Will The Fed Pause?

Bitcoin Moves toward $109k

LIVE STREAM ANNOUNCEMENT: Fed Day Coverage

Join me tomorrow for live coverage of the Federal Reserve's crucial December announcement. The stream will begin 30 minutes before the Fed statement to provide a pre-meeting analysis and continue through Powell's press conference.

I also have an important announcement about an upcoming event you won't want to miss.

When: Wednesday, December 19th

Start Time: at 1:30 pm EST… 30 minutes before the Fed announcement

Where: youtube.com/thekendallreport

I'll post a reminder on Twitter just before we go live.

Please mark your calendars and join us for comprehensive Fed day coverage and a special announcement!

KR Opinion

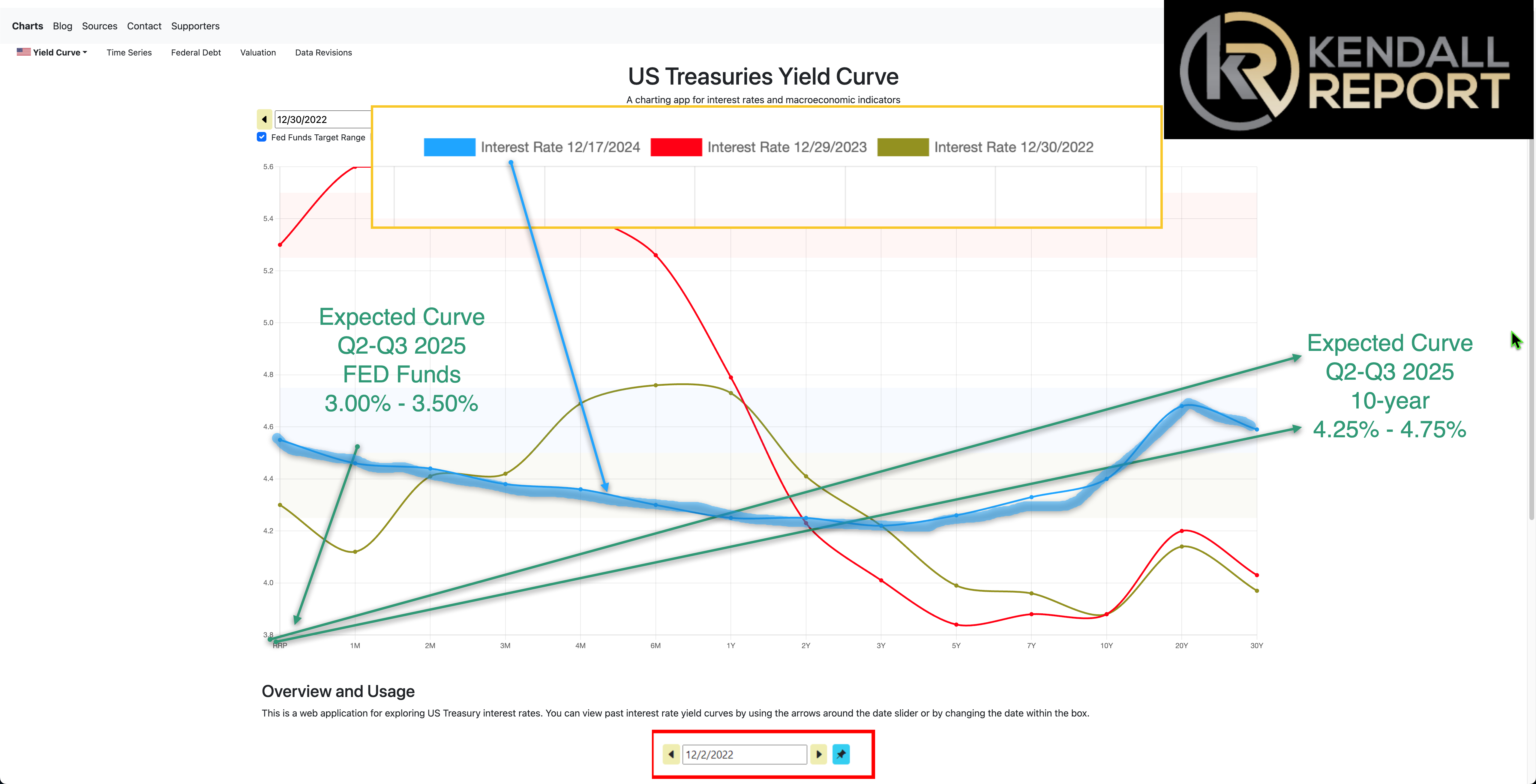

The consensus among major Wall Street firms that the 10-year Treasury yield will move to 5% is particularly interesting, especially as it aligns with my earlier predictions about an inflation echo bounce. While many attribute this potential move to proposed tax cuts and tariffs, there's reason to be skeptical of the more extreme projections of 5-6% yields discussed on CNBC.

The dynamics of the yield curve deserve careful consideration. Rather than seeing dramatic moves higher, a more likely scenario involves maintaining the curve's relatively flat back end. The optimal configuration would involve a more orthodox yield curve structure, with Fed funds and short-term rates (up to one year) around 3.25%, then steepening toward the longer end to somewhere between 4% and 4.75%. While 5% is possible, the current rhetoric about 6% yields seems overly aggressive.

Despite widespread enthusiasm from market participants, small-cap stocks remain in what could be called "Zombieland." Their real potential will likely be unlocked until the yield curve reconfigures into a more traditional shape. This restructuring would involve the short end, around 3.25% for Fed funds through one-year rates, steepening by 1.5% or 4.25-4.75% toward the longer end of the curve.

Expectations for a quarter-point rate cut at tomorrow's Federal Reserve FOMC meeting are high. However, the narrative that this might be the final cut seems premature. There's still approximately a 50% probability of the Fed skipping this meeting and implementing a cut in January instead. Looking further ahead, Fed funds rates will likely reach the 3.25-3.50% range, probably by the end of Q2 2025.

Current equity market behavior shows defensive positioning despite the broader risk-on environment. We're seeing consolidation patterns emerge, suggesting a continued sideways trading range rather than dramatic moves in either direction. While some upside potential exists over the next several days and possibly into next week, the overall expectation is for choppy, range-bound trading through year-end.

The inflation echo bounce that has been discussed for months will likely materialize soon, though its impact might differ from current market expectations. Tonight's technical report will provide a more detailed analysis of these factors and their potential market implications.

Looking Back on Tuesday’s Action

Today's stock market experienced broad weakness, with declines across major indices reflecting a shifting market sentiment. The Russell 2000's 1.2% decline led to the downturn, highlighting particular pressure on smaller companies. The equal-weighted S&P 500's 0.8% drop, steeper than the traditional S&P 500's 0.4% decline, indicates the selling pressure was widespread rather than concentrated in a few names.

In the technology sector, semiconductor stocks faced notable pressure. NVIDIA continued its recent weakness with a 1.2% decline, while Broadcom saw a steeper drop of 3.9%, contributing to the Philadelphia Semiconductor Index's 1.6% decline. However, some mega-cap tech stocks provided counterbalance, with Tesla surging 3.6% and Apple and Microsoft posting modest gains. These three companies, representing 16% of the S&P 500's weight, helped cushion the broader market's decline.

The healthcare sector faced significant pressure, particularly among companies with pharmacy benefit management operations. UnitedHealth Group fell 2.6%, while CVS Health dropped 5.5%. These declines followed President-elect Trump's comments about addressing pharmaceutical industry intermediaries, which created uncertainty around the future of drug pricing and distribution models.

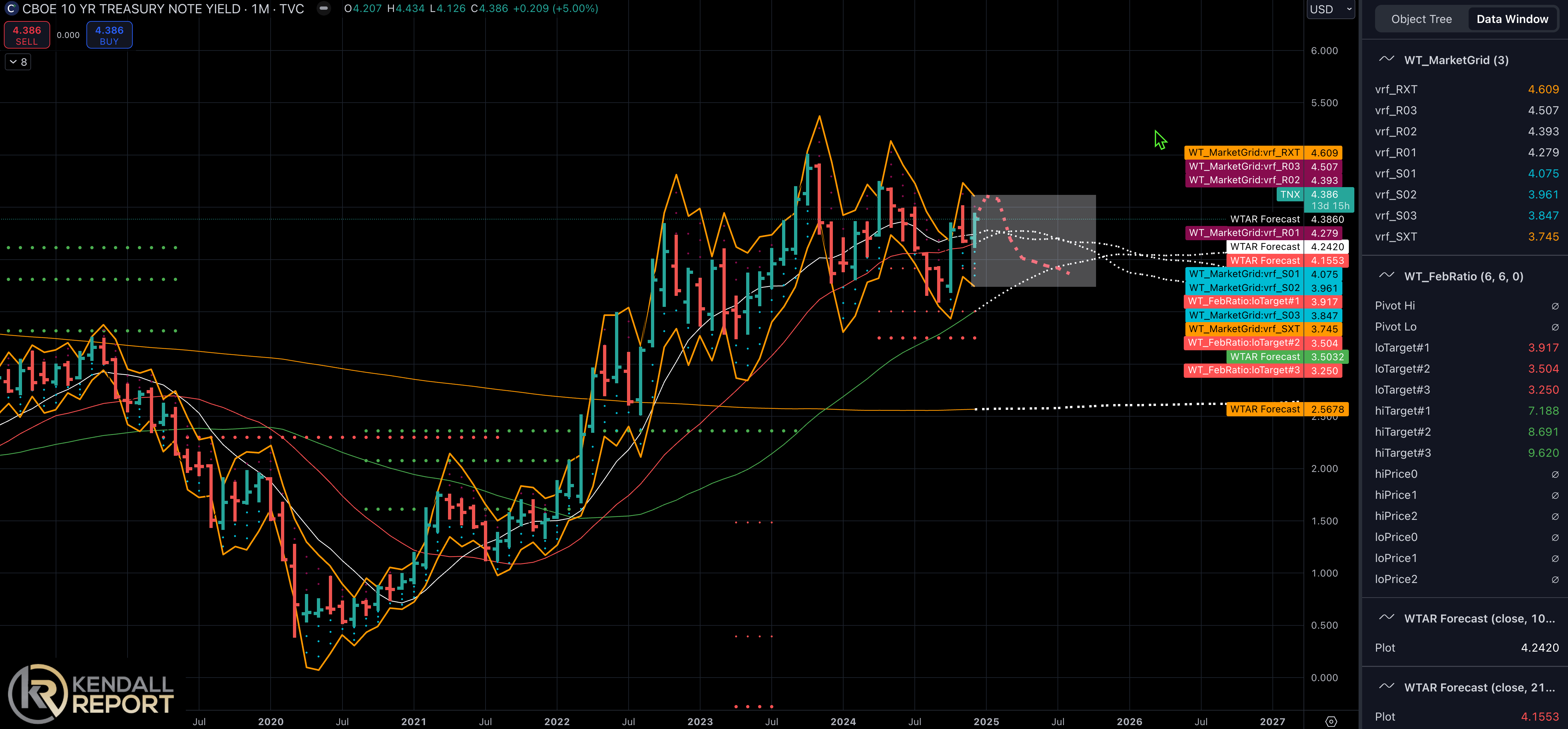

Fixed-income markets showed a measured response to the day's economic data. The 10-year Treasury yield settled at 4.38%, down two basis points, while the 2-year yield remained steady at 4.24%. The November retail sales report played a key role in today's market dynamics, with the modest 0.2% increase in sales excluding autos suggesting weakening consumer demand, especially considering the figures aren't adjusted for inflation. Adding to the fixed income narrative, a $13 billion 20-year bond reopening saw underwhelming demand, highlighting potential concerns in the longer-term Treasury market.

This combination of weak retail data, uncertainty in the healthcare sector, and mixed performance in technology stocks reflects a market grappling with sector-specific challenges and broader economic concerns.

Nasdaq Composite: +34.0% YTD

S&P 500: +26.9% YTD

S&P Midcap 400: +16.4% YTD

Russell 2000: +15.2% YTD

Dow Jones Industrial Average: +15.3% YTD

Tuesday's economic data releases painted a mixed picture of the U.S. economy, setting the stage for Wednesday's crucial Federal Reserve decision. November Retail Sales increased by 0.7%, surpassing the KR Forecast consensus of 0.5%. October's figure was revised up to 0.5% from 0.4%.

However, retail sales, excluding automobiles, rose only 0.2%, falling short of the 0.4% KR Forecast consensus. This modest ex-auto increase suggests consumer spending may be softening, as the numbers aren't adjusted for inflation. The gain likely reflects price increases rather than higher sales volumes.

Industrial Production was disappointed with a 0.1% decline, well below the KR Forecast consensus of a 0.3% gain. The previous month was revised lower to -0.4% from -0.3%. Capacity Utilization dropped to 76.8%, missing expectations of 77.3%. Despite some improvement in manufacturing output, the overall production figures haven't shown a strong recovery from hurricane-related disruptions in recent months.

Business Inventories increased 0.1% in October, slightly below the KR Forecast consensus of 0.2%. September's figure was revised down to 0.0% from 0.1%. The NAHB Housing Market Index held steady at 46 in December, just below the expected 47, indicating continued caution among homebuilders.

Wednesday's schedule is dominated by the Federal Open Market Committee's announcement at 2:00 ET, followed by Fed Chair Jerome Powell's press conference at 2:30 ET. This highly anticipated event will include updated economic projections and the Fed's "dot plot" showing officials' rate expectations. Market participants will closely analyze the statement and Powell's comments for signals about potential rate cuts in 2025.

The day begins with MBA Mortgage Applications data at 7:00 ET, following last week's 5.4% increase. According to KR Forecast, housing data takes center stage at 8:30 ET, with November Housing Starts expected at 1.347 million units and Building Permits projected at 1.430 million units.

The third-quarter Current Account Balance report is also due at 8:30 ET. Forecasts suggest a deficit of $283.0 billion, which is wider than the previous quarter's $266.8 billion. Energy markets will focus on the EIA Crude Oil Inventories report at 10:30 ET, following last week's 1.43 million barrel draw.

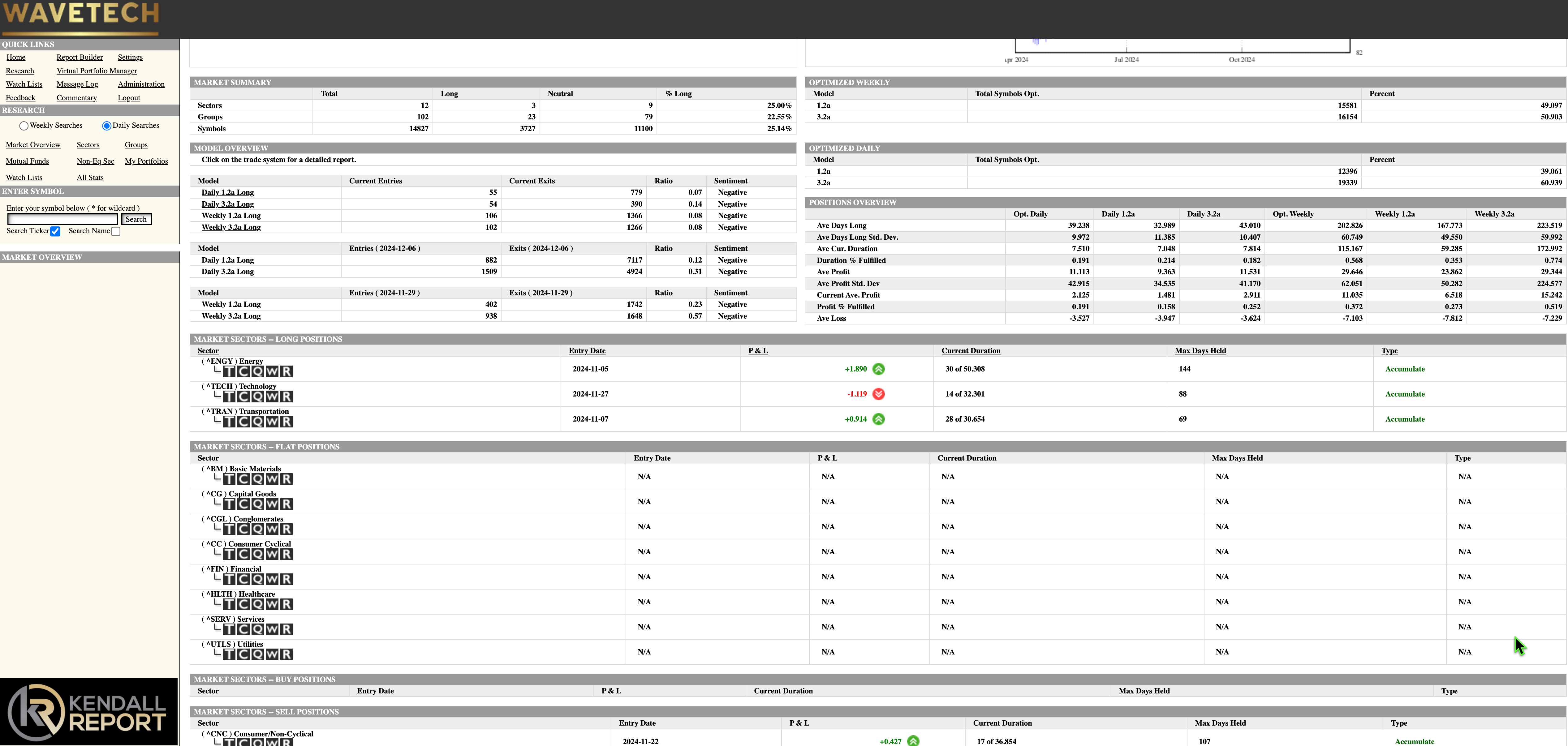

WaveTech Database

The market's breadth continues to weaken notably across multiple dimensions. Today's database shows a stark imbalance of 1,169 exits against only 109 entries, pushing the bullish percentage down to 25.14%. A break below the critical 22% level would signal a full liquidation phase, typically driving the percentage into the mid-to-lower teens, around 12%. However, historical extremes have reached as low as 6%.

Sector participation has contracted to just three sectors, which maintain bullish positioning. Energy leads despite minimal gains over its 30-day-long position, followed by Transportation and Technology. The recent exit signal in Consumer Non-Cyclical, after a 17-day-long position, further exemplifies the broader market weakness. Industry group participation has fallen dramatically, with only 22% maintaining long positions.

Over the past 5-8 sessions, this deterioration pattern suggests the weakness will likely spread into intermediate-term models as we approach year-end. The technical configuration indicates a potentially volatile start to 2025, though markets may continue consolidating soon.

The significance of this technical deterioration becomes particularly apparent against the backdrop of exceptional market performance over the past two years, with gains ranging from 44% to 50% across various indices. These substantial back-to-back annual returns are historically unusual, making the current weakening in breadth metrics especially noteworthy.

The systematic reduction in market participation, sharply reduced sector exposure, and declining industry group positioning indicate elevated market risks ahead. These technical signals suggest a potential shift in market dynamics as we transition into the new year, warranting careful attention to risk management and position sizing.

S&P 500 December Futures contract

The S&P futures show an intriguing technical setup, indicating a potential V-shaped bottom formation over the next several days. Supportive Federal Reserve rhetoric during tomorrow's announcement could reinforce this pattern. The market grid shows a downward slope with resistance between 6072 and 6082 and an upside extreme at 6092. Support levels have established themselves at 6042 and 6031.

Algorithmic indicators suggest upward price movement. A higher close today would likely trigger an upward shift in the market grid, potentially leading to several days of higher prices. While previous Fibonacci targets pointing to a potential decline to 5912 remain technically valid, the current readings across all three Price Pressure Momentum indicators don't support such a significant downturn.

The likely scenario is continued sideways movement within the market grid's parameters. However, traders should prepare for increased volatility, which typically accompanies FOMC announcements and is likely to be particularly pronounced during Powell's press conference.

The technical configuration suggests we're at a pivotal point where the Fed's communication could significantly influence market direction. The potential V-bottom formation, combined with the current momentum indicators, points to a possible upside, though contained within the defined technical ranges. This setup creates an environment where precise technical levels can guide trading decisions while accounting for the expected increase in volatility around tomorrow's Fed events.

Tomorrow's Fed decision and subsequent press conference could be catalysts to either confirm or negate this technical setup, making the next 24 hours particularly crucial for short-term market direction.

NASDAQ December Futures

The NASDAQ's performance this year has been nothing short of extraordinary, and momentum indicators have shown exceptional strength. Price Pressure Momentum readings are particularly robust, with PPM 1 at 0.37 and PPM 2 at 0.38, indicating a steep upward trend with significant momentum. These technical readings reflect the market's robust upward trajectory.

The index has already hit the Fibonacci target at 22,223 and now appears poised to challenge the final target at 22,538. Technical indicators suggest this positive momentum could extend into early next week. While the bottom formation isn't as clearly defined as what we see in the S&P 500 futures, the upward momentum remains strong and well-defined.

An interesting market dynamic has emerged: Rising yield expectations drive more capital into technology stocks. Rather than acting as a headwind, higher yields on the long end of the curve appear to make these tech names more attractive to investors, a pattern that has persisted throughout the year.

The key technical levels for today's session are well-defined. Support is between 22,240 and 22,169, while resistance is 22,440 and 22,511. If reached, the upside extreme at 22,575 would coincide with hitting the third Fibonacci target, potentially marking a significant technical milestone.

Despite and perhaps because of higher yield expectations, the continued surge in tech stocks demonstrates how market dynamics have evolved. This relationship between yields and tech stock performance has been a defining characteristic of this year's market behavior, challenging traditional correlations and creating opportunities in the technology sector.

Treasuries

Given the technical and fundamental setup, the current market consensus anticipating 5-6% yields on the 10-year Treasury as we move into 2025 appears overly aggressive. While a move toward 5% remains possible, the more probable range lies between 4.25-4.75%, with potential peak levels around 4.60-4.75%. With the Fed's current strategy, the notion of yields pushing substantially above 5% seems unlikely.

A significant shift appears to be underway in the Federal Reserve's approach to monetary policy, potentially returning to a more market-driven rate environment reminiscent of the 1970s and 1980s. In this scenario, the Fed would focus primarily on managing the discount rate and Fed funds rate, allowing market forces to determine yields across the broader spectrum. This represents a move away from the intensive market management we've seen in recent years.

The progression of the yield curve from 2022 through the present reveals an interesting evolution. We've moved from the deeply inverted curve of 2023, which sparked widespread recession concerns, to the current configuration. The projected path suggests continued yield normalization into 2025, with Fed funds and short-term rates likely settling around 3.25-3.5%, establishing a neutral rate relative to inflation.

It's crucial to understand that the Fed isn't in a traditional loosening cycle but is instead continuing the normalization process it initiated nearly two years ago. This gradual approach is intentional, as rapid rate movements can disrupt banking system stability, hedge positions, and overall balance sheet structures. Even when the direction is toward lower rates, the pace of change matters significantly for market stability.

Looking ahead to 2025, expectations include at least three rate declines if they skip this meeting and two if they decide to do a .25% drop at this meeting, regardless of potential inflation fluctuations. The key objective is achieving a neutral rate where short-term rates align more closely with inflation. Whether the Fed implements a rate cut at this meeting or skips to January, this is part of a longer-term normalization strategy rather than the beginning of an aggressive easing cycle.

Tomorrow's Fed announcement and Powell's commentary will provide crucial insights into how this normalization process might unfold, particularly regarding the pace and extent of future rate adjustments. The market's interpretation of this guidance could significantly impact near-term yield movements and broader market dynamics.

Bitcoin