Will Employment Rollover?

KR Opinion

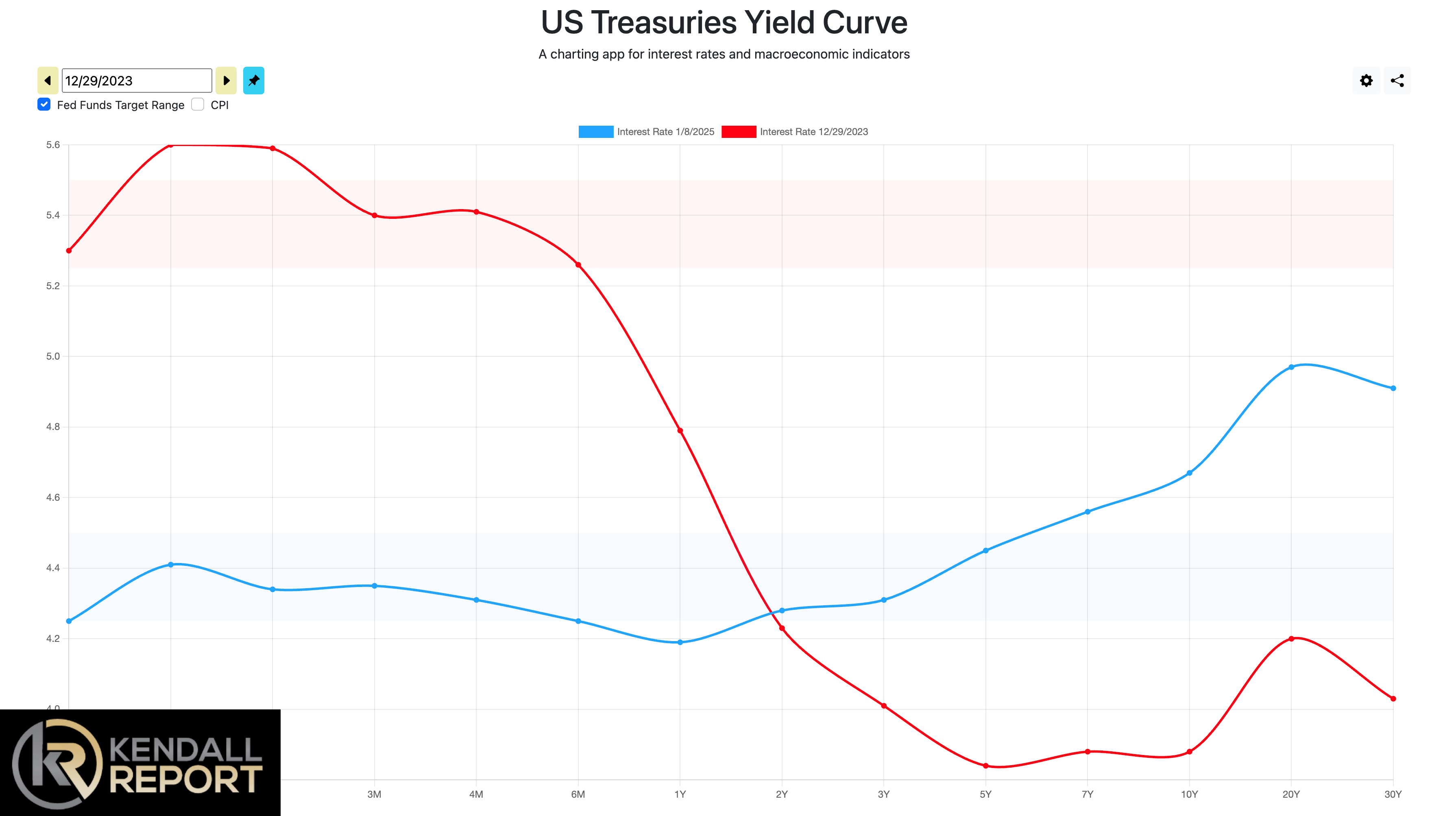

Markets remain in flux as we conclude the first week of 2025 trading, which was interrupted by Thursday's closure for President Carter's memorial. The Treasury market has been particularly active, with the 10-year yield approaching 4.70%, continuing the steepening of the yield curve projected early last year.

The upcoming Trump administration and its related legislative actions generate significant market uncertainty. Congress's efforts to develop a reconciliation bill to fund the administration's agenda have added new complexities to market assessments. The extent and execution of proposed tax cuts and tariff policies draw particular concern from market participants.

Market risks appear to be rising as we near mid-January and the inauguration. While a significant recession is not my base case, institutional positioning signals increased hedging strategies against adverse scenarios. The uncertainty surrounding policy implementation and its potential economic impacts drives a more cautious approach.

Labor market indicators are showing subtle signals. While Wednesday's ADP employment report generally met expectations, underlying trends suggest possible softening ahead. Projections indicate that unemployment may rise to about 4.3% or perhaps 4.5% in the coming months, although current jobless claims data has not yet confirmed this trajectory. The market faces additional challenges from potential immigration policy changes, which could disrupt the labor market in the upcoming quarter.

The proposed reconciliation bill adds another layer of complexity, particularly regarding government spending reductions. Given the government's position as the largest employer, significant spending cuts could materially impact economic cash flows. Potential inflation pressures, creating an "echo bounce" effect in economic data, further complicate this situation.

The Treasury market's evolution remains crucial for overall market direction, though a detailed analysis will follow next week. The persistent steepening of the yield curve continues to influence market behavior and sector positioning. These combined factors suggest heightened volatility as markets navigate the complex interplay of policy transitions and their economic implications. The environment appears primed for increased uncertainty before any clear direction emerges from the new administration's policy implementation and subsequent economic responses.

The confluence of these factors suggests markets will remain challenging to navigate until greater clarity emerges on both policy implementation and economic impacts. Traders and investors appear to be positioning for a period of increased volatility rather than making strong directional bets at current levels.

Looking Back on Wednesday's session

The Action demonstrated the market's ongoing struggle with multiple crosscurrents. The major indices showed mixed performance, with the S&P 500 advancing 0.2% and the Dow Jones Industrial Average gaining 0.3%, while the Nasdaq Composite edged lower by 0.1%. The session was characterized by volatility in both interest rates and mega-cap stocks.

Interest rates remained a key focus, with the 10-year Treasury yield reaching an intraday high of 4.73% before settling at 4.69%, up one basis point. The 2-year yield finished slightly lower at 4.29%. The Treasury market found support from strong demand at a $22 billion 30-year bond reopening.

Economic data provided mixed signals. The December ADP Employment Change report came in below expectations at 122,000 (versus the KR Forecast consensus of 131,000). Initial jobless claims surprised to the downside at 201,000, notably below the KR Forecast consensus of 218,000 and the prior week's 211,000.

The release of the December FOMC minutes proved particularly significant. The minutes reinforced Fed Chair Powell's previous messaging, indicating the committee wants greater confidence in inflation's return to the 2% target before considering rate cuts. This messaging and other factors have led to a significant shift in rate cut expectations. According to fed funds futures, the probability of a March rate cut has declined to 40.4%, down from 53.0% a week ago and 69.1% a month ago.

Wednesday’s trading patterns reflected ongoing uncertainty about monetary policy and economic conditions in 2025. Markets remained closed on Thursday in observance of the National Day of Mourning for former President Jimmy Carter, providing participants with time to digest these developments before Friday's session.

The mixed performance across major indices suggests investors continue to grapple with the balance between strong employment data and the Federal Reserve's cautious stance on potential rate cuts, creating a complex environment for market positioning early in the new year.

Nasdaq Composite: +0.9% YTD

S&P Midcap 400: +0.7% YTD

S&P 500: +0.6% YTD

Russell 2000: +0.4% YTD

Dow Jones Industrial Average: +0.2% YTD

Reviewing Wednesday’s economic data:

Weekly MBA Mortgage Applications -3.7%; Prior -21.9%

December ADP Employment Change 122K (KR Forecast.com consensus 131K); Prior 146K

Weekly Initial Claims 201K (KR Forecast.com consensus 218K); Prior 211K, Weekly Continuing Claims 1.867 mln; Prior was revised to 1.834 mln from 1.844 mln

The key takeaway from the report is that layoff activity is low, but finding a new job has become more challenging for employees who lose their jobs.

November Wholesale Inventories -0.2% (KR Forecast.com consensus -0.2%); Prior was revised to 0.0% from 0.2%

November Consumer Credit -$7.49 bln (KR Forecast.com consensus $9.1 bln); prior revised to $17.3 bln from $19.2 bln

The key takeaway from the report is that consumer credit contracted in November for only the third time in the past 16 months with revolving credit, which is subject to extra high interest rates, acting as the drag.

Fridays Economic Calendar: January 10, 2025

The employment report headlines tomorrow's economic releases, with data arriving at 8:30 ET. KR Forecast anticipates December Nonfarm Payrolls of 165K, moderating from November's 227K increase. Private sector employment is expected to show similar moderation, with KR Forecast projecting 150K new jobs compared to November's 194K gain.

Wage growth will be closely monitored. December's average hourly earnings are expected to increase 0.3%, slightly below November's 0.4% gain. The unemployment rate is forecast to hold steady at 4.2%, while the average workweek is predicted to maintain its 34.3-hour reading.

Later in the morning, at 10:00 ET, the preliminary January University of Michigan Consumer Sentiment report will provide an early look at 2025 consumer confidence. KR Forecast anticipates a slight decline to 73.8 from December's 74.0 reading.

WaveTech Database