Will The Yen Trigger Chaos?

New upward Fib Targets for the S&P 500 Futures!

KR Opinion

Yesterday's trading session presented some intriguing dynamics. Initially, the market peaked early, reaching a high between 5220 and 5237, based on the S&P 500 futures, specifically hitting 5226. This was followed by about an hour to two hours of sideways trading before the market drifted lower towards the close. Despite this, the market remained relatively stable, closing slightly higher.

From a technical perspective, we are observing a pattern that suggests a continued sideways movement with a potential for upward movement, which I will discuss more in the S&P quantitative section below.

On the fundamental side, some disappointing earnings from Disney negatively affected market sentiment, likely contributing to the market's fade after the initial trading hours. However, the overall earnings landscape was mixed but somewhat supportive, which helped keep the indices within an upward trending range.

We are beginning to see new market patterns that hint at a possible extension to the upside. Despite a quiet day in terms of database activity, indicating a consolidation, emerging signs suggest higher prices might be on the horizon.

Regarding economic data, there was a notable moderation in consumer credit expansion, which came in significantly lower than expected. This counters the prevailing narrative that rising credit card debt further strains the economy. This data point suggests a potential flattening trend in consumer credit, at least for the month, and it remains to be seen if this will continue.

Despite ongoing concerns among some observers about a possible major market collapse—some predicting as much as a 50% decline—such an extreme outcome seems unlikely. Expectations are set for the market to continue its sideways trajectory as we head into Wednesday, which looks to be shaping up as another lackluster session.

Looking Back on Tuesday’s action

Today's stock market had a mixed close, with varying performances across the major indices. The Nasdaq Composite fell by 0.1%, pulled down by significant losses in large technology companies and the semiconductor sector.

In contrast, the S&P 500 and the Dow Jones Industrial Average ended the day slightly up by 0.1%. The Russell 2000 index outperformed, gaining 0.4%.

Market breadth was mixed beneath the surface. At the NYSE, advancers outnumbered decliners by a 4-to-3 ratio, whereas at the Nasdaq, decliners slightly outnumbered advancers.

The trading session started positively, but momentum shifted to selling after the S&P 500 peaked at 5,200.23. This led to a sharp downturn across the major indices, which eventually recovered somewhat before the market closed.

Earnings announcements influenced stock performances significantly. Walt Disney and Builders FirstSource were among the worst performers in the S&P 500, with their stocks plunging due to disappointing earnings or guidance.

On the positive side, FMC Corp. and International Flavors & Fragrances saw substantial gains following their positive quarterly results and outlooks.

Only three of the S&P 500 sectors declined, while four advanced by at least 1.1% sector-wise. The consumer discretionary and information technology sectors experienced the largest drops, largely due to weaknesses in major companies.

Conversely, the materials and utilities sectors were the leading gainers.

In the bond market, the yield on the 2-year note rose slightly by one basis point to 4.83%, while the 10-year note yield decreased by three basis points to 4.46%. These movements followed a well-received $58 billion sale of 3-year notes earlier.

·Nasdaq Composite: +8.8% YTD

·S&P 500:+8.8% YTD

·S&P Midcap 400: +7.0% YTD

·Dow Jones Industrial Average: +3.2% YTD

·Russell 2000: +1.9% YTD

Reviewing Tuesday’s economic data:

Consumer credit rose by $6.3 billion in March, below the expected increase of $15.3 billion. This followed an upward revision for February's figure, which was adjusted from $14.1 billion to $15.0 billion.

The main observation from the report is that credit expansion slowed in March, with little change in revolving credit (such as credit card debt).

For Wednesday's economic calendar:

- At 7:00 AM ET: The Weekly MBA Mortgage Index will be reported; the previous reading showed a decline of 2.3%.

- At 10:00 AM ET: March Wholesale Inventories are expected, with a KR Forecast consensus predicting a decrease of 0.4%, following a previous increase of 0.5%.

At 10:30 AM ET, crude oil inventories will be updated. The last report indicated an increase of 7.27 million barrels.

WaveTech Database

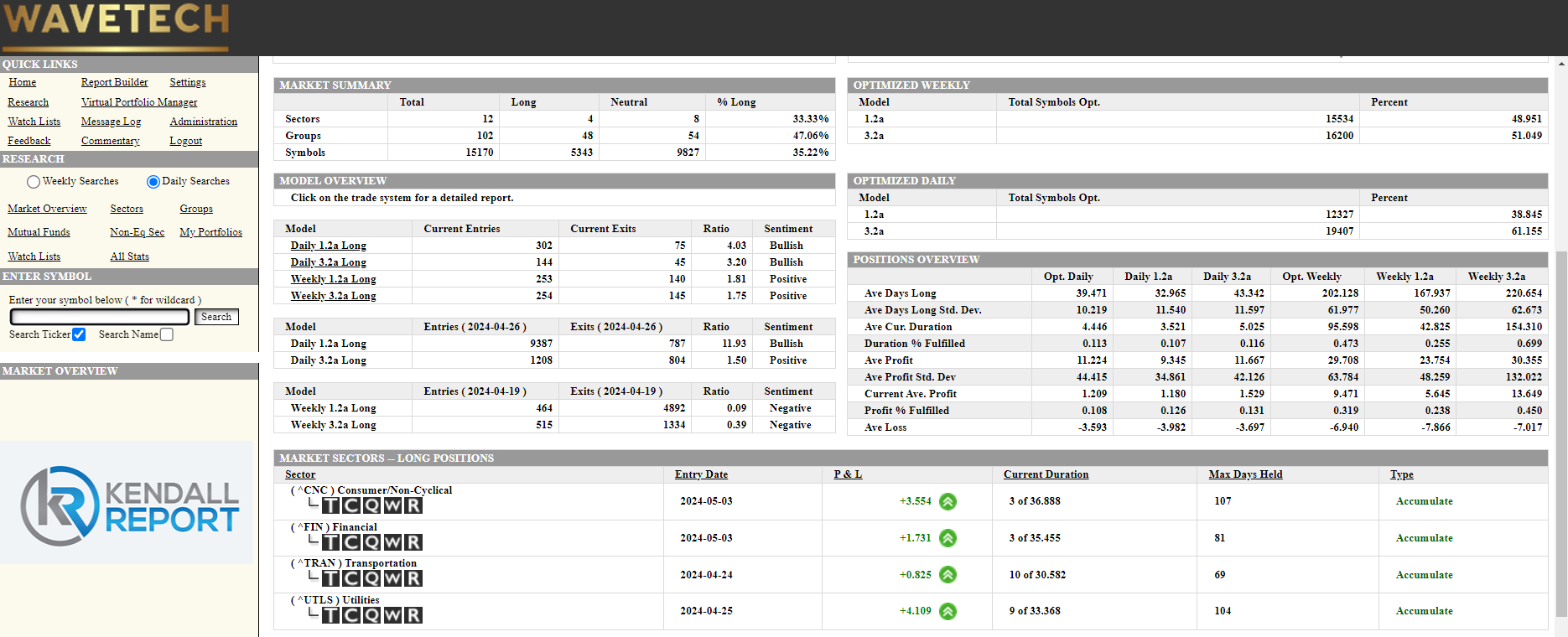

The database has not seen much new activity, with 446 new entries and 120 exits, pushing the bullish percentage to 35.22%. This figure remains below the important threshold of 42%, suggesting that the market might continue to move sideways.

The data indicates that the market may have reached a short-term low. The potential for an upward trend increases if the bullish percentage can exceed 42%. Although there has been a noticeable buying bias recently, as evidenced by emerging bullish ratios, these have not been strong enough to push the database past this threshold and signal the beginning of a more significant trend.

S&P 500 Futures