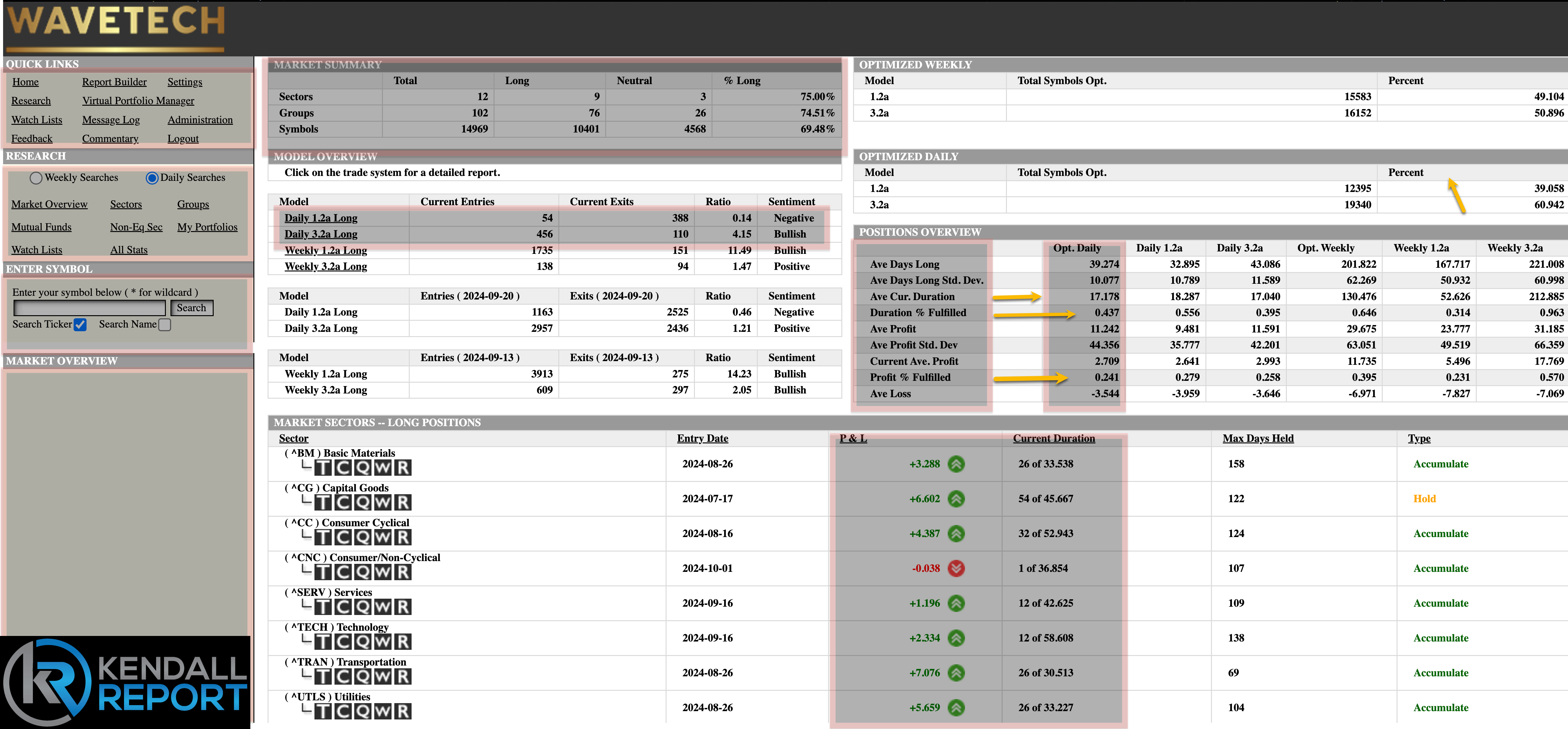

WaveTech Database

Despite Tuesday's negative market performance, our proprietary database continues to show a pattern of rotation rather than a clear directional trend. There are 510 new buy signals for Wednesday's open and 498 exits from previous positions. This activity has maintained the overall bullish percentage at a relatively high 69.48%.

This persistent bullishness in our signals, even when the broader market is down, is noteworthy. It suggests that while the overall market sentiment might be cautious, sectors or individual stocks still show strength or potential for growth.

However, as mentioned in yesterday's report, we anticipate a potential shift towards a slightly more negative rotation shortly. This expectation is based on several factors. First, Tuesday's market action showed signs of a technical breakdown. If this trend continues, we could see several more days of downward movement in the broader market indices. This sustained downward pressure often leads to more widespread negative signals in our database.

Additionally, I expect substantial news over the next three trading sessions that could impact market sentiment. Given these considerations, we project that the bullish percentage in our database could retreat to the 62-58% range. It's important to note that this doesn't indicate a major collapse in market sentiment. Instead, it represents a moderate cooling off from the current highly bullish levels.

That said, I must emphasize that this is a fluid situation. The market's reaction to upcoming news events will determine the short-term trend. We could see further deterioration in our bullish signals depending on how these events unfold and how the market responds.

In conclusion, while our database still shows overall bullish sentiment, we're entering a period when this could start to moderate. Investors should stay alert to rapidly changing conditions and be prepared for potential increases in market volatility.

The interplay between technical factors, economic data, labor disputes, and geopolitical events will likely shape market dynamics in the short term, potentially leading to shifts in our database signals and overall market direction.

S&P 500 Futures

Tuesday's trading session presented an intriguing configuration in the futures market. We witnessed a new high compared to the previous day and a significant price collapse. As the session progressed, prices penetrated the previous day's low, indicating the formation of a reversal pattern. This setup signals the three-day reversal trade pattern that we frequently discussed in my analyses.

For this pattern to be confirmed, two key events must occur on Wednesday. First, we need to see a lower low below Tuesday's level of 5733. As of the overnight session, we've seen a low of 5738, approaching but not yet breaching this critical level. Second, we need a lower close on Wednesday than Tuesday or a close below 5758. If both these conditions are met, it would confirm the downward pattern we've been anticipating for several days.